Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“…seven years of college down the drain.” – John “Bluto” Blutarsky, Animal House

The inspiration and credit for this article belongs to Emil Kalinowski and his recent publication, The Silent Depression: Trundling Is the New Booming.

Most profound about Kalinowski’s piece is that it was published just eight days prior to the February 19 S&P 500 market peak. Kalinowski’s article highlights the same problem that I have been discussing for many months now. That issue is how the media, Wall Street’s “finest,” and Ph.D. economists misrepresent economic conditions.

Their economic euphemisms and overly optimistic expectations remind me of a Dylan Grice quote “Linguistic precision yields cognitive precision.” Or, put a little differently, linguistic imprecision yields stupidity.

Strong economic footing

We entered this turbulent period on a strong economic footing, and that should help support the recovery. In the meantime, we are using our tools to help build a bridge from the solid economic foundation on which we entered this crisis to a position of regained economic strength on the other side. –Jerome Powell 4/9/2020

To paraphrase Bluto, “eleven years of economic recovery down the drain.” Sporting a 0.0 GPA, like Bluto, the U.S. economy was never in a real recovery or on “strong economic footing.” The expansion was like Enron’s profits, Madoff’s performance record, and Lance Armstrong’s seven Tour de France titles; they never existed.

Instead, what we experienced was little more than a made-for-television comedy/drama or super-hero movie. Most people were led to believe it was real as they watched. It may have even been somewhat entertaining, but it was a fabrication.

What is becoming increasingly clear, however, is that the price for our fabrications to future generations is dear. As Kalinowski properly documented, we were already in a “silent depression,” what comes next is entirely another matter.

Decisions and incentives

As I have written, an economy hinges upon individuals making decisions about needs and wants in their own best interest. Those decisions are influenced by a variety of factors, including:

- The discipline and prudence to save;

- The desire to invest wisely to compound wealth; and

- The need to borrow to consume more today.

The objective of monetary policy for the past 30 years has been to influence those individual decisions. The obvious goal has been to promote more spending and discourage savings.

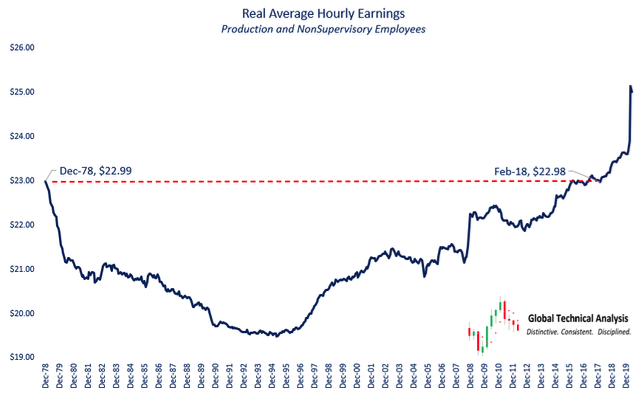

Throughout the process, debt levels grew much faster than aggregate income at an individual, corporate, and national level. As shown in the chart below, real wages for most Americans have been stagnant. Inflation-adjusted hourly earnings were the same in 2018 as they were 40 years earlier. The recent bump in earnings will likely reverse as they are due COVID-related stimulus checks.

That creates a problem for the Fed, the solution for which lies in manipulating the cost of money – interest rates.

Wisdom

Warren Buffett’s partner, Charlie Munger, is well-known for his emphasis on understanding incentives. Munger says that if you want to predict how people will behave you only have to look at their incentives.

So, the Federal Reserve, wanting to encourage more spending despite stagnant wages and rising debt loads, changed the incentives. They began to impose price controls on the cost of money.

The most expedient and effective way of making poor people feel wealthy is to give them cheap loans.

Unsurprisingly, people, corporations, and the government responded.

Gradually, then suddenly

The current extreme circumstances we observe surrounding monetary and fiscal policy evolved over time.

Leniencies taken following the October 1987 stock market crash and the early 1990s savings and loan crisis/recession in the name of the greater good led to economic imbalances and misallocation of capital. The question, therefore, is whose greater good?

Instead of reversing crisis policies and allowing the economy to function on its own accord, the Fed “managed” ensuing expansions.

Successive and progressively larger bubbles formed and burst as a result of prior misallocations. In each ensuing instance, the demands for the government and the Fed to “do something” grew incrementally louder. These voices overwhelmed any concerns about whether or not “doing something” was constructive and in the collective interest.

Instead of well-thought-out reason and logic, the counter-factual ruled the day. For instance, “if we had not passed TARP (in 2008), the financial system would have collapsed.” How would anyone know? Such myopic thinking results in the Fed and Congress mutually granting the authority to do more of that something. Regard for legality or long-term efficacy are not considerations.

Hedonics

According to Congress, the Fed has a dual mandate that governs its activities. First, it must seek a monetary policy construct that will maximize employment and, second maintain, price stability.

(A third mandate, fast solidifying in the language of the Fed and the halls of Congress, is the objective to maintain financial stability. That concept is not in the Federal Reserve Act. It is so obtuse as to override the first two and allows a small group of unelected, unaccountable officials wide berth on virtually any action.)

Achieving the proper balance between mandates is important. However, it is inconvenient and constraining in terms of the Fed’s unspoken goal of urging people to borrow and spend more. To avoid that problem, Alan Greenspan began lobbying the government bureaus responsible for measuring inflation to modify their inflation metrics.

From this, adjustments using hedonics were born. Hedonics argue that if the quality of a good is improved and its price unchanged, then the adjustment will lower its reported price.

Televisions and computers are easy examples. Given technological advancements, hedonic adjustments allow the Bureau of Labor Statistics (BLS) to deliver Consumer Price Inflation (CPI) readings that are lower than they otherwise would be. That allows the Fed more latitude in holding interest rates lower than they otherwise would be or should be. In so doing, the Fed can provide the incentives to influence the public to incur debt to consume.

Like any Ponzi scheme, money and leverage must increase at greater rates, or it will collapse and reveal the fraud. Therefore, to protect the true identity of the scheme, each successive setback (dot-com bubble, housing bubble, COVID-19) must be met with even greater extraordinary measures.

Do something

As described in The Fed Enters Monetary Lightspeed, Fed actions and talking points go beyond the imagination. The language we hear from Treasury and Fed officials is frightening, especially considering they do not know what the future holds or what is best practice any more so than you or us. It does not matter; reality is superseded by the “DO SOMETHING!” demand.

In his interview on 60 Minutes on May 13, 2020, Fed Chairman Jerome Powell served as both amateur epidemiologist and Fed chief fortune-teller re-stating the obvious:

The good news is that the 20 million people who've been laid off overwhelming report themselves as having been laid off temporarily. They're considered temporarily unemployed. And that's because they expect to go back to their old job.

Powell continued,

So if those businesses can reopen and if we can do it in a way that doesn't create further problems with the virus, then people can go back to work. So I would say the peak unemployment might be in the next couple of months. And then you might see it coming down over the second half of the year.

I hope he is correct, but given that even epidemiologists and medical doctors do not know what to expect, I am hesitant to grant Powell and his Ph.D. economist colleagues the benefit of the doubt.

I would prefer that our leaders manage risk prudently and expectations even more carefully.

A telling article by Patricia Cohen in the New York Times, citing Stanford economist Nicholas Bloom, claims that 42% of recent layoffs will result in permanent job loss. His study, rigor, and analysis stand in stark contrast to Powell’s off-the-cuff prime-time TV happy talk.

Powell once demonstrated some promise in the area of considering the cold hard facts and the risks that go along with them. On page 192 of the transcript from the October 23-24, 2012 Federal Open Market Committee (FOMC) meeting, Powell expressed deep reservations about several major issues. He worried about the size of the Fed’s balance sheet and the difficulties that may accompany reducing purchases and balance sheet size. He also clearly had anxiety about unforeseen market risks and the Fed’s role in advancing moral hazard stating:

I think we are actually at a point of encouraging risk-taking, and that should give us pause. Investors really do understand now that we will be there to prevent serious losses. It is not that it is easy for them to make money but that they have every incentive to take more risk, and they are doing so. Meanwhile, we look like we are blowing a fixed-income duration bubble right across the credit spectrum that will result in big losses when rates come up down the road. You can almost say that that is our strategy.

These are remarkable comments. They stand in stark contrast to what we are seeing from Chairman Powell in 2020.

Summary

The appearance of a record long economic expansion was fueled by expanding levels of debt and corporate share buybacks. The façade of recovery, a soaring stock market, convinced most people that it was real. The quality of economic growth was the weakest in decades, despite rounds of QE, near-zero interest rates, and ridiculous amounts of Federal spending. That, in the words of Powell, constitutes a “strong economic footing.”

Maybe for his well-endowed investment accounts.

The current fiscal and monetary policy actions mimic the mistakes made during and after past bubbles. The language used to describe their actions, as illustrated by Emil Kalinowski, is highly suspect.

Despite, and potentially because of, policy decisions to flood the economy with money, most of which will never reach those who need it, stresses will re-emerge. Our hope lies not in pumping up another imaginary “Bluto” economy. Our hope is that leadership will adhere to principles that foster the needed discipline for a healthy organic economy. One in which all boats rise.

We, as individuals and as a nation, will either live with discipline or regret. Pray we choose wisely.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.