I give these brilliant investment strategies a failing grade.

I give these brilliant investment strategies a failing grade.

As advisors and investors, we have evolved over the past several decades from foolish tactics such as picking hot stocks and market timing to more sophisticated strategies. Those sophisticated strategies are supported by peer-reviewed academic rigor. Yet they have failed almost as badly. Here is a look at several failed strategies along with some take-away lessons for the future.

Stocks for the long run – Jeremy Seigel

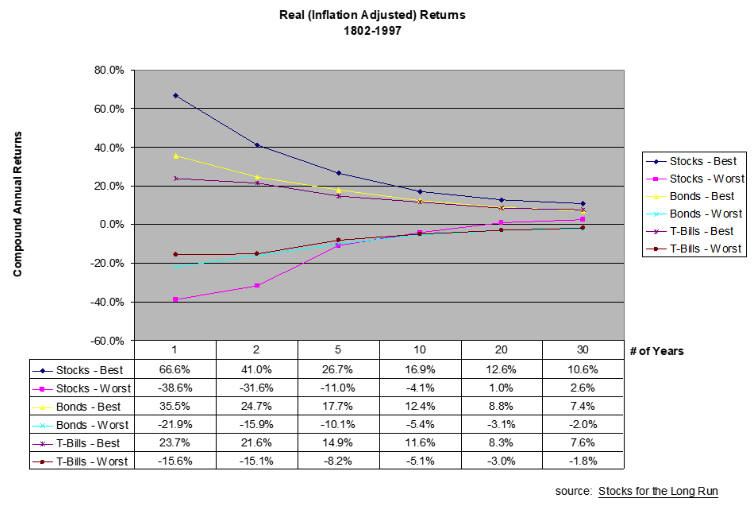

In 1994, Wharton professor Jeremy Seigel first published his ground-breaking book, Stocks for the Long-Run – The Definitive Guide to Financial Market Returns & Long-Term Investment Strategies. It was based on almost 200 years of market history.

The data indicated that the worst 20-year inflation-adjusted return for bonds was an annualized loss of 3.1 percentage points while stocks bested inflation by one percentage point, annually. Thus, stocks were actually less risky than bonds as long as one stayed the course. And the worst we could expect is that stocks would only best bonds by 4.1 percentage points. Who could refute 195 years of history?

But the markets didn’t read the book.

In the 20.5 years since the beginning of this century (12/31/99 ), a portfolio of half U.S. and half international stocks, rebalanced annually, returned 4.58% annually, while a Bloomberg Barclays bond fund returned 5.00% annually, according to Portfolio Visualizer. I’m using international stocks since we live in a global economy.

This isn’t a new phenomenon. A 2009 Ibbotson paper demonstrated that long-term government bonds slightly bested the total return of the S&P 500 for the 40-year period ending March 2009.

So what went wrong? History doesn’t always repeat itself. But just as important, we don’t know how accurate the data is. Wall Street Journal columnist, Jason Zweig, questioned whether Siegel’s data went back 200 years. How accurate was it? Other data showed that between 1803 and 1871, bonds did best stocks.

It turns out that a balanced portfolio of 30% U.S. stocks, 30% international stocks, and 40% bonds (rebalanced annually) did better than stocks or bonds alone, returning 5.29% annually.

Lessons learned: Holding stocks for the long-run may be longer than you can wait. It’s not a choice of stocks or bonds but rather holding both and rebalancing to control risk.

Smart beta – Rob Arnott, Eugene Fama and Ken French, and others

Weighting indexes by market cap was eminently appropriate, yet many felt there was a better way. Rob Arnot’s Research Affiliates came up with what it claims were the first indexes to break the link between price and weight. Methodologies such as weighting indexes by adjusted sales, cash flow, dividends and buybacks, and book value became known as “smart beta.” Proponents argued that relying on John C. Bogle’s market-cap weighting methodology was overweighting the “obviously overvalued” large cap growth stocks.

Though not called “smart beta” at the time, the original factor funds offered by Dimensional were built on the work of Eugene Fama and Ken French. They noted small-cap stocks and value stocks had long-run returns much greater than the market overall. The logic was that small companies weren’t as widely followed and expectations for value companies were much lower than for growth companies, making it easier for those stocks to best those expectations. Vanguard even jumped into factor funds.

But things haven’t gone well recently. Over the five- and 10-year periods ending July 14, annualized returns of the DFA small-cap value (DFSVX) underperformed the old-fashioned, cap-weighted Vanguard Total stock Index funds by 12.15 percentage points and 6.46 percentage points, respectively. As of July 14, 2020, the Invesco FTSE RAFI US 1000 ETF (PRF) had underperformed the cap-weighted iShares Russell 1000 ETF (IWB) by 4.53 percentage points and 2.62 percentage points annually over the past five and 10 years, respectively.

The typical response I get will be something like, “from 1927 through June 2019, the Fama-French (FF) US Small Value Research Index returned 14.5% per annum, outperforming the S&P 500 Index by 4.3% per annum.” I would agree if one had been investing in that style since 1927. How different is that argument than touting the performance of the Fidelity Magellan Fund (FMAGX) since its inception in 1963 while ignoring the fact it has consistently underperformed for the past 15 years?

What went wrong? Nothing. Neither Fama nor French nor Dimensional argued against market efficiency or that these excess expected returns were a free lunch. It was compensation for taking on additional risk. Unfortunately, many advisors ignored this critical fact and promised clients a free lunch.

Lessons learned: Read and understand the underlying academic research. When you are at a conference and hear terms like smart beta and fundamental indexing repeated every few minutes, consider it a warning sign that something hot is about to go into a deep chill.

Alternative investments

The strategy is simple. By investing in asset classes that have little to negative correlations with stocks, you dampen volatility of the overall portfolio. This means that alternative investments will zig when the market zags. Those asset classes include market-neutral funds, commodity futures, foreign-currency futures, inverse-bear market funds, reinsurance funds, and the like.

This is no passing fad, as firms known for their academic rigor jumped in, including AQR and even Vanguard. AQR noted that alternatives can help diversify and complement traditional portfolios by seeking returns that are independent from equity and bond markets and reduce overall sensitivity to traditional markets.

But last year, Morningstar’s John Reckenthaler decided to take a look at the performance over the past decade since they burst onto the scene. He looked at both the best and worst performing alternative investment asset classes. He concluded that not only did they underperform the S&P 500, they generally underperformed even during the worst years for stocks.

Indeed, the AQR Multi-Strategy Alternative fund (ASAIX) has returned a negative 8.95% annualized return over the past five years as of July 14, 2020 and is down significantly from its inception date in 2011. And in the current down market for stocks, its YTD return is a negative 27.60%. When stocks zigged, it also zigged, but with a far greater magnitude.

What went wrong? I first wrote about this in 2012, noting that a good alternative needed something in addition to low correlations; it needed a decent positive expected return. In the aggregate, not a penny has ever been made in the futures markets even before costs since someone has to be on the other side of a trade. And a market-neutral fund should have a zero beta and return the risk-free rate before costs, but with more volatility than cash.

Lessons learned: Low and negatively correlated assets are only one component of a good investment; they must also have attractive, long-run expected returns after the very high costs of these investments.

Private investments

Why invest in public funds when your client is an accredited investor and has access to private deals like hedge funds, private equity, and venture capital. Indeed, this is how the largest university endowment funds invest. David Swenson at the Yale University Endowment Fund uses this strategy.

The argument for these funds is simple. Public markets are efficient, but not private markets. Good venture capitalists can invest in startup winners like Google or Facebook and private equity firms buy companies not part of public markets.

Indeed, these sexy investment options were offered to accredited investors such as the now defunct Endowment Fund, founded by Mark Yusko, the former head of the University of North Carolina’s endowment fund. More on this in a bit.

How have those investments performed? It’s difficult to tell precisely because not all hedge funds report performance. Still, the evidence is compelling that overall performance is dismal.

What went wrong? When money poured into these funds, the inefficiencies of private markets became a small fraction of what they once were when few were playing in these spaces. This means the opportunity for outperformance went way down, though the high fees remained – typically a “2-and-20” model, meaning an annual 2% fee and 20% of profits. At one time, Yusko’s Endowment Fund, a fund of funds, charged over 10% in annual fees. I was able to get two out of my three clients out of this fund before they gated redemptions, locking in those outrageous fees.

David Swenson called hedge funds of funds a “cancer,” layering fees on top of fees. Yale and other large university endowments were paying far less in fees. In fact, three years ago I wrote a story on how a small foundation trounced the big guys. It was mostly by avoiding expensive private investments and merely buying cap-weighted index funds.

Lessons learned: Because your client qualifies for a private investment, it doesn’t mean you should put them in one. These are high-cost products with opaque risks and limited liquidity.

Summing it up

All of these strategies were supported by well-known academic researchers and everyone worked in the past. Why did they fail going forward?

Most charged high to outrageously high fees and some of the research ignored those fees. Past performance isn’t a good predictor of future performance and back testing merely means you are buying at a high valuation, after outperformance. Finally, no professor from any university is going to get published or get juicy consulting gigs by proving once again that simplicity, diversification, low fees, and rebalancing is superior. They must come up with new insights and it is human nature to want to beat the market.

In public markets, the investor return on average must equal the market return before fees. Those high-fee strategies are statistically likely to underperform on a risk-adjusted basis going forward. That is sound, academically proven research on which you can rely.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

More ETF Topics >

I give these brilliant investment strategies a failing grade.

I give these brilliant investment strategies a failing grade.