Since 2009, the U.S. stock market has outperformed the rest of the world by a factor of nearly three. But that “American exceptionalism” may transition to a movement to break up monopolies, according to Jeffrey Gundlach.

Gundlach spoke to investors via a webcast, which he titled “Superman,” and the focus was on his flagship DoubleLine Total Return Bond Fund (DBLTX). Slides from that webcast are available here. Gundlach is the founder and chairman of Los Angeles-based DoubleLine Capital.

The exceptional U.S. performance was due to a group of companies he called the “super six”: Facebook, Amazon, Apple, Alphabet, Netflix and Microsoft. Without those six stocks, the S&P “494” would be up about 12%, only slightly better than the MSCI all-world, ex-U.S. index.

Price gains and earnings growth across those six stocks have far outpaced the earnings of the other 494 stocks. There has been no EPS growth in those 494 or in the rest of the world, according to Gundlach.

Gundlach’s view is that the dominance of those six stocks could lead regulators to break them up, especially if the economic recovery falters.

That is not Gundlach’s only fear. If Biden “or some like-minded politician” wins the November election, Gundlach said, he could increase corporate taxes. “That will take away some of the underpinnings of the market.”

Gundlach began his presentation with a video featuring a soundtrack of a 1967 hit song, Up, Up and Away, by the pop group Fifth Dimension. The video featured images from the Albuquerque hot balloon festival, a clicking debt clock and Fed Chairman Jerome Powell in a Superman costume, replete with dollar bills floating through the air.

The balloon launch was a metaphor for the soaring national debt, Gundlach said, driven by the various liquidity facilities that were enacted by the Fed, starting in March. “We are not up, up and away in terms of economic growth, though,” he said.

Public debt grew by $3.5 trillion this year, despite a contraction of $2.5 trillion in GDP. Last year, debt grew by slightly more than GDP in real and nominal dollars. “This debt is really big,” Gundlach said.

The problem, according to Gundlach, is that debt will impede economic growth. Japan got to 120% of debt-to-GDP in 1998, and the U.S. is at that level now. But Japan has not had any real GDP growth since then. Japan was the “pace car” for debt growth, he said, and it has been joined by the European Central Bank (ECB).

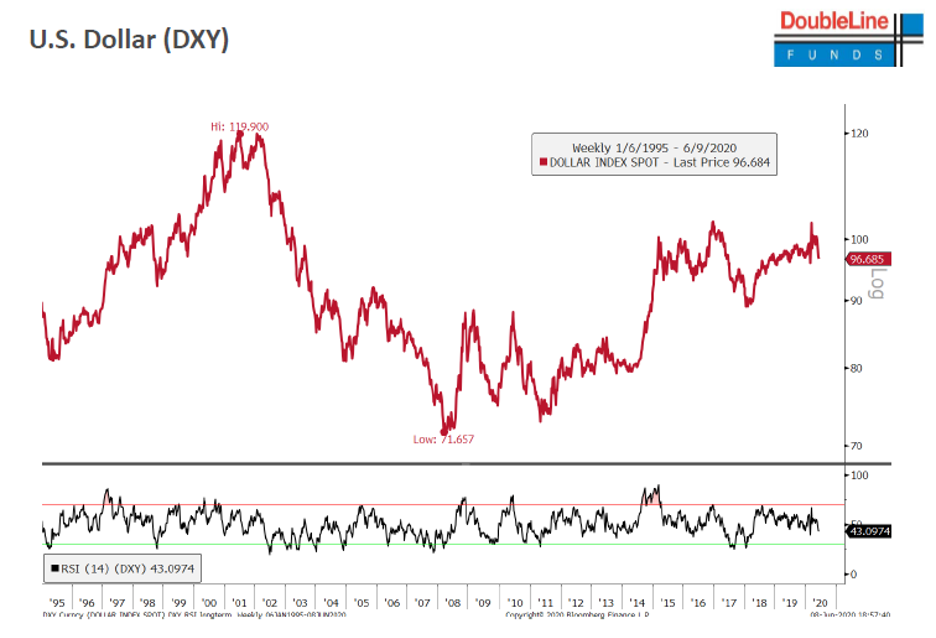

Has the U.S. run up its debt faster than other countries? Yes, he said. Using a chart that showed budget deficits as a percentage of GDP for 2019 and through April 2020, he showed that the U.S. is at the extreme on both dimensions among large global economies. “We have put on the accelerant and the dollar has started to weaken,” Gundlach said.

The dollar was a safe haven during the stock market sell off, but it fell when the market recovered.

Powell is being praised for the performance of the stock and bond markets, Gundlach said, but the Fed will move to “yield-curve control” if the 30-year yield becomes “unhinged.” Yield-curve control means the Fed would use open-market activity to control yields on long-term Treasury bonds. The Fed has been controlling the five- and 10-year part of the market, he said, but seems to be less concerned about the 30-year, so far.

Bond market action during the crisis

A lot of fear struck parts of the bond market outside the scope of the Fed’s liquidity programs because of the specter of forbearance and nonpayment. But those fears have been unfounded, he said. There has been no increase in defaults on government-backed securities, like GNMAs. In the non-agency market, forbearance has increased only slightly.

There has been some forbearance in student loans, he said, but not at a very high level. By comparison, there were much higher levels of forbearance and default during the 2008 financial crisis.

The corporate bond market has been the worst performer among the fixed-income markets since the Fed announced its measures to support that market on April 9. It turned out to be unwise to buy what the Fed was buying, Gundlach said, contrary to conventional wisdom. Emerging markets, which were not supported by the Fed, have outperformed corporate bonds by about 700 basis points since that date.

That atypical corporate-bond performance was, in part, due to front-running of ETFs, such as iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD). Gundlach said corporate bond ETFs were trading at huge discounts to their underlying securities prior to April 9, and eventually shifted to a premium. “The indices couldn’t keep up with the price action,” he said, because of the lack of liquidity in the corporate bond market.

Corporate bond prices became highly volatility at the peak of the crisis, due to the small size of dealer inventories, which have been contracting since 2007. The lack of corporate bond inventory was why Powell and the Fed had to act in that market, he said.

The post-pandemic prognosis

“Superman [Jay Powell] showed up and managed to finance an awful lot of the economy,” Gundlach said.

But what does this mean for the future, after those programs, like the PPP, roll off?

Many workers who lost their jobs during the pandemic will not be able to return to work, he said. There will be other problems, like higher-end unemployment. Mostly low-paying jobs were lost during the lockdown and those people were protected by government stipends. But, according to Gundlach, businesses will learn that many white-collar, service-sector jobs were not as essential as some people assumed. Those businesses will rethink whether they need as many supervisory, middle-management personnel.

“I could easily see layoffs hitting those earning $100,000 per year, who are not eligible for government help,” he said. Those people have insufficient savings and will be unable to find jobs. They will be forced to take lower-paying jobs, especially if they have a family to feed. That is “wage deflationary,” he said.

Employees permanently working from home will also lead to lower wages, as people will no longer need to live in expensive locations, like the Bay Area.

Inflation will be non-existent this year, he said. That is supported by data from the N.Y. Fed’s underlying inflation gauge, which has predicted inflation accurately 16 months ahead. The Conference Board inflation survey spiked to 6.2%, which reflects an inflationary psychology that could drive inflation, Gundlach said. Money supply, as measured by M2, shows some signs of inflation.

The outlook for monetary policy

Gundlach recounted that, in May 2009, the market thought the Fed funds rate would rise; it never did. Now, he said, the market believes Powell is Superman and will keep the Fed funds rate at zero for the next two years.

“The Fed clearly wants to remove volatility from the market, and it has succeeded in doing that,” he said. That has been true for stocks, corporate bonds, high-yield bonds and other asset sub-classes.

In response to the Fed’s actions, there was an “ocean” of inflows into corporate bonds, he said, based on LQD. The inflows were twice the outflows. LQD’s price is being propped up by the Fed, but has performed relatively poorly over the last two months.

“There is a tremendous belief that LQD is the place to be,” he said, “but that is not justified by the underlying fundamentals, he said.”

There will be continued waves of downgrades in the corporate bond market, he said. But there has been growth in corporate bond issuance over the first five months of this year, especially since late March. Investors have bought those bonds out of a need to “put cash to work,” he added.

The illusion of growth

The growth since the financial crisis was an “illusion,” Gundlach said. All the jobs created since then were lost in the last several months. Some will be gained back, but many are lost permanently.

Moreover, we have the same interest rate policy and quantitative easing as we did after the financial crisis. “One way to look at things is that we never really left the great financial crisis,” Gundlach said.

He asked, rhetorically, whether the Fed’s extraordinary policies have worked. If they had worked, we would not be using them again, he said. But we have had to reapply those policies, and they have had a weaker effect.

“We could be heading for bigger QE, negative rates, or yield-curve control.”

He warned that “rampant speculation” has been driving the market. According to the brokerage site Robinhood, since mid-May, retail investors have been investing in mega-cap growth stocks. Other on-line brokers have benefited from the growth in retail accounts. There has also been an ominous growth in open interest in call options, which could signal the end of the rally.

The dollar looks “terrible,” he said, although it has moved sideways over the last five years. But the trade and budget deficit are about to explode, and that foreshadows a weaker dollar.

Gold has done well, but has hit a resistance level. But Gundlach thinks it will go to new highs over the next several months. Long term, he said he is “unequivocally bullish on gold.”

Where is the kryptonite?

Superman’s weakness was kryptonite, and Gundlach identified several things that could prevent even Powell from fostering economic growth and a strong market.

The kryptonite is the budget deficit, Gundlach said, and it is just beginning to explode. In a six-week period, the unemployment rate skyrocketed. Staying at these levels of unemployment and deficits is “really problematic,” he said, especially during this period of social unrest. The employment-to-population ratio dropped from 62% to 52%. If it goes below 50%, we have an upside down society, with more people unemployed than not, and “things could get seriously out of hand.”

The vast majority of unemployment insurance claims don’t get approved, he said, but that changed in this crisis. Nearly 80% of applications are getting approved. That led Gundlach to conclude that, “perhaps two-third of all stimulus funds may be wasted. It is fast and loose with the money printing.”

The biggest kryptonite of all is negative interest rates. They have proven to be a disaster in Japan (starting in 1995) and Europe (starting in 2009), where negative rates destroyed the performance of bank stocks. The U.S., by virtue of having non-negative rates, is the destination for capital flows.

If we go negative, it would be catastrophic for the global financial system. “It would be fatal,” he said.

The last piece of kryptonite is in the corporate bond market. As he has noted in the past, the BBB-rated portion of the bond market, one step above junk, is extraordinarily large. The high-yield bond market would be overwhelmed if a sizeable portion of those bonds were downgraded.

Many more bonds are being downgraded than upgraded, he said, and the ratings agencies are worried. They are being more proactive in downgrading marginal credits.

Based on the credit-default swaps market, the implied default rate was 9.67% for the next year for the high-yield market and 60.5% over the next 10 years. After the April 9 Fed actions, those rates decreased to 6.18% and 46.2%. But, unless fundamentals improve significantly, Gundlach said those default rates will catch up with the weak underlying fundamentals of the issuers.

Read more articles by Robert Huebscher