Try out the Big Picture App here free for 30 days.

It’s been my privilege to meet and correspond with William P. Bengen, whose name many will recognize for his pioneering research on safe withdrawal rates (SWRs). In one of our discussions, Bengen noted that the following questions had not been well explored: Is there an optimal number of asset classes for a retirement portfolio, and which are most impactful? Are there diminishing returns to adding more asset classes and, if so, at what point do they reach zero?

It’s been my privilege to meet and correspond with William P. Bengen, whose name many will recognize for his pioneering research on safe withdrawal rates (SWRs). In one of our discussions, Bengen noted that the following questions had not been well explored: Is there an optimal number of asset classes for a retirement portfolio, and which are most impactful? Are there diminishing returns to adding more asset classes and, if so, at what point do they reach zero?

Intrigued, I decided to use the “Big Picture” client education software to examine the impact of portfolio diversification on historical SWRs and other retirement outcomes. The striking results may help advisors persuade retirees to review their asset allocation strategy.

Approach

My research builds on the work of Bengen, who in 1994 published his pivotal study, Determining Withdrawal Rates Using Historical Data. The originality of his work sprang from the use of rolling retirement periods. He showed us how the retiree’s portfolio had fared, under various spending levels and equity weightings, in every investment landscape that retirees faced, starting January 1, 1926. By accounting for the worst historical retirement periods, Bengen quantified sustainable spending in a way that past performance averages, by definition, could not.

Bengen focused initially on bond and large-cap stock portfolios, but later measured how the addition of other asset classes, such as small-cap stocks, affected safe withdrawal rates. He also began to use data that was quarterly, rather than yearly, in frequency, thus boosting his sample size of rolling periods. Bengen’s conclusions continue to enlighten and inform today’s financial planner.

I complement Bengen’s research by accounting for the effects of further portfolio diversification on SWRs. The Big Picture software allows advisors to build hypothetical portfolios using up to 11 major asset classes, and instantly back-test their strategy over hundreds of rolling retirement periods. It illustrates for clients how dramatically diversification has impacted SWRs over the past nine decades.

The Big Picture program relies on the historical performance of indexes and inflation, using monthly frequency total-return data. Monthly data give us a “net” through which to sift history that is three times finer than that offered by quarterly-frequency data. As Bengen and others have noted: Two same-length retirements have, at times, experienced wildly different outcomes – even when they have started just months apart. By capturing more start dates in our sample, we gain deeper insights into historical outcomes.

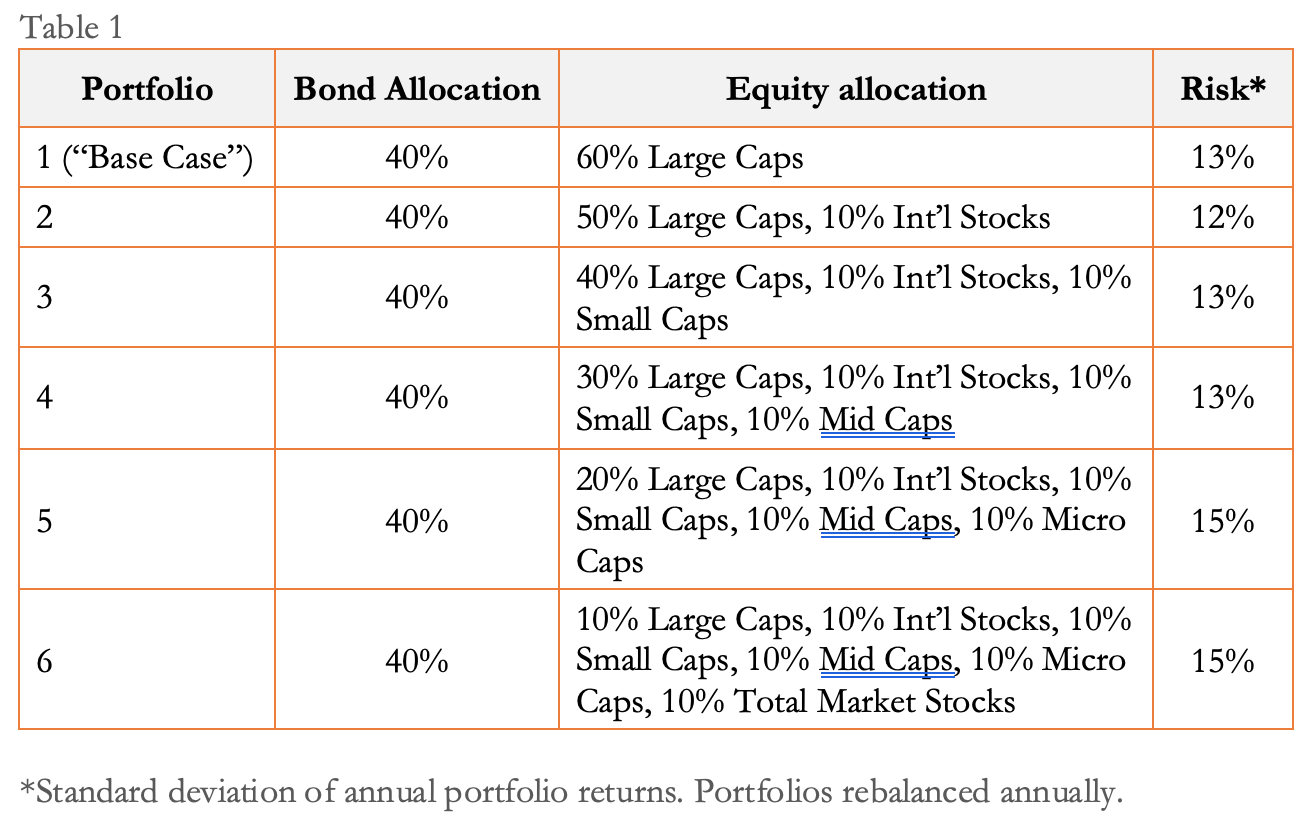

The 11 major asset classes featured in the Big Picture can be used to simulate a near-infinite number of portfolios. Since it would be impractical to test even a small fraction of the possible combinations, a simplified, systematic approach to the selection of test portfolios was needed.

We know that all-equity portfolios have, by some measures, been superior to those containing an allocation to bonds. For example, a portfolio of 100% small-cap stocks has historically supported, on average, higher withdrawal rates than conventional portfolios. However, this outperformance has come at the expense of portfolio stability. Because the volatility associated with all-equity portfolios is unacceptably high for retirees, they were excluded from this analysis.

Instead, I started with a “base case” portfolio of 60% large-cap stocks and 40% intermediate-term government bonds. From there, the bond allocation was held constant while other equity classes were gradually added, diminishing the large-cap allocation correspondingly. For simplicity, new equity classes were added in increments of 10% each. This allowed up to six portfolios to be constructed, with the last one holding six equity classes (plus the 40% bond “anchor”).

Portolio 1, our 60/40 base case, had one equity class. Portfolio 2 had two equity classes. And so on up to Portfolio 6.

The following table describes the composition of the test portfolios:

Of course, adding equity classes in a different order would have produced different results. The above order was chosen to ensure that all portfolios (except Portfolio 1) contained international stocks – a frequently recommended constituent for achieving diversification.

Findings

Safe withdrawal rates

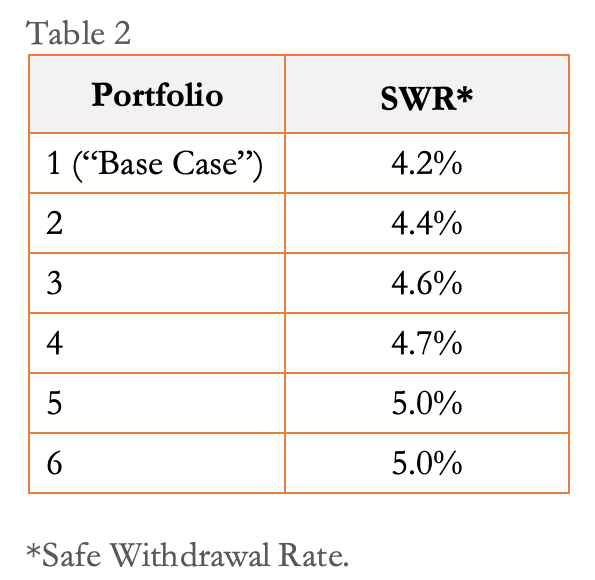

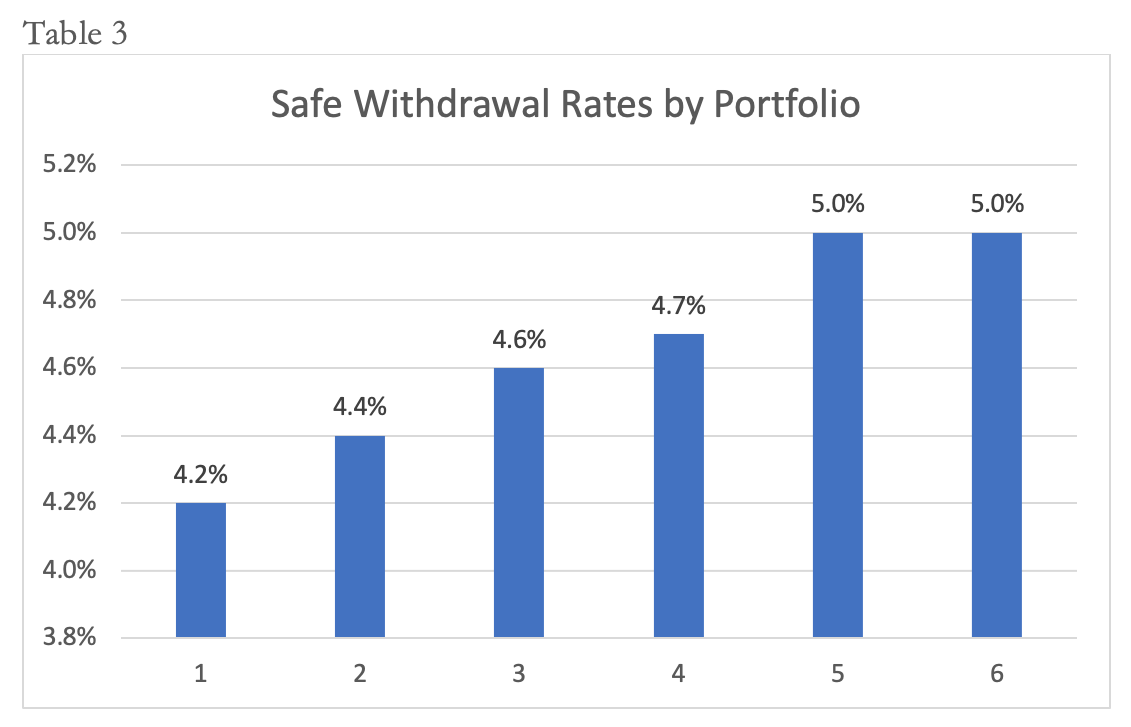

Perhaps retirees’ single greatest concern is their SWR. Did the progressive addition of equity classes boost a portfolio’s SWR and, if so, by how much?

To answer this question, each of our six portfolios was back-tested over rolling 30-year retirement periods (a shorter or longer period could have been stipulated instead). Additionally, a confidence level (i.e., success rate) of 95% was selected. This meant that the software would solve for the highest withdrawal rate that still allowed the portfolio to remain solvent in 95% of historical 30-year periods (in 5% of periods, the withdrawal rate would be too high, and the portfolio would be exhausted before the 30 years were up).

The impact of diversification was remarkable. Portfolio 1 (base case) sustained a 4.2% withdrawal rate in 95% of historical 30-year periods. Portfolio 2 sustained a 4.4% withdrawal rate, while Portfolios 3, 4, 5, and 6 sustained a 4.6%, 4.7%, 5.0%, and 5.0% rate, respectively.

Stated differently, the addition of the first new equity class boosted safe spending by 4.8%, while the addition of the second, third, fourth, and fifth equity classes boosted safe spending by a further 4.5%, 2.2%, 6.4%, and 0.0%, respectively.

The marginal utility to safe spending was greatest with the addition of the fourth asset class (micro-cap stocks), and promptly diminished to zero with the addition of the fifth asset class (total-market stocks). Overall, Portfolio 5 allowed for 19% higher spending than Portfolio 1!

(These results, and all others discussed here, relate to the specific equity classes and weightings tested; adding other types of holdings, or different weightings, would have yielded different outcomes.)

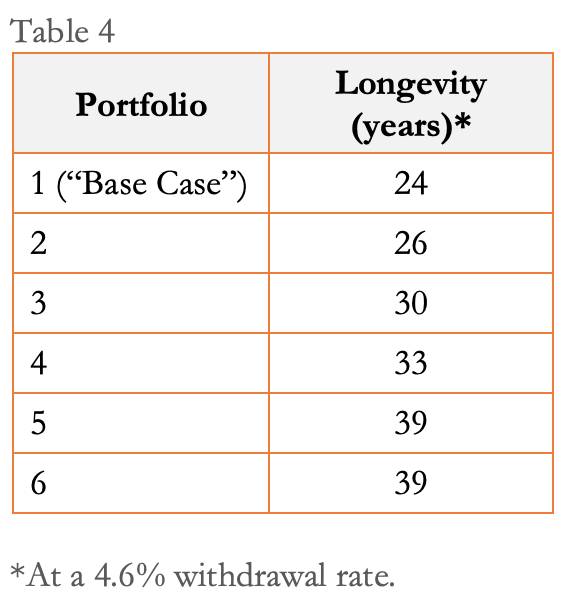

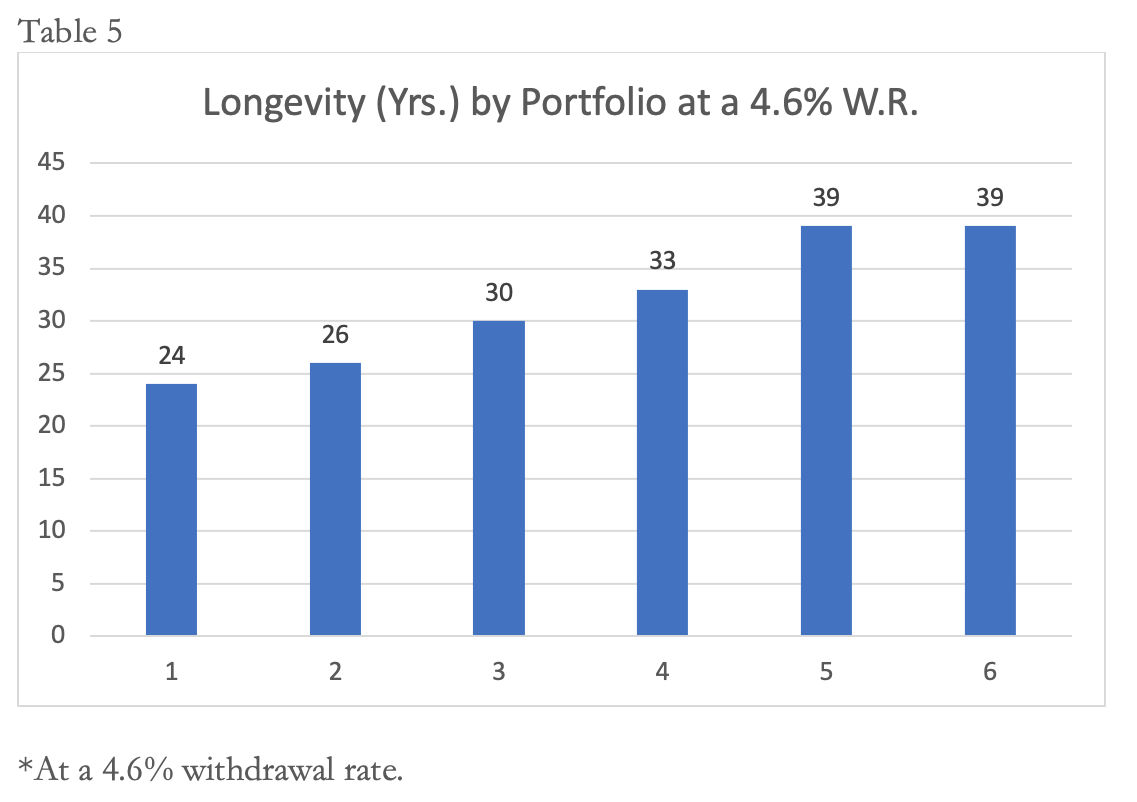

Portfolio longevity

The Big Picture program can back-test over rolling retirement periods of up to 40 years in duration. When solving for portfolio longevity, a standard withdrawal rate of 4%, or even 4.5%, implied longevities of at least 40 years for some portfolios, making them impossible to compare by this metric (the output in these cases appeared as “>40 years”). To draw out differences in longevity across our test portfolios, I therefore set a higher withdrawal rate of 4.6%.

In 95% of historical occasions, it took the longest-lasting portfolio 39 years or longer to be exhausted at this spending level, while it took the shortest-lasting portfolio at least 24 years.

Below are the results across our test portfolios.

Here again, the greatest utility was from adding the fourth new asset class (micro caps), with zero utility from the fifth new class (total-market stocks). Overall, Portfolio 5 lasted 15 years longer than Portfolio 1.

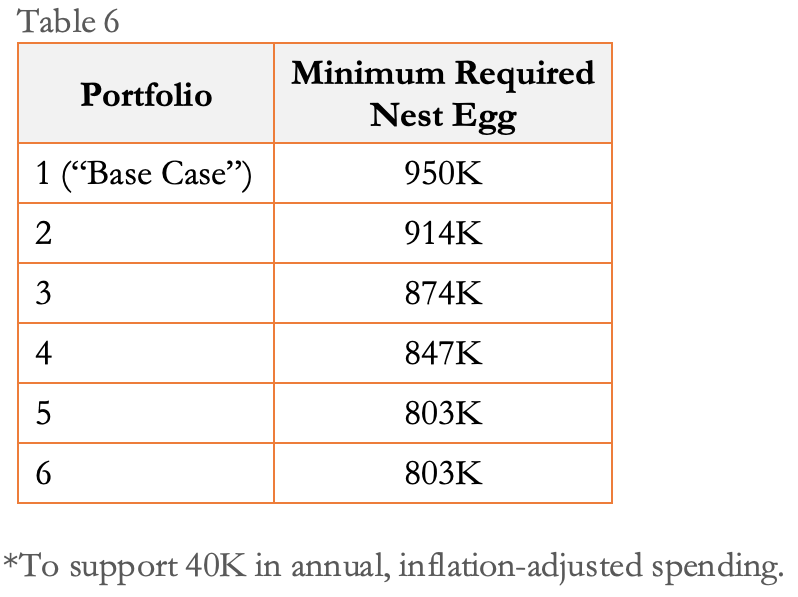

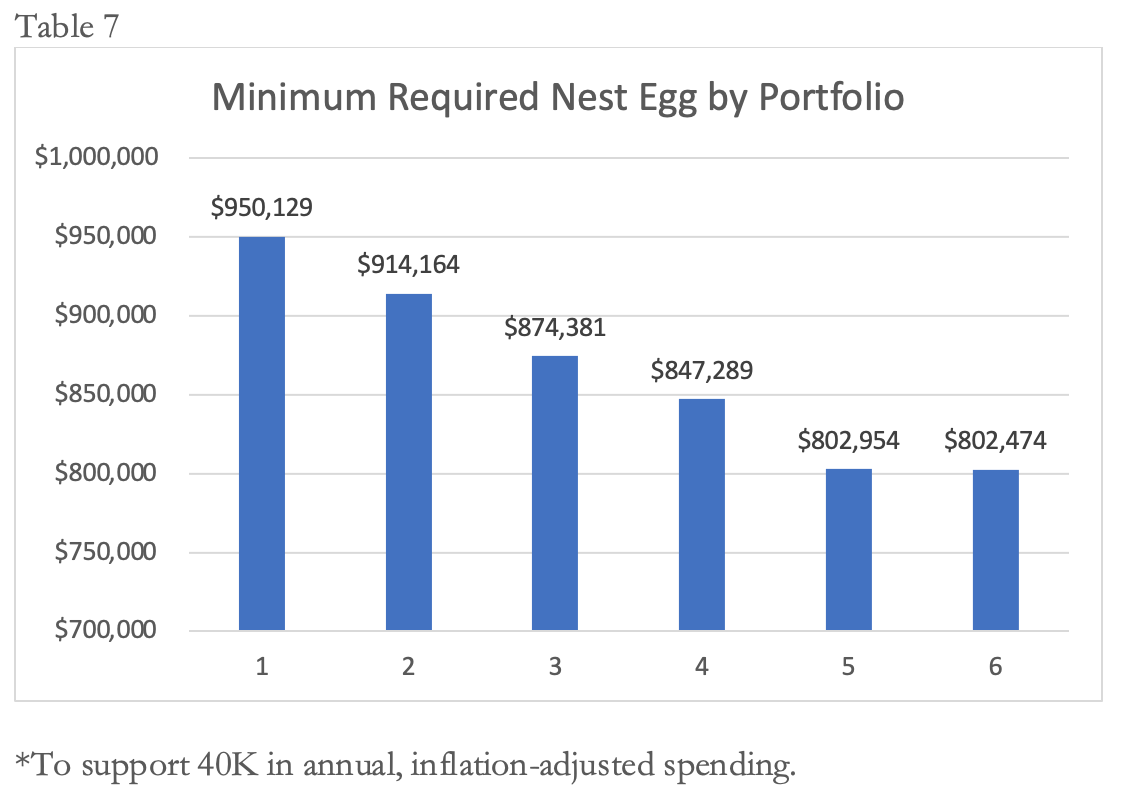

Minimum required nest egg

Provided a desired spending level, asset allocation, and confidence level, the Big Picture can solve for minimum required initial capital. Using the same 95% success rate and 30-year timeframe as above, as well as a required $40,000 in CPI-adjusted annual spending, Portfolio 1 would have needed a starting balance of $950,000. Portfolio 2, meanwhile, would have needed a starting balance of $914,000, and Portfolios 3 through 6 would have needed $874,000, $847,000, $803,000, and $803,000, respectively.

Once again, the greatest utility was conferred by adding the fourth new asset class (micro caps), while adding the fifth asset class (total market stocks) conferred zero value. Overall, Portfolio 5 required $147,000 less in retirement savings than Portfolio 1 – no small sum for the prospective retiree!

More micro caps?

The addition of micro-cap stocks produced the greatest benefit by all of the above measures. Did this benefit derive from micro-cap stocks, specifically, or would the addition of some other novel holding have yielded a similar result? To help answer this, an international bond index was added to Portfolio 5 instead of micro-cap stocks.

The performance of this “Alternative Portfolio 5” was identical to that of Portfolio 3 in terms of its SWR and longevity, and marginally worse than Portfolio 1 in terms of the minimum required nest egg to support $40,000 in spending. In other words, adding international bonds caused a setback.

Portfolio 5’s jump in performance, therefore, seems entirely attributable to micro-cap stocks.

What, then, if even more of this asset class were added instead?

To find out, a second “Alternative Portfolio 5”, containing 20% micro caps, was simulated. Perhaps unsurprisingly, it performed better than any before it. This portfolio offered a 5.2% SWR (again, this was computed at a 95% historical success rate over 30-year rolling retirements) and a minimum required initial investment of just $770,000 (again, to support $40,000 in inflation-adjusted spending). Finally, at a withdrawal rate of 4.6%, this portfolio lasted more than 40 years in 95% of historical periods.

However, this portfolio also exhibited a higher risk level: 17% volatility vs. 15% for the original Portfolio 5 (which contained half the allocation of micro caps) and just 13% for Portfolio 4 (which contained no micro caps).

Conclusion

The strategic addition of asset classes (including international, small-cap, mid-cap, and micro-cap stocks) to a conventional portfolio has yielded meaningful benefits historically, in most cases at little cost to portfolio risk. These benefits are apparent in the form of higher SWRs, greater portfolio longevities, and lower minimum required nest egg balances. The greatest gain was obtained by adding micro-cap stocks; however, their addition caused a relatively significant increase in portfolio volatility. This asset class is worthy of consideration, therefore, by those retirees with a higher risk tolerance and/or supplemental sources of income.

A consideration of diversification is vital to the retiree’s chances of success. I hope the findings presented here, and the Big Picture program itself, will serve as useful material in client meetings.

Ryan McLean is the founder of BigPicApp.co. He worked previously as an equity analyst at Morningstar. He holds an MBA in finance from McGill University.

Historical data range from January 1, 1926 to September 30, 2020.

More Fixed Income Topics >

It’s been my privilege to meet and correspond with William P. Bengen, whose name many will recognize for his pioneering research on safe withdrawal rates (SWRs). In one of our discussions, Bengen noted that the following questions had not been well explored: Is there an optimal number of asset classes for a retirement portfolio, and which are most impactful? Are there diminishing returns to adding more asset classes and, if so, at what point do they reach zero?

It’s been my privilege to meet and correspond with William P. Bengen, whose name many will recognize for his pioneering research on safe withdrawal rates (SWRs). In one of our discussions, Bengen noted that the following questions had not been well explored: Is there an optimal number of asset classes for a retirement portfolio, and which are most impactful? Are there diminishing returns to adding more asset classes and, if so, at what point do they reach zero?