Let’s look at the correlation between size of independent advisory firms and the average wealth of the clients they serve.

Let’s look at the correlation between size of independent advisory firms and the average wealth of the clients they serve.

Recently, in separate conversations, Michael Kitces of Nerd’s Eye View and Angie Herbers of Herbers & Company told me something very similar. Kitces said that the larger an advisory firm becomes, the more it has to rely on wealthier clients to sustain itself financially. The internal expenses become so great that the firm has to move upscale to survive.

Meanwhile, Herbers said that she is witnessing a vacuuming effect in the profession, where the largest advisory firms are gaining a very high percentage of the wealthiest clients. It is becoming very difficult for smaller firms to compete in the high-net-worth space.

Being naturally excitable by nature, I found these pronouncements – from people I greatly respect –alarming. They brought back unhappy memories of the dystopian landscape that Mark Hurley predicted (albeit wrongly) 20 years ago for the advisory space: that the profession would be dominated by a small handful of very large firms, with a diminishing number of smaller firms in fierce and unprofitable Darwinian competition for the meagre scraps off the table.

Is it true that, if your firm grows dramatically, you will have to give up the unprofitable smaller clients and rely on attracting larger ones (surely a risky bet) to survive?

Is it true that, if your firm is small, you will find it difficult or almost impossible to attract wealthier clients?

It turns out that I was in possession of some data that explored the accuracy of these observations and could see whether we are traveling down the dystopian path predicted so long ago. Our annual T3/Inside Information software survey collects demographic data on the survey respondents – 5,255 advisors from our upcoming (not yet released) 2021 survey. These advisors rate the software products they use on a scale of 1-10 in 32 different categories (CRM, financial planning, portfolio management etc.), but the survey also asks for information about their revenue model (fee-only, dually-registered, wirehouse), about the annual revenues of the firm (which tells us the size of the firm), and the average “size” of its clients, measured by investible assets.

Before I get into the statistics, I should warn the reader that there are a variety of ways that this data can be skewed, leading to potentially misleading conclusions. Perhaps the most worrisome is that a brokerage rep would report average client size in his/her book of business, and then report the size of his overall firm – Morgan Stanley or Merrill Lynch, perhaps – which would give a misleading view of the match between average client size and firm size. Reps with 100 clients mostly under $1 million in portfolio size would report the size of their firm at the top of the scale – which might provide evidence that larger firms are working with smaller clients.

The same problem would exist with of investment advisor representatives of independent broker-dealers, who would be reporting the size of their employers rather than the size of their actual offices.

Another problem is that our survey didn’t collect data on the full range of clients from each respondent; only their estimate of the average “size” of their clients’ AUM across the full book of business. So one firm might serve mostly clients with $1-2 million in assets, and all the remaining clients have larger portfolios. Another firm might serve mostly the same size clients, with $1-2 million in assets, but everybody else has smaller portfolios. The two firms would show up the same in our data set.

With those limitations in mind, let’s look at what the respondents told us about size of firm versus size of clients. The first thing I did was eliminate brokerage firm and dually-registered reps from the analysis, for reasons cited above. That left only fee-only planners, which cut the overall sample from 5,255 responses down to 2,460 independent firms of all sizes.

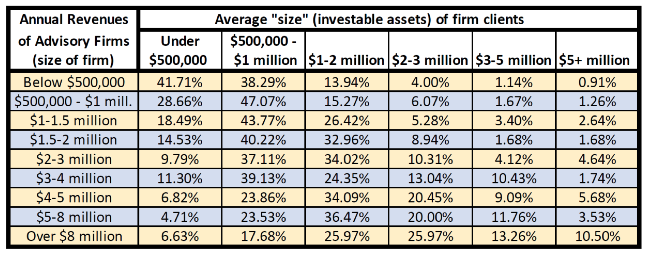

The survey divided those fee-only firms into size categories, not by AUM (some firms, after all, don’t actually manage client assets), but by annual revenues collected by the firm. The size categories ranged from small, lifestyle firms with less than $500,000 in total annual revenues to much larger enterprises whose yearly revenues were more than $8 million.

For each size category, I calculated the percentage of those organizations whose average client fell into each of six average client size categories, ranging from average investible assets less than $500,000 up to more than $5 million.

You can see the results in the table below. In general, there’s a clear pattern that supports, albeit not terribly strongly, the Kitces and Herbers observations. The smallest firms are primarily working with less wealthy clients; almost 42% of the smallest firms are focusing on what might be called the mass-not-yet-affluent (under $500,000), and another 38% are working with people who might just barely qualify as mass-affluent (average portfolio size of $500,000 to $1 million).

Slightly larger firms, whose annual revenues fall in the $500,000 to $1 million range, are more than 70% likely to have average clients with $1 million or less to invest.

Conclusion: The smallest firms tend to have, on average, the least wealthy clients. Kitces and Herbers didn’t say this directly, but it generally supports their observations.

As you move up in firm size, firms tend to have wealthier average clients. The percentage of firms whose average client has less than $1 million to invest goes down, from 60% for the firms with $1-1.5 million in annual revenues, to less than 25% for firms that collect more than $8 million a year from their clients.

Meanwhile, at the higher end of the client-size spectrum, very few small firms (0.91% and 1.26% respectively for the smallest and next-smallest firms) report that their average clients have over $5 million AUM. More than 10% of the larger firms have clients primarily in that size category. If you look at the last two columns, from top (smallest firms) to bottom (larger ones), you see that, in general, the largest firms tend to be working with larger clients.

But what I found most interesting is that this spectrum is not nearly as monotonic as Kitces and Herbers claimed. Just under 25% of the firms with more than $8 million in revenues reported in our survey that their average client has less than $1 million AUM. A sizable number of the largest firms appear to be working with clients with investible assets below $2 million, and this is true also for the next-largest firms with $5-8 million in annual revenues. Assuming that these firms are still in business, it is possible for enterprise advisory firms to survive their internal economics without moving wholesale to an upscale clientele.

Once a firm gets above $3 million in annual revenues, it becomes more likely to have clients above $2 million in assets, which suggests that wealthier clients tend to prefer to work with firms that have size and scale. But at the same time, there still seems to be plenty of competition for the wealthiest clients across the spectrum of the fee-only advisory space. Nine percent of firms with under $1 million in assets report their average client to have at least $2 million in assets (adding up three columns), and 2.64% of those small firms are primarily working with clients with $5 million and above. The competition for clients with between $2-3 million in assets appears to be fierce.

It would be interesting to profile some very small firms that specialize in clients at the top of the wealth scale, and some much larger firms whose bread-and-butter clients are still aspiring to mass affluent status. I don’t doubt the underlying truth of the Kitces and Herbers observations, but I find myself wondering how easy (or hard) it is to be a contrarian. Clearly, more firms are doing it than many observers realize.

What else does the data tell us? The bread-and-butter client in the fee-only space, pretty much across the board, is someone with $1-2 million in assets, followed by people with $500,000-$1 million to invest. Once a firm achieves $5 million in revenues, the most likely average client will fall somewhere in the $1-3 million range – which makes me wonder how many significantly wealthy clients there are in the deep red AUM ocean where most advisory firms are targeting their marketing efforts.

Beyond that, there is a somewhat awkward stage that advisory firms reach as they grow their revenues. Notice that a significant percentage of the firms with $3-4 million in revenues report that most of their clients fall into the smallest size category, and just 1.74% of these firms typically work with clients over $5 million – fewer than firms that are smaller and larger than they are. It could be that this is a transition point where the firm is still dependent on its legacy clients and has not yet reached upscale.

Overall, looking at the data, I’m less alarmed. The advisory space continues to be competitive at all levels for all types of clients. The dystopian predictions haven’t come true in the advisory marketplace – and my longstanding prediction continues to be that they never will.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com.

More Portfolio Building Topics >

Let’s look at the correlation between size of independent advisory firms and the average wealth of the clients they serve.

Let’s look at the correlation between size of independent advisory firms and the average wealth of the clients they serve.