Reversing Financialization in the Post-COVID-19 World

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The COVID-19 pandemic has revealed the extreme income and wealth inequality that has undermined U.S. economic growth for more than 40 years. The bottom 90% of U.S. households by income have endured stagnant wages, rising debt loads and generalized economic insecurity, all of which became evident as house prices collapsed in 2007-2009. Although many suggest that the inequality is attributable to the impact of globalization and technological advancements on employment and wages, what they miss is the role of speculative finance (financialization) and the complicity of the central bank in driving this process.

The Great Depression is the closest analogue to the extraordinary dislocation currently unfolding in the U.S. economy. Conditions will likely deteriorate further throughout 2020, given the non-linear spread of the virus. The frailty of the U.S. economy is revealed by the staggering levels of income and wealth inequality that pre-dated the arrival of the pandemic. In fact, polarization of income and wealth have been increasing over the past 40 years. A key driver of this phenomenon was the turn toward the “market knows best” framework that began during the 1980s, especially the deregulation and liberalization of financial markets and capital flows.1

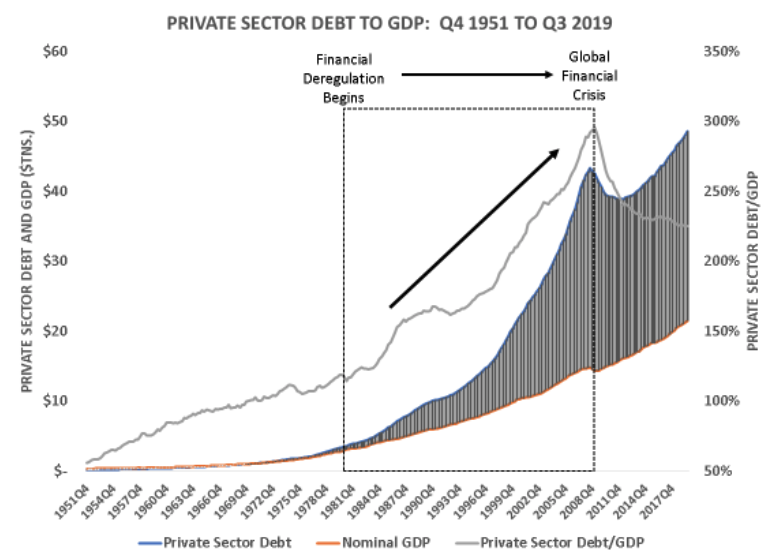

The process of financialization reflects the role of unfettered financial markets in fueling the debt-induced asset price cycles and the turn by non-financial corporations toward maximizing shareholder value that began during the 1980s. Prior to 1980, speculative use of debt was constrained under the financial framework adopted during the New Deal. Interest rates were regulated (Regulation Q) and Glass-Steagall separated commercial from investment banking. Those regulations were eliminated during the 1980s and 1990s, as were other regulations that prohibited corporations from buying back their own stock (November 1982), exempting credit default swaps (CDS) from federal regulations (2000) and permitting corporations to grant stock options (early 1990s). The financialization process began during the 1980s and took hold during the 1990s and 2000s, as financial markets decoupled from the underlying real economy in a series of debt-driven boom-bust cycles (see chart below).

The Fed has been complicit in the financialization process though it is not entirely clear whether this was attributable to regulatory capture, ideology or more than likely, a combination of both. Central bankers, policymakers and financial regulators failed to understand the implications of financial deregulation as constraints were lifted from banks and other financial market participants. This shortcoming was underscored in a speech delivered by Ben Bernanke in February 2004, The Great Moderation, which some have referred to as the “great illusion.” Bernanke believed that markets were efficient and rational. His speech illustrated the obliviousness of the mainstream economics profession to the challenges that would confront the U.S. economy several years later. In fact, mainstream neoclassical models (known as dynamic stochastic general equilibrium models) were designed based on a belief that money is a mere “veil” over the real economy. Those models did not incorporate money, credit, banking, or finance.

Bernanke’s speech followed several crises that the Fed appeared to have navigated successfully. When Russia defaulted in August 1998 and Long-Term Capital Management (LTCM) neared collapse a month later, the Fed introduced the Greenspan or Fed “put.” As asset prices fell in the fall of 1998, the Fed cut short-term interest rates three times, including once on an inter-meeting basis. Thereafter, the Fed left asset prices alone as they appreciated, but intervened whenever they declined, reducing interest rates and injecting liquidity, if needed. The asymmetric policy, or Fed put, effectively provided a floor to asset prices. And the floor would rise along with asset prices. If stock prices rose by 20%, the floor would rise as well. Investors quickly understood that no-fault investing had arrived!

The end-results of the deregulation of financial markets do not correspond with the generalized arguments about the so-called “invisible hand.” According to economic theory, market prices are determined by supply and demand in a “free” market. However, prices in financial markets are driven by investors’ views of valuations, not the valuations themselves. In unfettered markets, euphoric expectations can fuel rapid credit growth that causes asset prices to rise (often accompanied by declining credit quality). Appreciating asset prices in turn drive additional growth in credit, etc. Feedback between credit growth and asset price appreciation drives a boom-bust outcome that can become destabilizing. Valuations run far head of fundamentals for an extended period of time, as they did from the early 1980s until 2007.2 This creates boom-bust cycles, during which markets appreciate for extended periods until fundamentals (gravity, as Wile E. Coyote learned) reassert themselves. This is indicative of how financialization has operated within the financial markets since the early 1980s.

Concerns expressed by a number of economists – Hyman Minsky, Wynne Godley, Steve Keen, Richard Werner, Michael Hudson, and Claudio Borio, to name a few – who operated outside the mainstream neoclassical paradigm were generally ignored, as asset prices soared from the mid-1980s until 2006. The consensus among central bankers in 2001 was premised on the notion that financial crises no longer existed, given that central bankers had figured out how to manage them. The dominance of mainstream neoclassical economists had become so overwhelming that the Queen of England, on a visit to the London School of Economics in November 2008, asked, “Why did no one see it coming?”

For their part, non-financial corporations utilized financial engineering to maximize shareholder value. In November 1982, the SEC approved Rule 10b-18, which permitted U.S. corporations to buy back their own stock. From the 1990s, this became a major driver of corporate activity, especially during the 2010-2019 decade, when U.S. corporations bought back $5.3 trillion of their own stock. The focus on maximizing short-term shareholder value was incentivized by compensation packages for CEOs (stock options, etc.) and by pressure applied by money management firms to deliver positive short-term results. These speculative pressures hollowed out employment opportunities, depressed wages, R&D and productive investments in favor of the pursuit of speculative profits.

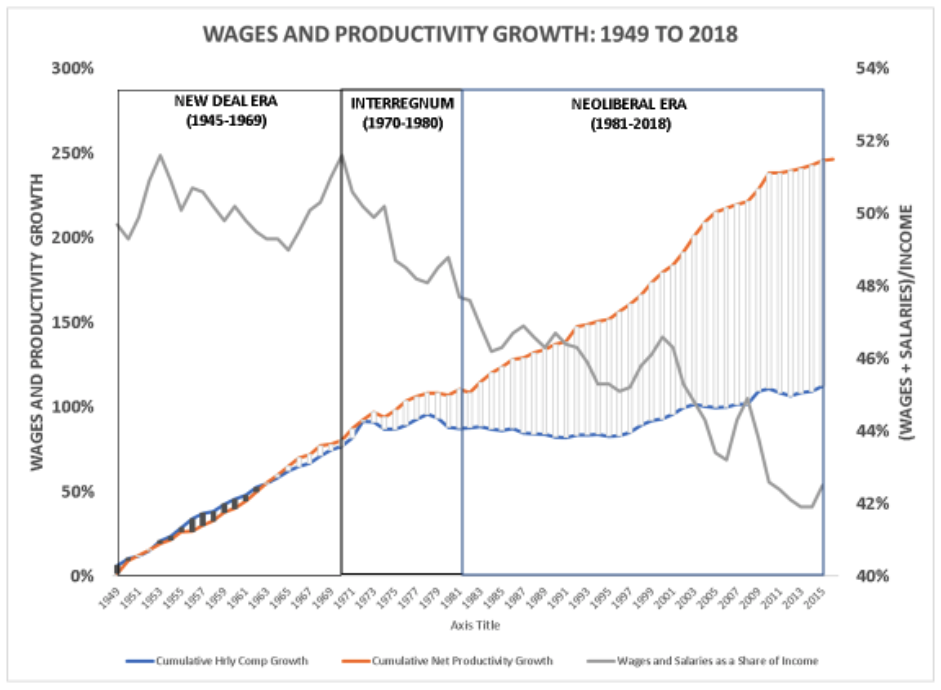

The financialization process elevated the role of markets and short-term profits at the expense of wages and salaries. Regrettably, since the end of the 1970s, real wages have stagnated. Actions pursued by the Reagan administration, including the decision to fire the striking air traffic controllers and to stack the National Labor Relations Board (NLRB) with members who were opposed to organized labor, set the table for administrations to follow. In fact, organized labor was confronting battles on multiple fronts throughout the 1980s, including rising global competition, the overvalued U.S. dollar, double-digit interest rates and the 10% unemployment that occurred in 1982. With organized labor neutralized, there was little unions could do to oppose suppression of real wages. The defeat of organized labor resulted in a Pyrrhic victory, as wages and salaries declined as a share of GDP (grey line in the chart below) since the early 1970s, raising corporate profits at the expense of growth in aggregate demand and real GDP.

Wage suppression stymied growth in aggregate demand, given that wage earners consume most of their income (“they spend what they get”). The turn toward “privatized Keynesianism” (where the private sector, instead of the public sector, uses debt financing to stimulate the economy) that occurred under Clinton supplemented stagnant real wages with household debt. This pattern persisted until the global financial crisis in 2007-2009. From 2001-2007, mortgage-related debt doubled in absolute terms from $7 trillion to $14 trillion, as real estate markets appreciated by about 50% on a nationwide basis. Many households borrowed against the rising equity in their homes (ATM machines), given declining wages.

Rising household indebtedness could be sustained for a while, but not forever. In 2006, financial fragility among highly stressed homeowners began to impact their consumption patterns. As Paul Mason stated in his book, PostCapitalism:

If a declining share of income flows go to workers and yet a growing part of profits is generated out of their mortgages and credit cards, you are eventually going to hit a wall. At some point, the expansion of financial profit through providing loans to stressed consumers will break, and snap back. That is exactly what happened when the subprime bubble collapsed.

As documented by Atif Mian and Amir Sufi in House of Debt, consumption slowed once housing prices peaked. Signs of weakness in aggregate demand were noticeable in early 2007 and into 2008, well before Lehman Brothers declared bankruptcy. The fallout from 2007-2010, though depicted as a financial system crisis, was attributable to rising financial fragility within the household sector (especially middle-class households).

When the GFC occurred and nationwide real estate prices fell by 30%, middle-class households lost 44% of their net worth from 2007 to 2010. The Fed and U.S. government stepped in and bailed out Wall Street, namely the banks and shadow banks that had made poor lending decisions. The Fed also absorbed many of these bad loans on its balance sheet and began to pay interest on reserves held by these banking institutions. However, nothing was done to support homeowners (Main Street) who held underwater mortgages on their residences. The decision not to provide relief to homeowners would slow the 2009-2020 economic recovery, given that these households were focused on paying down debt.

As U.S. interest rates hit the zero bound in 2008, the Fed deployed quantitative easing (QE). In an article published in the Washington Post, Bernanke, the Fed’s resident “expert” on the Great Depression, explained that purchases of financial assets by the Federal Reserve would lower interest rates, despite the zero bound. Lower interest rates would restore confidence and result in increased investment and GDP growth. However, this outcome failed to materialize.

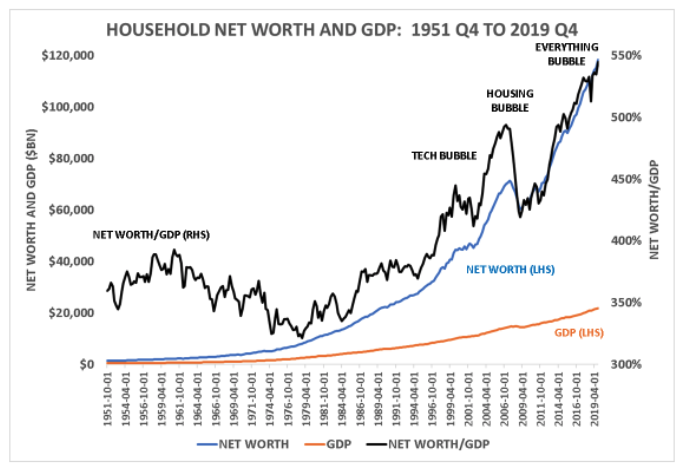

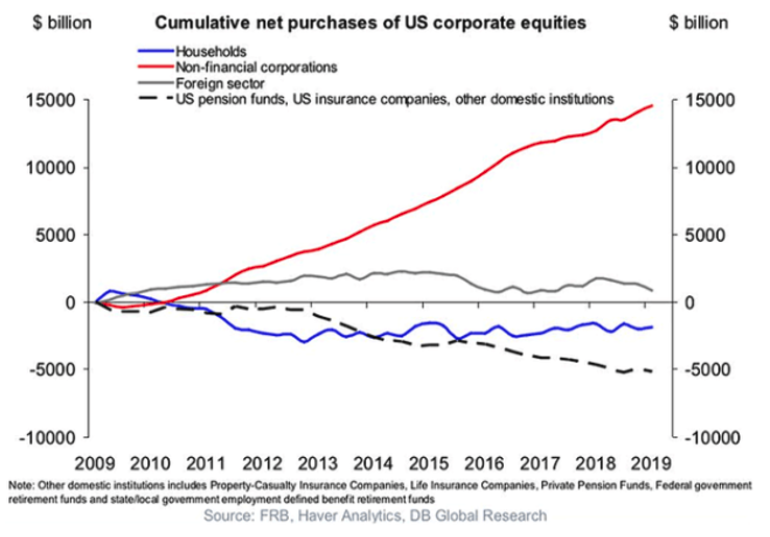

The Fed has consistently misdiagnosed the underlying source of stress in the U.S. economy for the following reason: Lower interest rates have failed to generate increased investment in productive activity. Instead, they have fueled speculative investments, especially among the top 10% of U.S. households, who have been the direct beneficiaries of the “liquidity” or “everything” bubble (see chart below). The Fed supported the deregulation of finance, engineered the Fed put in response to its loss of control, given financialization, bailed out the financial sector and then engineered quantitative easing. Each of those four steps caused the financialization process to accelerate, causing rising income and wealth inequality.

When it conducts QE, the Fed creates reserves “out of thin air” that are used to purchase assets (usually U.S. Treasury and mortgage-backed securities). This additional source of demand causes interest rates to decline. The seller of those assets can then invest the reserves in other financial assets that it purchases from other financial institutions or leave them as is and collect interest (Interest on excess reserves or IOER). The reserves do not leave the coffers of the financial system. They cannot be on-lent to the public. Nor are they finite. There is no central source of reserves; the Fed can create them with a keystroke.

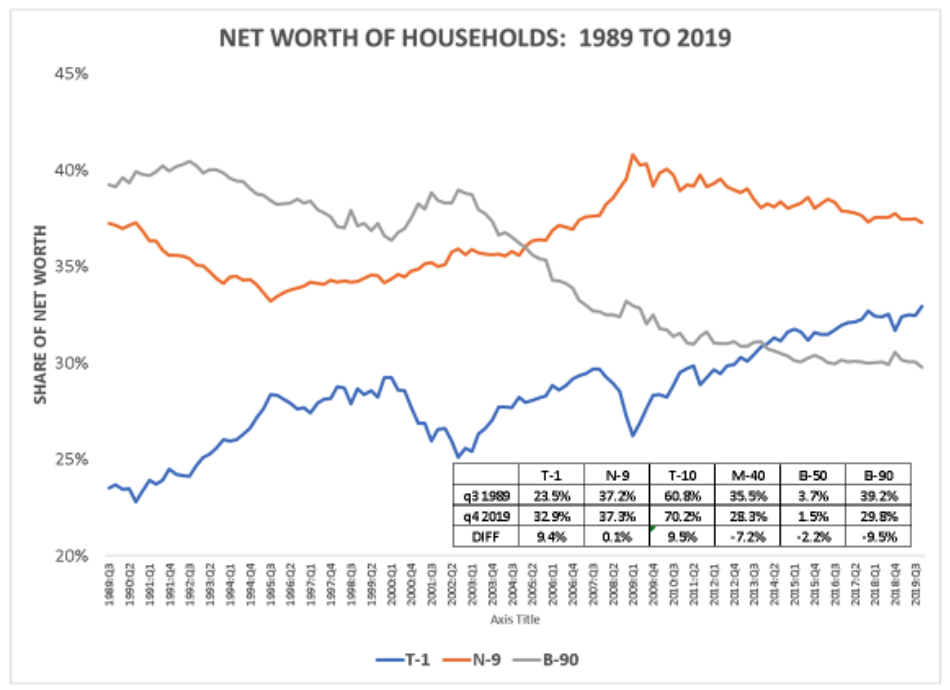

In the aftermath of the GFC, the absence of productive investment reflected the depressed state of the U.S. economy. Financial institutions did not want to lend, and over-indebted customers did not want to borrow. Speculation became the primary driver of the 2009-2020 recovery. Given that the top 10% of U.S. households owned most of the financial assets, they were the primary beneficiaries of the QE policies engineered by the Federal Reserve System (see chart below). The share of wealth held by the top 1% of U.S. households has increased by more than 9% since 1989, while the share of the bottom 90% has declined by about the same amount.

Financial engineering and the Fed fueled the rise of the “liquidity” or “everything” bubble, abetted by corporate stock buybacks and QE. Lower interest rates did nothing to spur productive investments, given that businesses only invest when sufficient demand exists. With the bottom 90% of U.S. households highly indebted and unable to drive aggregate demand, as they had historically, corporations elected to borrow (at record low interest rates) to buy back their own stock, generating financially engineered rises in stock prices that have done nothing to enhance growth in productive enterprise.

Asset prices have been pumped up over the past decade by stock buybacks (which have slowed sharply in 2020, given COVID-19) and by QE, with little support from the underlying economic fundamentals. The private sector debt overhang now casts an immense shadow over aggregate demand.

The Fed is caught in a web of its own design, given its incorrect diagnosis as to how the economy actually operates. If the Fed were to end its QE operations, asset prices would fall sharply (as they did in December 2018). The Fed today has little choice but to continue doing what it has been doing, acting as a “market-maker of last resort,” despite the fact that its actions only serve to further polarize the distribution of income and wealth.

At some point, market participants will lose faith in this engineered outcome.

What happens then?

Investing in a financialized COVID-19 world

Financial fragility, largely from the 2001-2007 era, was quite evident at the end of 2019. The arrival of the COVID-19 pandemic in February 2020 triggered the lockdown that began in March. More than 30 million people remain unemployed and GDP in the second quarter fell by -9.5% (32.9% annualized). For twenty-one of the last 22 weeks, initial unemployment claims have exceeded one million. In response, the Fed and U.S. government came forward with a package of about $6 trillion, with the Fed providing up to $4 to $5 trillion in credit via 11 special purpose vehicles (SPVs) that would be backed by $425 billion in the U.S. Treasury’s exchange stabilization fund (leveraged up to 10 times). Congress approved the CARES Act, which would provide $2.3 trillion in funds that would be distributed to various individuals and corporations. These funds were expected to last until the end of July 2020, by which time many in government thought the pandemic would have ended.

Unfortunately, it has not.

The virus is accelerating in many states and a second wave is possible in the fall. Given the structure of the U.S. economic system, namely the distribution of wealth, income, and debt, according to the Census Bureau 60% of U.S. households do not have sufficient resources to weather three months of expenses without outside support. Most U.S. households’ live paycheck to paycheck, a reflection of four decades of stagnant incomes and the buildup of excessive debts that occurred prior to the GFC. According to Piketty (2018), the share of income earned by the bottom 50% of U.S. households declined from 20% of the total in 1980 to 12% in 2014 as the share earned by the top 1% increased from 12% to 20%. This is a massive redistribution of income and wealth from the bottom 50% to the top 1%.

The magnitude of the dissonance between ebullient financial markets and the devastated real economy is unprecedented in the postwar period. The future path of the U.S. economy is difficult to discern, given the fragile state of balance sheets for the bottom 90% of U.S. households and the uncertainty associated with the pandemic. However, barring the arrival of a miraculous vaccine, numerous restaurants, hotels, department stores, sporting events, concerts, resorts, mass transit systems, airlines, energy companies and other travel organizations, etc., will be forced to close shop before the end of 2020, resulting in significant further falls in employment.

Eventually, liquidity becomes insolvency.

It is impossible to rule out another Great Depression. The ideal response would be for the government to spend, as it did during the Great Depression, without worrying about how the debt will be repaid. The issue parallels the challenge during the Great Depression, though the specifics are different. The problem in both periods is that the distribution of wealth, income and debt were and are out of whack. The bottom 90% have borrowed to support stagnant incomes while the top 10% have enjoyed the bounty due to financialization, at least some of which was directly attributable to the debt amassed by the bottom 90% (fees, spreads, interest payments, etc.). When the global crisis occurred in 2007-2008, the Fed stepped into the breech, utilizing QE to keep the wealth-effect in play, as income and wealth became more and more concentrated at the expense of the bottom 90%. Unfortunately, none of this has supported investment in productive enterprise, which is what generates jobs for the bottom 90%.

The magnitude of the dislocation may be even greater than the Great Depression, given the financialized state of the economy and the massive uncertainty about COVID-19. The corporate sector was hugely leveraged before the pandemic, given the buyback activity and depressed demand.

What is most important is to maintain aggregate demand. The ongoing debate in Congress about whether to continue the payment of $600 to unemployed people is misplaced. This is not the time to worry about excessive government spending. If aggregate demand collapses, we will be living in Japan, except that income and wealth inequality is far greater here and there is much less of a safety net (meaning that the crisis here will be more severe). By focusing on moral hazard (the unemployed staying home because they can collect more from the government than they can be working), Congress is neglecting to see the entire system, given that, as a country with as sovereign currency, “we borrow from ourselves.”3 If the crisis deteriorates and liquidity risk transitions into solvency risk, a decision not to spend ensures a deflationary outcome.

The U.S. government and the Federal Reserve have little choice but to continue pursuing current policies. The Congressional debate will eventually end, one can hope, with authorization of the full $600 per week. What is needed is much bolder leadership. The Fed has made clear its intention to do “whatever is needed” to keep the U.S. economy from sinking, though its credibility will be tested. For now, these policies appear to be resulting in a weaker U.S. dollar, given interest rates that are on hold for some time. A free fall in the U.S. dollar will introduce new headaches.

Investment implications

Gold and other precious metals have rallied strongly so far in 2020 and that pattern appears likely to remain in place. In addition, investment in equity markets outside the U.S. (including Asia and possibly Europe and Japan) that appear to be handling the COVID-19 crisis better than the U.S., may be sensible over time, though caution is advised. And finally, cash makes a lot of sense, given the likelihood that at some point, though no one knows precisely when, U.S. equities might well decline, perhaps by as much as 50%. In any or all of these circumstances, precious metals should continue to perform reasonably well as a hedge against adversity, despite current elevated valuations.

Long-term economic policies: One can hope!

In terms of longer-term economic policies, three come to mind:

- Reverse the financialization process and restructure the financial system. This should have been done during the GFC. Restoration of Glass-Steagall (separation of commercial banking from investment banking) and other constraints imposed during the Great Depression are key. Banks must behave as public utilities, given that they cannot be allowed to utilize public resources to speculate, as they have since the early 1990s. And there are numerous aspects to the creation of central bank digital currencies (CBDCs), that I intend to examine in a subsequent article.

- The Fed must be restructured and democratized. The Fed has become captive to the industry it is responsible for regulating. It will need to work collaboratively with the U.S. Treasury to finance recovery, much as it did during the Great Depression.

- It is time to create a 21st century Reconstruction Finance Corporation (RFC) that can invest on behalf of the public in job creation, infrastructure, green technology, etc. The RFC during the Great Depression and World War II was one of the most successful ventures ever launched by the U.S. Government. There is very little incentive for private corporations to invest in a depressed economy, as was the case during the 1930s.4

It is time to head back to the future and recognize that the preferable economic framework is one that creates an effective bridge between the private sector and government. In order to dig our way out of the current crisis, government (“all of us”) is essential! The collapse of the “market knows best” framework should have resulted in positive steps being taken a decade ago during the global financial crisis. It was truly an opportunity missed! The collaboration that existed during the Great Depression and World War II provide outstanding historical evidence that government and the markets can work together collaboratively to generate positive outcomes for all citizens. Given the COVID-19 pandemic, there is no plausible alternative.

John Balder is working on a book that will examine the links between financialization, Federal Reserve policy and rising income and wealth inequality. He spent more than twenty-five years as a global strategist building innovative investment strategies at firms that included GMO and SSgA. Prior to that he worked with the U.S. Treasury and the Federal Reserve Bank of New York having begun his career with the House Committee on Banking, Finance and Urban Affairs in Washington D.C. These views are strictly his own and do not represent any organization with which he has been or is affiliated.

Bibliography

Balder, John M. (2018). “Financialization and Rising Income Inequality: Connecting the Dots,” Challenge, Taylor Francis Group, August 2, 2018.

Balder, John M. (2020). “A Bold Solution for the Post-COVID Recovery,” Advisor Perspectives, April 27, 2020.

Canova, Timothy (2015). “The New Global Dis/order in Central Banking and Public Finance,” Chapter in the Research Handbook on Political Economy and Law, Edited by Ugo Mattei and John D. Haskell, 2015.

Eccles, Marriner (1933). Hearings before the Committee on Finance, United States Senate, Seventy-Second Congress, Second Session, Pursuant to S. Res 315, entitled “Investigation of Economic Problems, February 13-28, 1933.

Krippner, Greta (2011). Capitalizing on Crisis: The Political Origins of the Rise of Finance, Harvard University Press, 2011.

Kuttner, Robert (2018). Can Democracy Survive Global Capitalism?, W.W. Norton & Company, New York, 2018.

Lazonick, William (2014). “Profits Without Prosperity,” Harvard Business Review, September 2014.

Mian, Atif and Amir Sufi (2014). House of Debt: How They (and You) Caused the Great Recession, and How We Can Prevent It from Happening Again, University of Chicago Press, 2014

Minsky, Hyman (1992). “The Capital Development of the Economy and the Structure of Financial Institutions,” Levy Economics Institute at Bard College, Working Paper N. 72, January 1992.

Quiggin, John (2010). Zombie Economics: How Dead Ideas Still Walk Among Us, Princeton University Press, 2010.

Stockhammer, Engelbert (2010). “Financialization and the Global Economy,” Political Economy Research Institute Working Paper, No. 240, November 2010.

Werner, Richard (2014a). “Can Banks Individually Create Money Out of Nothing? Theories and Empirical Evidence,” International Review of Financial Analysis 36, 2014.

1 This shift in economic ideology and policy is referred to as Neoliberalism, Market Fundamentalism, or the Washington Consensus, all of which were underscored by the financialization of the U.S. economy.

2 Keynes’ expression about “financial markets remaining irrational for far longer than any of us can remain solvent” is particularly apropos of deregulated and liberalized markets.

3 These quotes were from prescient testimony delivered by Marriner Eccles to the Senate Finance Committee in February 1933. Eccles arrived as a banker from the state of Utah and eventually became the chair of the Fed from 1934-1948, as well as a board member from 1948-1951. His testimony anticipated many of the conclusions subsequently drawn by Keynes in 1936.

4 For more on this, see Balder (2020).

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All