Does time diversification work in the real world? Do portfolios get less risky – i.e., converge to a more reliable expected return – the longer we wait?

Does time diversification work in the real world? Do portfolios get less risky – i.e., converge to a more reliable expected return – the longer we wait?

Or do we believe in time diversification because we are not very good at mathematics?

To get into a fierce dispute where the person on the other side of the argument will not hear any contrary evidence, try talking to a mathematically oriented advisor about time diversification.

In the heated discussions that I’ve been involved in, the person on the other end of the argument is a proponent of dynamic or tactical asset allocation, meaning that they shift allocations according to investment regimes, economic scenarios, or various stages of the economic cycle. They tell me that this is necessary because without their intervention, the actual client investment experience would become increasingly volatile over time.

The simple version of their argument is that it’s just mathematics; time diversification is an illusion. The spectrum of expected outcomes in a diversified portfolio doesn’t narrow over time; it actually expands dramatically.

The mathematics of this argument are similar to what you see in Monte Carlo analyses. You start with a certain expected return and standard deviation of returns around it. The Monte Carlo engine then pulls random returns out of a hat, year after year, for, say, 10,000 30-year sequences. Some of those sequences are going to be catastrophic: the engine will, somewhere in those 10,000 iterations, pull out a sequence that starts with a return like we experienced in 1931 (-43.34%), and 1974 (-26.47%), followed by 2002 (-22.10%), 2008 (-37.00%), 1930 (-24.90%), 1937 (-35.03%), 1930 (-24.90%) –you get the picture. Two or more of those 10,000 random selections might just be combinations of all those disagreeable possibilities.

At the other end of the spectrum, the Monte Carlo engine will have pulled out, at least once, a sequence of stellar bull-market returns, one after another. By including the most optimistic sequence with the gloomiest, you will, indeed, see that the possible range of client investment outcomes expands over time, rather than contracts.

Does that win the argument, ipso facto? Somewhere around the third beer, I find myself wondering whether the markets behave according to the tenets of pure mathematics. How is it that, in the real world, we never experience a long unbroken bear market that lasts decades – or, for that matter, a long bull market of the same longevity? In the time sequences that we have lived through, the horrible returns from 1929 through 1932 was followed by a 53.99% return in 1933, and 1935 and 1936 (47.67% and 33.92% respectively) were at least moderately corrective for a patient investor. Though 1973 and 1974 were pretty bad (-14.66% and -26.47%), 1975 (37.20%) and 1976 (23.84%) helped moderate the damage. Although 2008 was a bad year, what came after was not bad at all.

Does the historical record strongly or weakly back up my side of the argument? To get a reliable answer, I turned to a helpful tool on the Andes Wealth Technologies software platform. Andes is a Swiss army knife of modern portfolio theory data; you can look (as we’ll see in a minute) at the efficient frontier for any time period, see graphs and charts of returns and risk measures for any portfolio, and construct graphs showing greatest drawdown for any portfolio combination over short or long time frames in any economic environment.

Advisors I’ve talked with use Andes for its risk tolerance capabilities plus the fact that it automatically generates an investment policy statement based on client selections. But you can also use it to compare the riskiness of a prospect’s existing portfolio with the model portfolios that the advisor would recommend (the marketing feature) – and some advisors use the program to evaluate the downside risk of their models. There are a variety of client risk-tolerance quizzes and presentations of the risk/reward characteristics of model portfolios as well, and clients can choose the model they’re most comfortable with by selecting it from a graph that shows the historical upside and downside of each model.

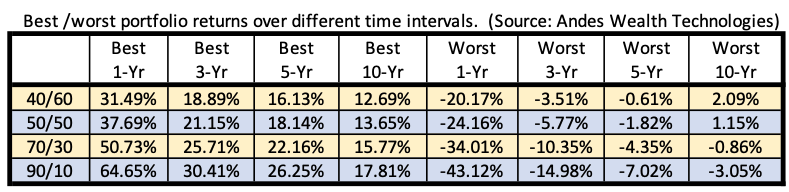

The part of the Andes software that I delved into shows any given portfolio’s best/worst returns over different time periods: one, three and six months, and one , three, five and 10 years. We all know that the average returns of different portfolio mixes have, historically, tended to converge over longer time periods, but here we’re looking at the key issue that people who don’t believe in time diversification are arguing about. Sure the average converges over time, but what about the upper and lower bounds, the best and worst returns over longer time periods? They should be a better measure of time diversification.

In the chart above, I show the best and worst one-, three-, five- and 10-year returns since 1980 for a spectrum of increasingly aggressive combinations of the SPDR S&P 500 ETF (SPY) and the Vanguard Total Bond Market ETF (AGG). Across all of these portfolios, without exception, as we move from one year to three, to five to 10 years, your best return smoothly decreases from shorter time spans to larger ones, and the worst returns moderate in exactly the same way. Not only do average returns moderate as you lengthen the holding period, but so too do the upper and lower return outcomes.

But if pure mathematics does not give us an accurate picture of how portfolio risk behaves over time, then what is the explanation? My best answer is that there are several external factors that intercede whenever market movements inflict pain on investors.

To take a simple example, we might have gotten one of those worst-case Monte Carlo sequences back during the Great Depression; we were certainly headed in that direction. But then came the New Deal, where the government took a highly active role in mitigating the economic decline. The markets stabilized, and there were a couple of years when the new legislation spurred optimism among investors. During that time, the investment returns were not being driven by pure mathematics; there was government intervention and an aggressive intervention in the mass psychology of investors who saw better times ahead.

Again, from 2008 to 2009, there was a severe downturn that was addressed by massive government intervention to prop up the economy and protect the markets from further collapse.

We are living through more evidence of this government mitigation today. The markets turned south in March, the Fed dropped rates to zero, and then there was a stimulus package and people were receiving checks in the mail from the federal government. Zero interest rates meant that there was no place else for investors to go than into stocks.

Indeed, some commentators have argued, persuasively, that the Fed is now paying at least as much attention to the stock market as it is to the economy and inflation. But even if you don’t buy that argument, you can see that our central bank does not hesitate to pull the levers of interest rates and capital flows whenever the economy shows signs of distress.

Beyond that, simple economic theory suggests a self-correcting mechanism that is not accounted for in the pure mathematics of multiplying each year’s volatility by the next. A severe recession or depression flushes out a lot of unproductive companies, inventory buildups and unwise expenditures, much like a forest fire cleans out the clutter in a dense woodland. In the aftermath, we don’t get another forest fire, and another, and another; similarly, we don’t get a second, third and fourth wave of bankruptcies. In each case, there is opportunity for new growth once the dead wood has been eliminated.

Take a second look at the chart, and you can see roughly when to expect the posse to arrive – or the fire to have finally cleared out the undergrowth. There’s a pretty big shift from worst one-year to worst three-year results across the entire spectrum of portfolio mixes. That suggests that after, at most, a couple of down-market years, corrective measures have been taken by the Fed, the government printing presses and the new entrepreneurs who are moving into niches once occupied by zombie companies.

You don’t see a drop of that magnitude in the positive return numbers: from one to three years, from three to five, from five to 10. I suspect that those who hold the economic levers are not quite as inclined to pull them when the markets are going up. It looks like most of the value in time-diversification is coming from a mitigation of downside returns, though the trend still does show up (less dramatically) in the best returns over different time periods.

Once you realize that you have historical statistics and modern portfolio theory cut and sliced in whatever way you want to see it, the Andes program becomes addictive. In another session with the software, I looked at a question related to the first one: whether the historical efficient frontier can be relied on as a guidepost for future returns.

Some advisors are not using dynamic asset allocation to save us from the gloomiest mathematics of future return dispersion. Instead, they will try to put their model portfolios on this hypothetically most efficient combination of assets, with the idea that it will, eventually, produce the best return per unit of risk over time. Andes has a feature which shows how far the prospect’s existing portfolio is from this curve of ideal portfolio mixes. (Another marketing tool; if the portfolio is also far from their risk tolerance, this helps to motivate them toward professional management.) But for existing clients, the program shows how far the actual investment experience has been from what the long-term projections would suggest. If you tweak the system a bit, it will show you the whole efficient frontier defined by a spectrum of model portfolios.

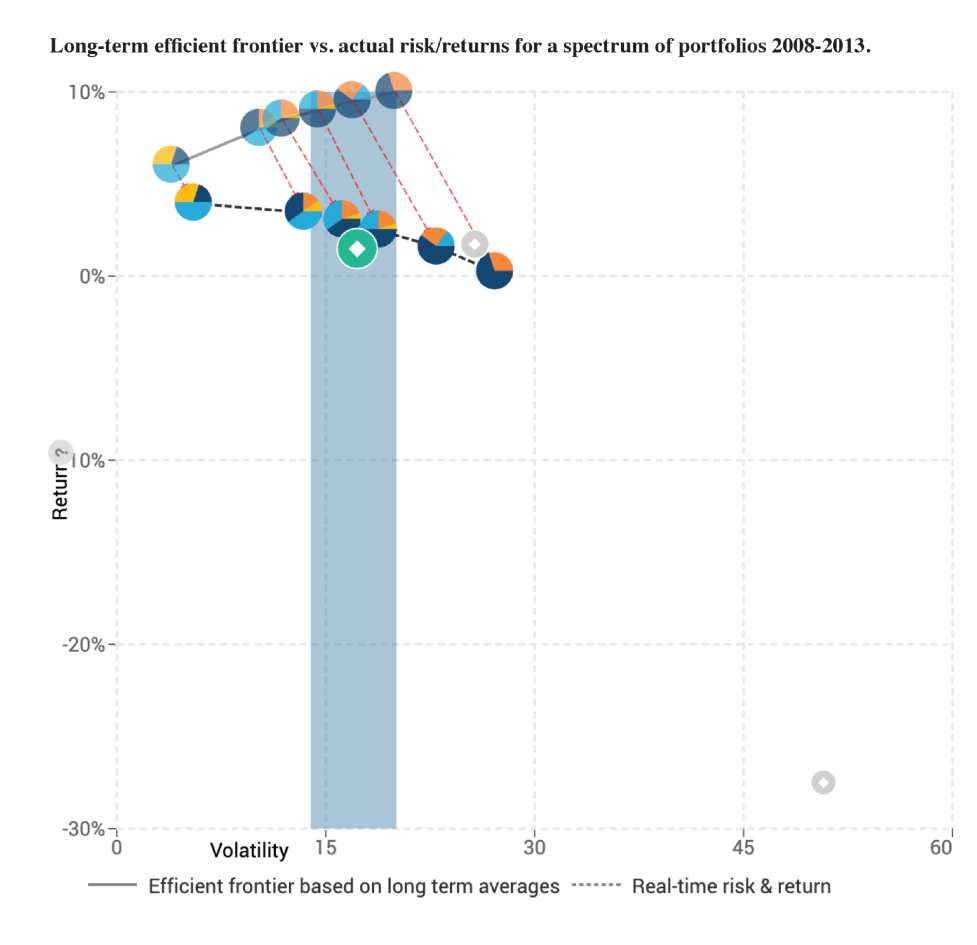

The following graphs show actual (dotted line) versus historical (solid line) efficient frontiers for the most recent 10 and five years for periods ending on January 1 of this year. They’re pretty close, which means the recent returns of portfolios that were placed on the historical efficient frontier matched up pretty closely with actual the actual efficient frontier for each of these time periods. In other words, the portfolios did pretty much what advisors were hoping they would do. (see below)

Taking that out to 20 years shows that, although the actual returns were lower than long-term return expectations for every portfolio on the spectrum, following the efficient frontier asset mixes proved to be nonetheless optimal. (see below)

The increasingly aggressive asset mixes I used are as follows:

Classic Conservative 20/80: 20% SPDR S&P 500 ETF; 50% Vanguard Total Bond Market; 30% iShares Short Treasury Bond ETF

Classic Balanced 50/50: 35% SPDR S&P 500 ETF; 15% iShares MSCI ACWI ex US ETF; 40% Vanguard Total Bond Market ETF; 10% iShares Short Treasury Bond ETF

Classic Balanced 60/40: 40% SPDR S&P 500 ETF; 20% iShares MSCI ACWI ex US ETF; 35% Vanguard Total Bond Market ETF; 5% iShares Short Treasury Bond ETF

Classic Growth 70/30: 50% SPDR S&P 500 ETF; 20% iShares MSCI ACWI ex US ETF; 20% Vanguard Total Bond Market ETF; 10% iShares Short Treasury Bond ETF

Classic Aggressive 85/15: 60% SPDR S&P 500 ETF; 25% iShares MSCI ACWI ex US ETF; 15% Vanguard Total Bond Market ETF; 0% iShares Short Treasury Bond ETF

Classic Aggressive 100% Stocks: 70% SPDR S&P 500 ETF; 30% iShares MSCI ACWI ex US ETF; 0% Vanguard Total Bond Market ETF; 0% iShares Short Treasury Bond ETF

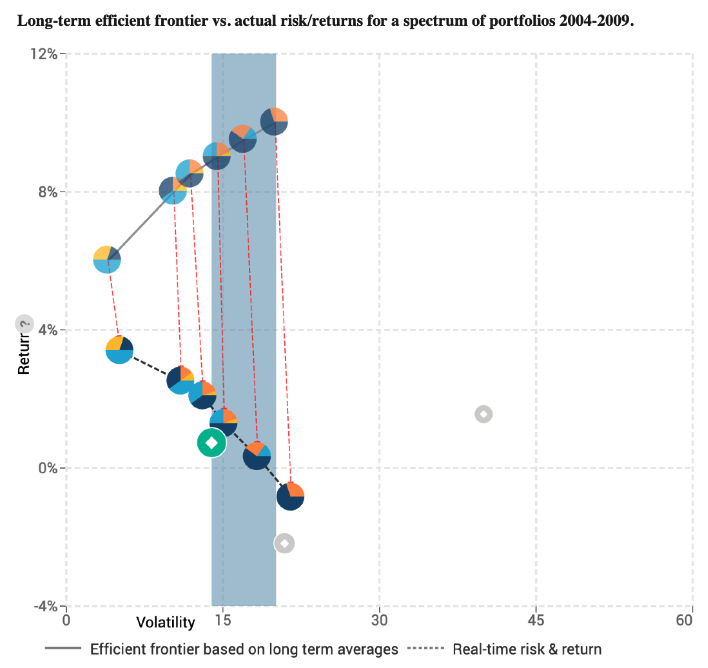

Alas, this exercise tends to underestimate how much five-year actual returns across the spectrum of portfolios can deviate from the long-term efficient frontier before they snap back to normalcy. Look at the difference between the historical efficient frontier and the actual performance of those same asset mixes for the five-year period ending January 1, 2014 (2008 through 2013; see below). During that time period, the most "efficient" portfolios were the ones with the highest percentage of bonds and the lowest percentage of stocks. Of course, nobody could have predicted that, but it shows that you don't always get what the long-term return pattern would recommend.

You see a more dramatic difference for the five-year period ending on January 1, 2010 (2004 through 2009) – a time period which ended, some may remember, with the great recession. (see below)

What I take from this exercise is that, yes, there are mechanisms impacting the market in ways that drive down the dispersion of results over longer time periods – and they work hardest to prevent bear markets from lasting for more than three years.

But at the same time, advisors should warn clients not to expect that, just because a portfolio is designed according to the long-term efficient frontier, it will perform accordingly. A graphic like these, appended to an annual performance report, shows clients that you did what you could to create an efficient portfolio, and the markets made a different decision.

I’d like to start a discussion. Does anybody still want to argue that, based on pure math, the dispersion of returns to investors grows over time, rather than narrows? Or do you agree with me that the spectrum of returns declines due (perhaps) to exogenous factors like interventions by government and central bank?

I’ve never won this argument outright; maybe this is my last chance.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com.

More Portfolio Building Topics >

Does time diversification work in the real world? Do portfolios get less risky – i.e., converge to a more reliable expected return – the longer we wait?

Does time diversification work in the real world? Do portfolios get less risky – i.e., converge to a more reliable expected return – the longer we wait?