Volatility Trading in the COVID-19 Era: Shaken not Stirred

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

While the world focuses on COVID-19, there’s another virus that’s getting far less attention – the volatility virus. Investors and traders who embrace and capitalize on volatility (or “vol”) are jumping into indices that track volatility. And 2020 is surely the year to do so.

The financial markets this year have experienced profound volatility that will likely carry over into 2021. Years like this one don’t come around that often: pandemic, trade wars, civil unrest and a U.S. presidential election. Each one is enough to heighten volatility, but all together translates to turbulent markets that are not just stirred, but violently shaken. In fact, 2020 began with unemployment at a 50-year low (3.6%) and by April, was the highest in 90 years (14.7%).

When uncertainty and instability reign supreme, it’s prudent to rely on experts best suited for the job. When looking for a vaccine for COVID-19, leave it to the top cellular and molecular scientists. When breaking an international narcotics ring, James Bond is your man. And when trading volatility-lined products, leave it to the experts.

Many trips, few triumphs

Market volatility has been widely followed and traded since the 1980s. The primary method of tracking volatility has been through the Cboe S&P 500 Implied Volatility Index (VIX), often referred to as the market’s “fear gauge.” The VIX measures the implied volatility of S&P 500 index options. It represents an expectation of market volatility and an indication of investor sentiment.

While the VIX is not a traded entity itself, the Cboe introduced VIX-linked products by launching VIX futures in 2004 followed by VIX options in 2006. While many retail traders chose not to trade futures or options, the launch opened the door to tradable VIX securities packaged into exchange-traded products (ETPs) including exchange traded funds (ETFs) and notes (ETNs)i. These second-generation volatility products, introduced in 2009 (some inverse, some leveraged) were not designed to replicate the VIX itself, but rather the futures indices on the VIX. They opened volatility trading to a broad audience and firmly established volatility as an asset class.

Trading volatility has risks.

One can trade vol through options and derivatives, but using less expensive and ostensibly less complex ETPs sounded promising. In February 2018, many zealous volatility traders piled into an overcrowded inverse VIX product (XIV), causing a massive selloff and its eventual implosion, known as “Volmageddon.” Since then, not only has the introduction of new volatility ETPs been dialed down precipitously, but many have since closed. Today there are approximately 26 VIX-linked ETPs.

Fast forward to 2020. COVID-19 ended the 11-year bull market that began in March 2009, the longest on record. The ”corona crash” was sharp and fast (February 19-March 23) with the S&P losing 34% – – all its 2020 gains. By June 8, the market miraculously recovered in full, fueled by hopes for a quick economic recovery, historic Federal Reserve intervention and a disregard for the major risks ahead. By June 10, the market came to a screeching halt from worries over a second coronavirus wave and a cautious Fed outlook.

Pass the Chain Saw

It would be sorely irresponsible to put a chainsaw in the hands of a novice. The same theory applies to trading VIX-linked products. A common and dangerous misconception is that to profit from volatility, one can simply buy a volatility index like the Cboe’s VIX index (VXX), betting long-only when volatility is strengthening, and sell the VIX when volatility has seemingly topped out. But that’s hardly the case and embraces the harsh risk of market timing.

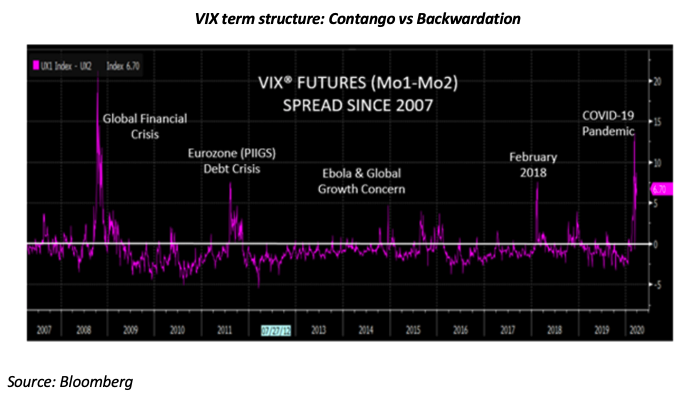

For one, the VIX futures term-structure (forward curve) makes positions in VIX-ETPs unsuitable for buy-and-hold investment due to negative-expected returns. VIX futures trade like commodity futures, which are priced along a forward curve from today (spot) into the future. Each curve is based on market expectations of the underlying contract at various points along a timeline. Where VIX is the volatility over the next 30 days, VIX futures represents the expectation of the volatility 30 days from now.

The VIX futures curve is typically upward sloping (contango), meaning shorter-dated VIX futures trade at a discount to longer-term ones. The shape represents greater expectations of market volatility in the future attributable to “headline” risk – the uncertainty of what tomorrow may bring. Most investors are risk-averse and thus willing to pay a premium for VIX exposure as it represents insurance against equity market losses. The curve rarely inverts to downward sloping (backwardation), as seen in the first chart below, unless volatility is exceptionally high and deemed unsustainable (such as now). Today’s curve barely resembles its shape from one year ago (the chart on the right). In either case the curves are rarely smooth, only exacerbating the difficulty in trading the VIX.

Even with volatility increasing, a long position will lose value in contango, as there is a cost (roll yield) to roll the futures contract forward by selling the near-term futures and buying a forward month contract. A position in the VIX would have lost 99.5% of its value if opened in January 2009 and held to April 2014ii. This scenario is not unique to the VIX-ETF and can occur with other futures-linked ETFs. One example is natural gas, whereby bullish investors flocked to the gas ETF, only to lose vast amounts of capital – even while the price of gas was rising.

Who is better to ask about the VIX than the inventor himself, Professor Robert E. Whaley of Vanderbilt University? Whaley, who created the VIX for the Cboe in 1993, points to its “misconception.” “The VIX is nothing more than a put option on the SPX. You buy it like an insurance policy when you think the market is going to collapse. It’s as if you had a house on the coast and hear about an impending storm.” Adds Whaley, “what the VIX represents – expected future volatility – is loosely true and is a biased view due to asymmetry. You don’t buy insurance that the market will go up! It lacks that symmetry.”

Since 2005 there have been only four short periods when the VIX roll yield was greater than 1%: the financial crisis in 2008, the “AAA” US credit downgrade of 2011, the threat of inflation in February 2018 and now, from COVID-19, the longest persistent backwardation since 2008.

Secondly, coupled with the infrequency of backwardation is its short-lived nature – at most a few months. “In a backwardation”, adds Whaley, “the curve shows that people are scared for the next 30 days but not as nervous for the next 60-90 days and are paying up for that short -term protection.” Selling the VIX index short in those brief periods is dangerous, particularly when the curve rapidly snaps back to contango.

Promoters of VIX futures and ETPs point to their diversification benefits for investors like pension and mutual funds. But instruments for diversification are only effective when that instrument is understood.

Of loggers and volatility traders

As for trading volatility, the chainsaw rule holds true. Yet, there are few volatility vehicles available for the retail investor, and the majority are long- or short-only but not actively managed long or short funds.

A long/short tactical strategy requires precise timing of when to buy or sell vol, or alternatively, remain in cash.

Trading volatility through VIX-ETPs can be a highly profitable trading strategy if executed with the right tools and risk management. VIX-ETPs are sophisticated products. Many retail traders don't have the basics to understand them and lack an algorithm to time exit and entry. Good traders are hard to come by and choosing them demands robust due diligence – somewhat like discovering the next James Bond.

Shelley Goldberg was a commodities strategist for Brevan Howard Asset Management and Roubini Global Economics, a hedge fund manager for G3 Capital Partners and a contributing writer to Bloomberg Opinion.

i ETNs are unsecured debt obligations whereas ETFs are backed by a pool of assets.

ii [ii] “VIX Exchange Traded Products: Price Discovery, Hedging, and Trading Strategy”, Christoffer Bordonado, Peter Molnar, & Sven R. Samd, Journal of Futures Markets, May 2016, page 19

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All