Investors underestimate the negative consequences of high environmental, social and governance (ESG) risks, and underreact to prior negative ESG events. High ESG risks destroy shareholder value.

Investors underestimate the negative consequences of high environmental, social and governance (ESG) risks, and underreact to prior negative ESG events. High ESG risks destroy shareholder value.

To appreciate the significance of this finding, consider that, over the past decade, there has been an accelerating increase in ESG investing strategies. In fact, ESG investing in its various forms (such as SRI, or socially responsible investing) now accounts for one out of every four dollars under professional management in the United States and one out of every two dollars in Europe. And the trend seems poised to continue. The Global Sustainable Investment Alliance 2018 Review, which covers the five regions of Europe, the United States, Canada, Japan, and Australia and New Zealand, showed that sustainable investing assets in those major markets stood at $30.7 trillion at the start of 2018, a 34% increase in two years. And responsible investment commanded a sizable share of professionally managed assets in each region, ranging from 18% in Japan to 63% in Australia and New Zealand.

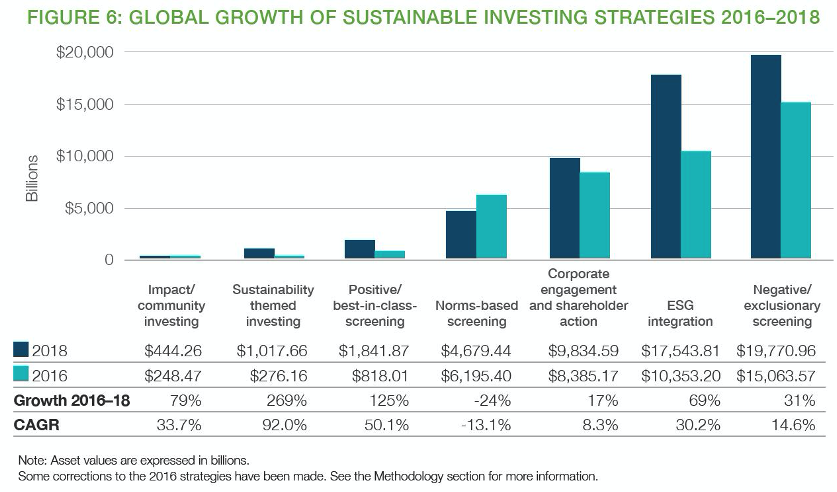

The following table from the report shows how investor assets are allocated across various ESG strategies. he largest share is still in negative/exclusionary screening (the exclusion from a fund or portfolio of certain sectors, companies or practices based on specific ESG criteria) as opposed to ESG integration (the systematic and explicit inclusion by investment managers of environmental, social and governance factors into financial analysis).

The report also noted that, “the leading motivation, based on the number of money managers citing it and the assets they represent, is client demand.” Among the other main motivations cited were the desire to achieve social and environmental benefit or to fulfill their firms’ missions.

Increased investor interest has not only led to cash inflows but to heightened interest in research on ESG investment strategies and the impact of those cash flows on returns. The hypothesis is that the incorporation of ESG characteristics in investment decisions can impact expected returns by reflecting investor preferences or by loading on some underlying risk factor. Either way, they suggest a likely ESG premium on expected returns because lower demand should lead to systematically lower valuations. And even if responsible firms encounter higher operating costs, investors’ preferences for ESG may make them willing to invest in such firms despite lower expected returns.

In general, the research confirms financial theory. Studies such as “The Contributions of Betas versus Characteristics to the ESG Premium,” “A Sustainable Capital Asset Pricing Model (S-CAPM): Evidence from Green Investing and Sin Stock Exclusion,” “Outperformance through Investing in ESG in Need” and Is ESG an Equity Factor or Just an Investment Guide?” have found that firms with lower ESG scores exhibit higher expected returns. However, as the authors of the study, “Sustainable Investing in Equilibrium” noted, the heightened interest in ESG investing has led to firms with high ESG scores having rising portfolio weights, leading to short-term capital gains for their stocks – realized returns may rise temporarily, though expected long-run returns fall.

On the other hand, there have been some studies, such as “ESG Investing: From Sin Stocks to Smart Beta,” which have found that ESG exclusion does not lead to deterioration of risk-adjusted performance. However, the study also found that ESG exclusion does lead to regional and sectoral tilts as well as (possibly undesirable) risk exposures of the portfolios, including underweighting small and value stocks, both of which have provided premiums historically.

An interesting approach to analyzing the performance of ESG investing was taken by Simon Gloßner, author of the November 2017 study “ESG Risks and the Cross-Section of Stock Returns.” He used data on ESG risks provided by RepRisk, which since 2007 has screened thousands of information sources (e.g., print and online media, NGOs [nongovernmental organizations], government bodies) on 28 predefined ESG issues, such as environmental pollution, human rights violation or fraud. “This collection of ESG issues is then used to calculate an ESG-related reputational risk exposure score, the RepRisk Index, for each firm in the sample. In this process, RepRisk distinguishes major from minor issues, based on the severity, reach, and novelty of an issue. The RepRisk Index ranges from 0 to 100. A higher number denotes a higher ESG risk: An index value between 0-25 indicates a low risk, 26-50 a medium risk, 51-75 a high risk, and 76-100 a very high risk. … A firm has a high ESG risk exposure when its RepRisk Index reached values of larger than 50 over the past two years, indicating that the firm had many and severe ESG issues.”

Gloßner created a portfolio of the stocks with RepRisk scores with a two-year peak RepRisk Index of larger than 50. In other words, instead of analyzing whether firms “do well by doing good,” his study asked whether doing bad destroys shareholder value. Unfortunately, his data set is only available for the short period 2009 through 2016. There were 38 firms with high ESG risks in December 2010, and 95 firms (mostly large cap, with median market cap of $49 billion) with high ESG risks in December 2014. Following is a summary of his findings:

- In December 2014, the most common industries of the 95 firms with high ESG risks were banking (9 firms), pharmaceutical products (8), retail (8), business services (7), and petroleum and natural gas (7). Note the absence of the three “sin” industries of tobacco, alcohol and gaming.

- Negative ESG events are associated with significant negative abnormal returns over the short term (21 days). For example, an increase in the RepRisk Index of larger than 10 points has a significant negative abnormal return of 0.40%. If the RepRisk Index increases at least by 30 points (indicating more severe ESG issues), the negative abnormal return exceeds 2%.

- Firms with high ESG risks have more ESG issues in the next year than firms with low or medium ESG risks – there is persistence in ESG scores.

- Firms with high ESG risks have significantly weaker operating performances (based on four different ratios: return on equity, one-year sales growth, net profit margin and return on assets), more negative earnings surprises, and more negative earnings announcement returns than peers. The abnormal returns of the earnings announcements explain about half of the negative alpha of the U.S. portfolio with high ESG risks.

- A capitalization-weighted U.S. portfolio of firms with the worst histories of ESG issues is associated with negative abnormal return of about 3.5%, statistically significant at the 1% confidence level.

- A similar European portfolio (44 firms) exhibits significant abnormal returns of between 2% and 4%. The negative alphas are significant at the 5% level with the Carhart four-factor European model, and at the 1% level with an eight-factor world model. This provides out-of-sample support for the U.S. findings.

- Robustness checks confirm that the abnormal returns of these firms are not the result of common risk factors: the underperformance stems from underperforming industries, negative outliers, weak profitability, weak corporate governance, or many other firm or stock characteristics.

Gloßner provided two explanations for the negative alphas. Despite the evidence demonstrating persistence in ESG scores, “investors are negatively surprised when firms with high ESG risks have new ESG issues.” This indicates that investors underestimate the persistence of weak ESG scores. Second, “firms with high ESG risks have significantly weaker operating performances, more negative earnings surprises, and more negative earnings announcement returns than peers.” He added that because the stock markets do not fully capitalize the negative consequences of intangible risks, his findings provide “a socially responsible investment strategy that is also profitable – short U.S. or European firms with a notable history of ESG issues.” Alternatively, investors could screen them out of eligible universes – the negative/exclusionary performed currently by many, if not the majority, of ESG funds today.

While Gloßner’s finding that investors underreact to negative past ESG events conflicts with the efficient market hypothesis, it is consistent with the literature from the field of behavioral finance. The basic hypothesis of behavioral finance – the study of human behavior and how that behavior leads to investment errors, including the mispricing of assets – is that due to behavioral biases, investors/markets make persistent mistakes in pricing securities. An example of a persistent mistake is that investors underreact to news – both good and bad news are only slowly incorporated into prices, resulting in the momentum anomaly. The explanations for underreaction include optimism, anchoring and confirmation biases, each of which can cause investors to underweight or ignore contrarian information. The literature also demonstrates that anomalies often occur in intangibles (such as accruals, R&D research and patents) – and ESG risks are intangible risks.

The publication of his findings could eliminate the anomaly, as the evidence clearly shows that there are persistent risks when investing in firms with the worst ESG histories. However, there are limits to arbitrage that can prevent sophisticated investors from correcting mispricings, allowing anomalies such as Gloßner found to persist. It’s also possible that at least some of the negative alphas he found were due to cash flows away from stocks with high negative ESG scores, leading to their short-term underperformance. However, the cash flows could not explain the negative surprises in earnings.

Summary

Gloßner’s findings provide valuable information for constructing portfolios. They also provide another example of how markets are not perfectly efficient, and how anomalies can persist due to behavioral errors investors persistently make and the presence of limits to arbitrage. It will be interesting to see if his findings will continue to hold up post-publication.

For those interested in learning more about ESG, I recommend a paper by McKinsey & Company titled “Five Ways ESG Creates Value.” The authors’ experience led them to believe that ESG links to cash flow in five important ways: (1) facilitating top-line growth, (2) reducing costs, (3) minimizing regulatory and legal interventions, (4) increasing employee productivity, and (5) optimizing investment and capital expenditures.

Larry Swedroe is the chief research officer for Buckingham Strategic Wealth and Buckingham Strategic Partners.

More Energy Topics >

Investors underestimate the negative consequences of high environmental, social and governance (ESG) risks, and underreact to prior negative ESG events. High ESG risks destroy shareholder value.

Investors underestimate the negative consequences of high environmental, social and governance (ESG) risks, and underreact to prior negative ESG events. High ESG risks destroy shareholder value.