Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In a low-yield environment, advisors need to use financial planning tools like no-commission annuities to improve after-tax, after-advisory fee bond returns.

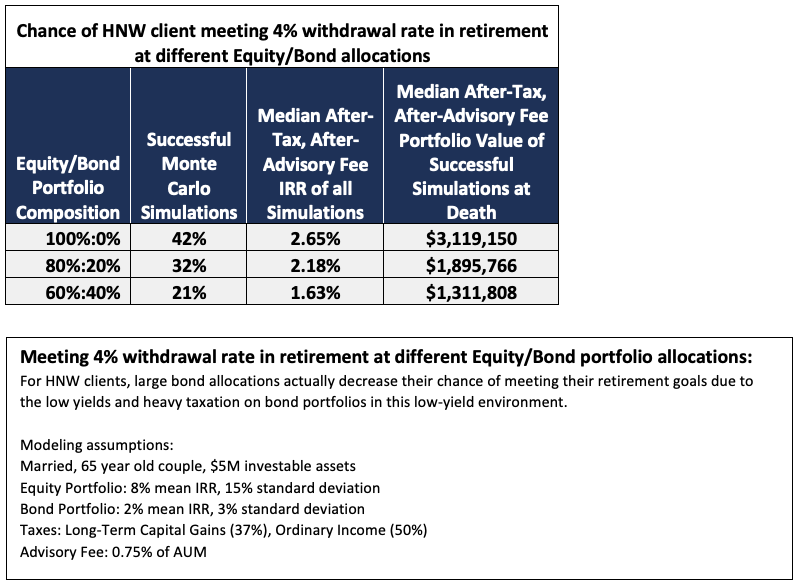

A large bond allocation has long been the staple diversification tool for advisors to hedge market risk in their equity portfolios – especially for clients nearing retirement. In high-yield environments, this is an excellent tool. Advisors can either hold the bonds to maturity and benefit from the high fixed income yield, or they can sell the bonds as yields decrease, thereby allowing for capital appreciation on the assets. In a high-yield environment, bonds are great assets by themselves, independent of the diversification benefits they provide.

But in a low-yield environment, the value proposition is the opposite.

Low yields don’t justify the AUM fees advisors charge on them. Furthermore, the high ordinary income taxes owed on bond gains makes the net, after-tax, after-advisory fee yields for the client abysmal – particularly if this client is the ideal HNW client in a high tax bracket. In the low-yield environment we’re in, after the client pays taxes and fees, he or she makes significantly less for owning the asset and taking all the interest, credit, and liquidity risk than the RIA earns for managing them.

As a result of this low-yield, high tax-rate dynamic, clients have a better chance of meeting their retirement goals (and passing more money to the next generation at death) using a 100% equity strategy than a 60% equity/40% bond strategy.

Retirement solutions

What strategy addresses the high taxes and lack of diversification that bonds pose in a low-yield environment?

One strategy is asset location, which is to put all of the client’s bonds and tax-inefficient equity strategies into retirement funds like 401(k)s or traditional/Roth IRAs. Retirement accounts allow for two key benefits for advisors and their clients on the bond portion of client portfolios:

- Earnings grow tax-deferred or tax-free.

- Advisors can charge fees on a pre-tax basis instead of on an after-tax basis, thereby reducing the tax liability of client and increasing the client’s after-tax return.

As the table below shows, an advisor charging an AUM fee on client bond portfolios on a pre-tax basis can more than double the client’s net after-tax, after-advisory fee return in this low-yield environment!

Unfortunately for HNW clients, they are often limited by their high-income from contributing to these tax-beneficial retirement plans which can improve after-tax bond gains. A workaround for such HNW clients is to use no-commission fixed and indexed annuities to invest millions of dollars into a vehicle that allows the same tax-deferral and pre-tax advisory fee benefits as a traditional IRA with the added bonus of interest-rate risk protection. The interest-rate protection allows for annuities to achieve higher yields than short-term bonds without the interest rate risk associated with long-term bonds. This is particularly valuable in this low-yield environment.

As I’ll show below, clients would be better off having their financial advisor allocate their bond assets to a no-commission annuity and have their advisor charge their AUM fee on the assets than to have that same advisor allocate their bond portfolios to short- or intermediate-term bonds directly.

However, most advisors have a strong aversion to annuities because of poor experiences with past products that paid agents high commissions and left limited benefit to the client.

Most advisors don’t realize that, at their core, fixed and indexed annuities are investments in tax-deferred investment-grade long-term bonds that provide clients protection against interest rate risk. In exchange for providing these tax-deferral benefits and interest-rate protection, life insurance companies that issue annuities earn a spread on what those long-term bonds are earning versus what they credit to policy owners. When you remove the high-upfront commissions on these products, the after-tax return clients achieve by using these annuities is notably higher than what they would earn by investing in the bonds directly.

Even the pre-tax payout rates of these annuities are highly competitive with pre-tax yields of the underlying bonds as the table below shows.

Sources: Annuity Rate Watch, iShares

The table above highlights a number of important points:

1. The intermediate-term AGG bond index has a lower yield than its longer-term IGLB counterpart. However, while advisors can achieve a higher yield by investing in longer-term bonds, they are also taking more interest rate risk. If interest rates rise over the time their clients are holding the bonds and they try and exit the investment, their clients will lose part of their principal. Given the low-interest rate environment we’re in, this is a real concern for investing in long-term bonds.

For this reason, advisors increasingly allocate clients to lower yielding, shorter term bond funds over longer ones.

2. Both the commissionable and non-commissionable annuities have higher pre-tax payout rates than the AGG and lower long-term payout rates than the IGLB.

This makes sense given that the insurance company is investing in long-term bonds and taking the interest rate risk in exchange for a spread. The client won’t get a pre-tax yield as high as investing in long-term bonds directly, but they will be saved from the interest rate risk involved from investing in long-term bonds. The pre-tax payout rates of both annuities are higher than the intermediate-term AGG bond fund that advisors would have invested in directly to avoid the interest rate risk of the long-term bond fund.

3. The no-commission annuity had higher pre-tax payout rate and a higher cap on the index than the commissionable product from the same company.

As mentioned previously, by removing the upfront commission paid to an insurance agent, the insurance company is able to provide a much better product to the client. The client is better off having their financial advisor invest in the no-commission annuity as opposed to that advisor allocating that client to an intermediate-term bond index like the AGG. While the client could achieve higher yields from investing in long-term bonds directly, they would also be taking the full interest rate risk of those bonds.

4. The client is better off investing in bonds through a high-commission annuity and paying a one-time upfront commission than investing in the AGG through an advisor and paying an ongoing AUM fee.

For advisors who critique annuities as not being in the best interests of the client, the above table shows that the pre-tax payout rates on the commissionable annuity outperform the standard AGG allocation on a pre-tax basis – without even considering the tax benefits. Furthermore, the client investing in the AGG through the advisor would have to pay an AUM fee on the assets on an ongoing basis, which would further reduce the client’s yield every year.

The client is better off purchasing a highly commissionable annuity as a vehicle to invest in bonds and paying a one-time high upfront commission than they are hiring a fiduciary advisor to invest those assets in a low-yielding bond while charging a high ongoing AUM fee relative to low-yielding assets.

Summary

No-commission annuities offer clients the ability to achieve better after-tax, after-advisory fee solutions than current bond strategies. Furthermore, annuities are clearly products that clients want. Over $200 billion dollars was invested in fixed and indexed annuities in 2019 alone.i This is potential AUM that these advisors are missing out on.

The problem is that most fixed and indexed annuities are the high-commission ones that have lower payout rates and index caps. If fiduciary advisors truly understood how to utilize no-commission annuities, they would be able to provide better retirement products and risk-adjusted, after-tax, after-advisory fee portfolio solutions to their clients and grab a larger portion of this market share they’re missing out on.

If advisors don’t start implementing better after-tax, after-advisory fee solutions for clients’s bond portfolios, clients will quickly do the math and do one of two things:

- Just let advisors manage the equity portion of the portfolio and stick the bond portion of the portfolio in a low-cost bond index fund themselves to avoid paying the advisor’s fee on this portion for limited value they receive in return.

- Take all of their assets to an advisor that is implementing better after-tax, after-advisory fee solutions for them for their entire portfolio.

Rajiv Rebello, FSA, CERA is the chief actuary of Colva Actuarial Services. Colva helps RIAs implement fee-only insurance, annuity, and alternative investment solutions to help provide better portfolio diversification and risk-adjusted after-tax returns in a low bond-yield environment.

i LIMRA.

Read more articles by Rajiv Rebello

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.