Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Even in an increasingly digital world the financial advisory profession relies on community. Advisors’ clients tend to live within driving distance. The most common methods of building new business are networking and referrals. Even the largest  wirehouses open offices in wealthy cities, rather than blanketing them with digital ads.

wirehouses open offices in wealthy cities, rather than blanketing them with digital ads.

As a result of the coronavirus, the advisory business model has changed precipitously, with two key trends driving this transformation: a shift in the way that consumers are using the internet to find advisors and a surge in consumer comfort with remote technologies.

As the coronavirus struck the U.S. in March, investors went searching for advice. Those who already had a financial advisor asked for advice. Those that did not went looking for answers.

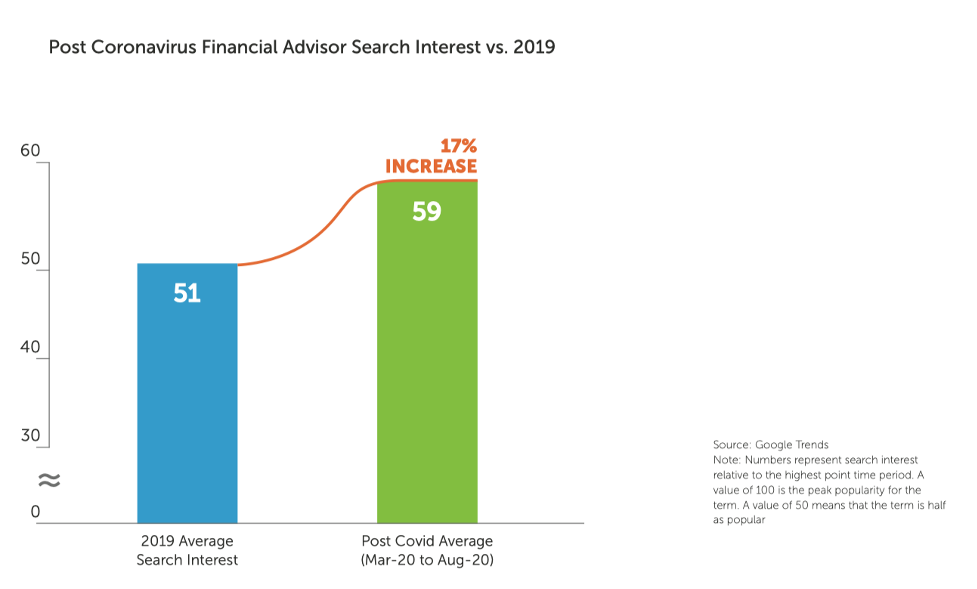

During the first six months of the coronavirus, the searches for the term “financial advisor” increased 17% compared to 2019’s average. With people confined to their homes and facing uncertainty, they realized that they needed advice. According to market research by Facebook, in the early days of the pandemic, 60% of respondents indicated that the crisis evinced a need to be more proactive about financial planning and security in the future.

An emerging digital divide

While it’s clear that investors turned to Google to find a financial advisor when confined to their homes, what’s to stop consumers from going back to their old habits once a vaccine is available?

Some investors will always be open to in-person prospecting. However, those investors are likely to be fewer and harder to reach.

By 2030, Generations X and Y will hold more wealth than Baby Boomers. In addition to soon entering their prime earning years, those generations also display an overwhelming preference for technology: 53% of millennials would seek out a new advisor if their current advisor wasn’t utilizing satisfactory technology. Only 29% of Baby Boomers would do the same.

But moreover, the way we consume is changing. Record numbers of consumers now use digital channels to access entertainment, grocery stores and banking services, many of whom have done so for the first time in the past seven months. The market for telehealth alone grew from a predicted 36 million visits in 2020 to more than one billion visits (and counting) this year.

Once consumers discover that there’s an easier way to do something, they’re unlikely to turn back. According to McKinsey, three-quarters of consumers who use a digital channel for the first time are likely to continue doing so.

Zoom zoom

More than half of us now work from home. And while many of us may relish the thought of getting away for a few days, few are about to relinquish the flexibility we’ve gotten accustomed to.

We won’t have to.

With the rise of virtual meetings, workout classes and even weddings, graduations and birthday parties, the nature of virtual relationships has changed. Pre-pandemic, consumers were comfortable moving the transactional aspects of their banking relationships, like bill payments and transfers, online, but two-thirds still preferred to meet with their advisors in person.

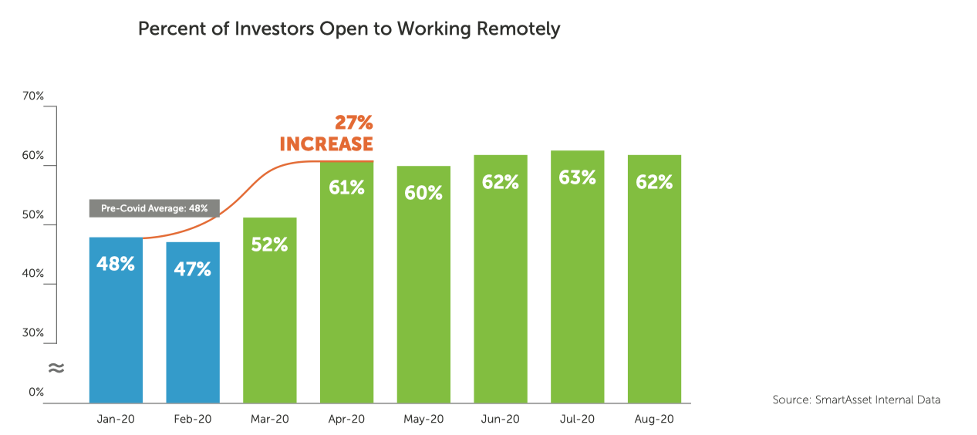

Today, investors are signaling that they can build great relationships virtually. A review of data from SmartAsset’s advisor-matching platform, SmartAdvisor, shows a 27% increase in investors’ willingness to work with an advisor remotely.

Investors have tasted convenience – and they’re unlikely to go back. While some clients prefer to meet in person, 77% of advisors had lost business as a result of not having the right technology to interact with clients. Of advisors’ lost business, the average was one-fifth of their book value.

Where do we go from here?

Firms that invest in marketing, technology and talent during difficult periods are more likely to outperform in the period afterwards.

Investors’ comfort with virtual advice offers an opportunity to advisors to reimagine their practice. Historically, the highest density of firms has been in urban areas, since that’s where the majority of clients were located. Today, advisors who open their practices to virtual clients can expand their potential client base while still managing assets for local constituents. In fact, investors in major coastal cities – with densities of high-net-worth individuals – are even more open to working remotely.

Embracing technology will also help advisors retain clients who still prefer a traditional advising model. According to Cerulli, advisors who are “heavy technology users” have 24% more time for practice management activities.

Advisors’ comfort with virtual meetings also benefits their clients. Investors have more access and choice. Individuals can find an advisor whose niche focus, investment philosophy or personality meets their needs, rather than being tied to the choices dictated by the physical proximity of their advisor’s office.

Firms that pursue a virtual new business strategy will need to be more aggressive in their marketing efforts, especially in markets where they do not have a physical presence. Locally focused firms have the benefit of word-of-mouth referrals and individual advisors’ reputations in the community. Remote-first firms need to centralize their marketing efforts and develop a brand that is recognizable to prospective clients. A firm’s reputation and brand will be the key to convincing prospects to agree to the first conversation with an advisor.

Chris Sonzogni is director, advisor marketing with SmartAsset, a technology company that provides personal finance solutions.

Read more articles by Chris Sonzogni

wirehouses open offices in wealthy cities, rather than blanketing them with digital ads.

wirehouses open offices in wealthy cities, rather than blanketing them with digital ads.