Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

I hate mutual funds. They can have incredibly high fees, with expense ratios that exceed 4% per year, and that doesn’t include sales commissions. Most mutual funds tend to underperform their benchmarks and many financial advisors who recommend or sell them aren’t fiduciaries.

Because of those simple yet powerful facts, you should never consider mutual funds as part of a client portfolio regardless of their situation, goals, or preferences.

Sound ridiculous? Sure does.

If you substitute “annuities” for “mutual funds,” though, these are the exact statements many financial advisors use for never considering annuities for their clients. While it’s true there are lots of bad annuities, to dismiss them (a product that has been around for thousands of years) outright because some aren’t very good is bad advice at best and a clear breach of fiduciary duty at worst.

While the “annuity puzzle” is well-documented in the academic literature, there is no “mutual fund puzzle.” Annuities and mutual funds are clearly different products, and there are notable differences in how they potentially help clients accomplish their financial goals; however, outliving retirement is one of the greatest fears cited among retirees1 and annuities are one of the few products that can fully eliminate this risk. Therefore, how can a financial advisor ignore annuities carte blanche for all retiree clients and consider that to be good advice (or a good financial plan)?

It’s not.

In this article, I summarize some of the key findings of a paper I have that’s about to be published in the Journal of Retirement titled, “The Value of Allocating to Annuities,” that explores these topics.

The value of allocating to annuities

Few financial products used by advisors are as polarizing as annuities, which I define somewhat narrowly as products that provide guaranteed income for life2. The term “annuity” can be used to describe a host of products, but I focus on those that generate guaranteed income, since that’s why they were originally created.

Despite more than 50 years of research on the potential value of annuitization, the use of annuities among retirees and financial advisors is sparse. Franco Modigliani dubbed this effect the “annuity puzzle” in his 1986 Nobel acceptance speech.

The public perception of annuities isn’t overwhelmingly positive. For example, Allianz released a study in 2011 that found that 54% of Americans aged 44-75 expressed distaste for the word “annuity.”

There are a variety of factors that affect financial advisor views of (and demand for) annuities. For example, annuities can be opaque and difficult to evaluate and compare. This makes it difficult for advisors to ascertain the “quality” (or cost effectiveness) of an annuity, and even more difficult for consumers. The calculations required to properly determine the expected benefit of an annuity, especially a complex one with a guaranteed lifetime withdrawal benefit (GLWB) are beyond the technical abilities of the average financial advisor.

Even among relatively plain vanilla annuities, such as single-premium immediate annuities (also called SPIAs or “immediate-fixed annuities”), there can be a significant variation in the benefits. A SPIA is effectively an irrevocable trade of some portion of the retiree’s savings for the insurance company’s guarantee of income for life. The payout rate, or the total annual guaranteed income divided by the premium, makes these products relatively easy to compare, similar to comparing the yields associated with CDs. While one would assume payout rates would be relatively tightly clustered, or that they would vary according to the credit rating of the insurer, actual quotes are a mess.

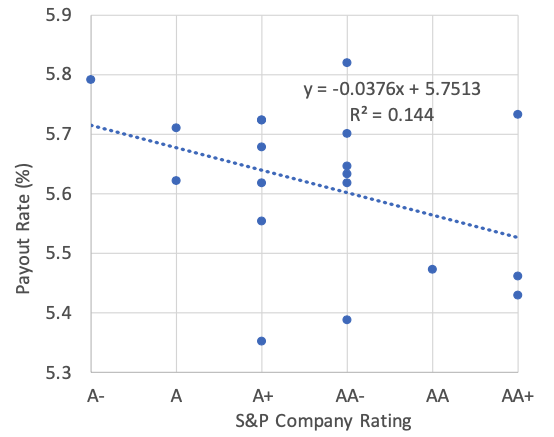

The exhibit below includes the payout rate for 20 different insurance companies providing SPIA quotes on CANNEX on June 22, 2020 for a single 65-year-old male life-only annuity based on a $100,000 premium, along with the S&P credit rating for the respective insurer. I only included insurers with an A- minimum rating.

Immediate Annuity Benefit Amounts and Insurer S&P Company Rating

There is a decent amount of dispersion among quotes. The highest payout ($5,817) is 8.73% higher than the lowest payout ($5,350). While there is a clear inverse relationship between credit quality and payouts, where the payout rate decreases as the financial strength of the insurance company increases, the effect is relatively weak not as strong as would be expected in theory. There are also notable exceptions. For example, there is an AA+-rated company that has a higher payout than an A-rated company.

SPIAs are relatively transparent and it’s relatively straightforward to estimate their expected value. In contrast, GLWBs are significantly more complex, and the expected value is likely to differ by over 25% across products.

Quality is incredibly important when determining the value of an annuity for a client. Many financial advisors dismiss annuities because some products have relatively high costs (i.e., are of relatively low quality). Even if most annuities were low quality, given the fact financial advisors have access to a large range of annuities, as well as a growing number of commissions-free products, dismissing them entirely because some are not very good is no longer a viable excuse. Just as there are high-cost annuities, there are high-cost investments (e.g., those with high expense ratio, as I noted in the opening). But it is the job of each financial advisor to determine which products are best-suited for their clients.

Dismissing mutual funds as an investment option because some are expensive and underperform is not a valid argument, but that’s the exact argument many financial advisors use for dismissing annuities.

The value of financial advisors offering services beyond investment planning (i.e., the value of financial planning) has been a topic of growing interest. I did some research with my Morningstar colleague Paul Kaplan on a topic we called “gamma.” We found helping a client create a more efficient retirement strategy can result in an alpha equivalent of over 200 bps in a variety of papers. Vanguard’s Advisor’s Alpha had similar findings. The more holistic the advice the better, and holistic advice demands seriously considering annuities.

Analysis

For the original research that this article is based on, I did a complex analysis that used Monte Carlo simulations and utility theory. I’m not going to get into the weeds in this article. To know more about the nitty gritty of the analysis, you’re going to have to read my paper when it is published.

My analysis focused on the idea of the “cost” (or quality) of investment and annuity strategies. For example, I can increase (or decrease) the associated fees (or costs) for an annuity and the investment portfolio to make them relatively more or less attractive. I did this for 243 different scenarios, where the assumed household attributes varied by the percentage of total income derived from Social Security, the initial withdrawal rate, the length of retirement, the portfolio allocation, and shortfall risk aversion. I attempted to represent the situations and preferences of different retiree households. I don’t want to assume a “generic” retiree household, but rather simulated how they differ in terms of situations and preferences.

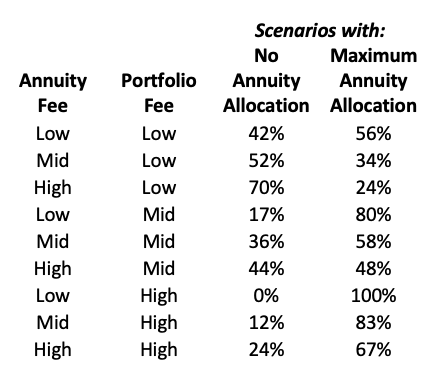

As I changed the fees for the annuity and for the portfolio, the optimal allocation to annuities changed significantly. In the table below, I show the percentage of scenarios that have no annuity (0%) and those that have the maximum annuity allocation (50%) for the nine different fee combinations between the annuity and the portfolio.

For example, if the annuity fee is low and the portfolio fee is high, the annuity allocations were significantly higher than if the reverse were true. The most realistic assumption is if the fees for both the annuity and the portfolio were moderate (i.e., “mid” in the table above). Under this assumption, there were 36% of scenarios that had no annuity allocation and 58% of had the maximum possible allocation (50%). In other words, nobody should categorically include or exclude annuities in a retirement plan; annuities are going to be a lot more attractive when they are fairly considered in the financial-planning process.

If you compare an expensive (high-cost) annuity to a low-cost portfolio, you’re not going to find much benefit to annuitization. That’s not a fair comparison, though. If you can build an efficient portfolio, you can select an efficient annuity.

Summary

Not allocating annuities simply because they are “expensive” is an overly simplistic perspective, since investment strategies can be just as, if not more, expensive. To help clients achieve better retirement outcomes, advisors must be familiar with the types of annuities available, their relative strengths and weaknesses, and how they can and should be incorporated to an efficient retirement plan. Ignoring annuities in a retirement plan is akin to attempting to build a portfolio without a major structural asset class such as fixed income. While it can be done, it puts clients at a clear disadvantage and does not help them accomplish their goals.

David M. Blanchett, Ph.D., CFA, CFP®, is head of retirement research for Morningstar's Investment Management group.

1 Right up there with healthcare costs

2 Guarantees are based on the claims-paying ability of the issuing insurance company.

Read more articles by David Blanchett