Clients are surprised when I request copies of their tax returns. But when they see the process I use to save them money – tax “alpha” – they often wish April 15 came more often.

Clients are surprised when I request copies of their tax returns. But when they see the process I use to save them money – tax “alpha” – they often wish April 15 came more often.

I explain to them that reviewing their returns is mandatory. Though, for security purposes, they must redact their Social Security numbers. I need the tax return to better design the plan. You don’t have to be a CPA to provide a ton of actionable and measurable results that add critical value to your clients.

Here are five areas to help clients and add that tangible and immediate value:

-

Make the most of clients’ past losses. Do they have a capital loss carryforward? With markets nearing all-time highs again, you’d think this would be fairly rare, yet it’s not. I regularly see clients with huge tax-loss carry forwards and this provides two key insights. I ask where the loss came from. That can shed light on possible poor behavior such as panicking and selling during past bubbles. I suspect I’ll see some losses in more than a few 2020 tax returns for those who sold during the brief March bear market. I advise clients that their past behavior is a far better predictor of the decision-making than any risk profile questionnaire. Understanding the loss is critical for determining how much risk a client should and can take.

Second, if the client has a loss then it opens up possibilities to exit investments with high fees or that are otherwise undesirable, such as concentrated positions. I jokingly tell the client, “I’m sorry for your loss but let’s make the best of it.” I estimate how much in gains can be recognized without paying any federal income tax. That’s not to say I’ll use all of it up, because that loss carryforward has value in future years. And, of course, any unrealized losses can also be sold and used to offset gains or add to the tax-loss carryforward.

2. Take control of their recognized capital gains. On the opposite side of the spectrum from loss carryforwards are the gains that the client is recognizing. Sometimes this shows frequent trading. But, more often it’s due to tax-inefficient vehicles. As you know, when a mutual fund trades and recognizes a gain, it pushes out that gain to the client via a 1099. Sometimes I see a fund pushing through short-term capital gains. To make this worse, I’ve seen many times when the fund has a negative return but still passes on taxable gains.

I look at the recognized gains by fund in the client’s schedule D to see how much each holding has passed through in gains with a particular eye as to whether or not a fund is in a death spiral. This happens when a once strong-performing fund suddenly underperforms for multiple years. A recent example is the client who held a large position in the Sequoia mutual fund (SEQUX), which they had for decades. It had been a legendary performer until it bet heavily on Valeant Pharmaceuticals. It exited Valeant, but Morningstar shows underperformance since 2014. This caused investors to sell the fund and Sequoia to sell stocks to meet investor redemptions. The sale of the stocks caused large realized capital gains and, since November 16, 2015, it has passed on $110.69 a share in recognized capital gains to those who remained. In another example from a few years back, the Columbia Acorn Select Z (ACTWX) was in a death spiral but did go extinct. This analysis shows me when to recommend immediately selling the fund rather than hold on to the dog and still pay the capital gains taxes over the next few years.

-

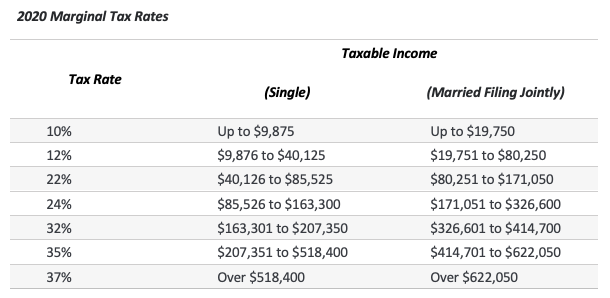

Manage to marginal tax-rates. Investment decisions have tax consequences. To the extent we can manage the tax brackets below, we add value. For example, we can manage how much of a Roth conversion the client should do. I typically recommend using up the 10% and 12% marginal bracket and frequently using up all of the 24% bracket. You can also assess how much benefit the client is getting from owning municipal bonds. And don’t forget state income taxes if the client is domiciled in a state that has income taxes.

Understanding marginal tax rates on capital gains is also critical. How much long-term gain can be recognized before the client hits the federal 20% marginal tax rate (income over $441,450 single and $496,600 married filing jointly - MFJ)? Even if they are in the 15% marginal rate, are they being hit with the 3.8% net investment income tax (income over $200,000 single and $250,000 MFJ)? Often the client can spread the gain over a couple of years. On the opposite side of the spectrum, can a retired client recognize a long-term gain at a zero percent tax rate? This is known as tax-gain harvesting.

-

Assess the benefit of debt. I’ve noted for well over a decade that a mortgage is virtually the inverse of a bond. If the client has enough liquidity, it rarely makes sense to borrow money at a higher after-tax rate than the rate it is loaned out at. Look at the clients’ itemized deductions in schedule A. In fact, the Tax Cuts and Jobs Act caused an estimated 90% of tax filers to take the standard deduction and not itemize at all. That gives them a zero tax benefit.

Yet a itemizing still usually results in a large part of the mortgage interest providing no benefit. Let’s take a couple filing jointly that has the maximum $10,000 in SALT deductions and $20,000 in mortgage interest at a 3% rate. They had $30,000 in itemized deductions, but that’s only $5,200 above the $24,800 standard deduction. Only a bit over a quarter of that mortgage interest provides any tax benefit. The client will be paying taxes on their bond funds (unless they are munis, which have credit risk) and possibly the 3.8% net investment income tax.

If one has an investment property with a mortgage, they don’t need to itemize. But often I tell the client to pay the mortgage off anyway. That’s because it increases the net income from the investment, which often qualifies for the 20% qualified business income deduction.

Though neither of these moves gives a short-term benefit to AUM-based advisers, in the long-run, they show the client you are acting in their best interests; it is something that clients will tell their friends and family.

-

Make charitable contributions the right way. Because our clients are generally high-net worth, they tend to be generous, making contributions to their favorite non-profit 501©3 organizations. Typically I see the client making cash contributions and getting little to no tax benefit. Look in schedule A, line 11, “Gifts by cash or check.”

I advise clients that they can do this in a more tax-efficient way and still provide the same benefit to the charity. Make large, lumpy donations of an appreciated security to a low-cost donor advised fund (DAF) and do so every few years rather than annually.

Take, for example, a couple that has $10,000 in SALT deductions and $15,000 in charitable contributions. They itemize with $25,000 in deductions, but that’s only $200 more than the standard deduction, so they get virtually no benefit. If, instead, they donated five years at once by taking a security with a large unrealized gain (such as the Sequoia fund mentioned earlier) and donated $75,000 to the DAF in year one, they get a tax benefit on $60,200 of that amount (limitations on gifting appreciated property apply). The appreciated security can then be sold in the DAF without taxable consequences. Then, over the next five years, the client can have the DAF give to that same charity.

This gives them both tax savings from avoiding taxes on those unrealized gains and getting a much greater tax-benefit from the gift itself. And you get a bonus for the client if they have such an underperforming investment with a big gain.

Those are only some of the ways you can provide tax “alpha” to your clients. Another example is using a health savings account (HSA) or a Roth. I often tell clients to max out their HSA contributions but pay for medical costs from taxable money. They can then keep the receipts and reimburse themselves tax-free decades later.

Tax alpha is real and building tax-efficient portfolios and strategies from the client’s current portfolio is a better way to add alpha than trying to beat the market. No robo-advisor could ever hope to do these things. They construct a portfolio from scratch, ignoring the consequences of selling everything in the current portfolio.

For new clients (and even existing ones), look at their tax return and work with their CPA. The CPA can often easily run scenarios, such as the impact of recognizing specific gains. That’s a value added your client may have never experienced before. It will impress the client and their CPA, and possibly result in referrals from both.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth

Clients are surprised when I request copies of their tax returns. But when they see the process I use to save them money – tax “alpha” – they often wish April 15 came more often.

Clients are surprised when I request copies of their tax returns. But when they see the process I use to save them money – tax “alpha” – they often wish April 15 came more often.