Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Visualizing your retirement savings not as dollars, but as tokens – like those used as the medium of exchange in amusement parks – will help retirees overcome the pernicious bias of myopic loss aversion.

Chuck E. Cheese is a kid’s dreamland, allowing for the instant gratification from tickets, lights and sounds. What do kids have to give up for the simple pleasure of playing pop-a-shot and video games? Tokensi. Tokens are the medium of exchange (currency) for this instant gratification, without which kids are relegated to watching others experience the joys of play.

We work so that we can earn money, our medium of exchange, allowing us to purchase goods and services for our own gratification. Whatever extra money we have we save for future consumption. That savings can come in many forms – a savings account, CDs, stocks, bonds, etc. Those assets become our tokens that we exchange for a form of consumption in the future.

Say we live in a world where we are paid in dollars but need to purchase goods and services in tokens. Each week, I make $100, I need $60 worth of tokens to pay for my general living expenses, another $30 worth of tokens for leisure, leaving me with $10 in tokens to save for later. I ask the man behind the counter what options I have to invest these tokens to be consumed in retirement. He gives me the following three buckets to choose from, along with the possible range of returnsii:

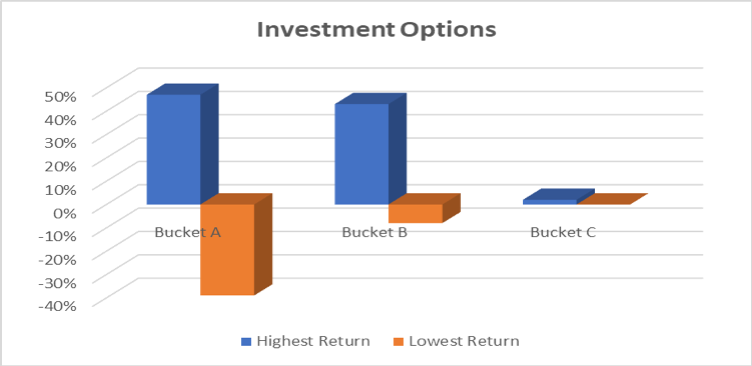

Figure 1

Bucket A: 47% to (-39%) Bucket B: 43% to (-8%) Bucket C: 2% to 0%

He assures me that between now and retirement he will offer me liquidity by buying or selling me additional tokens whenever I want. However, each time the price of the token changes based on how his business is doing. When business is good, he may offer to buy/sell me tokens for more than $1; if business is bad, he may offer to buy/sell them for less than a $1.

Which bucket would you choose?

Most people would choose B, assuming you are not very risk averse. Bucket A doesn’t make much sense, since I could lose more than a third of my investment for the possibility of only earning an additional 4% more than bucket B. Bucket C gives me the safest return, but since I’ve been playing video games a long time, I know that in 20 years it’s going to take two tokens to play the same game that costs me one today (inflationiii); 2% is probably not going to work.

Before making my final decision of which bucket to invest in, the man behind the counter offers me another set of optionsiv, with the caveat that these buckets are only available if I keep the tokens till retirement.

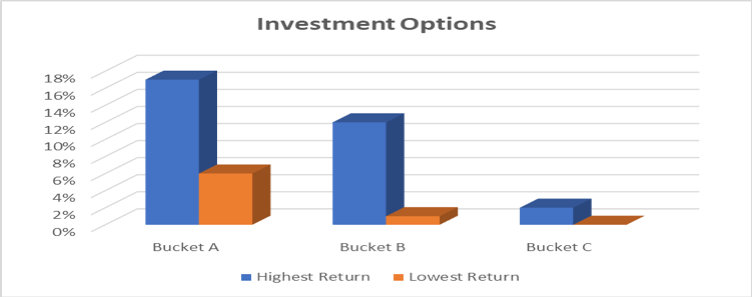

Figure 2

Bucket A: 17% to 6% Bucket B: 12% to 1% Bucket C: 2% to 0%

Clearly in this set of options, bucket A is the most rational choice. It has the highest possible range of returns and will almost certainly double the worth of my tokens. In this illustration, the only difference between figures 1 and 2 is the time frame. Figure 1 represents the range of returns over a 1-year time frame, while figure 2 represents the annualized range of returns over a 20-year period. These return ranges were calculated on a rolling basis from 1950-2019, with bucket A representing equities, and bucket B representing bonds. Bucket C is a hypothetical cash account, somewhat representative of a savings account. Historicallyv, had you held on to stocks for 20 years at any point during this period, your best return would have been 17% and the worst being 6%, annually. The best 20-year return for bonds would have been 12% annually, with the worst being 1%.

If one has a long-term horizon for investing, which is often the case for retirement savings, it would be rational to have a greater proportion of your portfolio invested in bucket A (equities). Unfortunately, we often make investment decisions based on figure 1, leading us to less than optimal portfolio allocations. In their paper “Myopic Loss Aversion and the Equity Premium Puzzlevi,” Benartzi and Thaler provide a possible explanation. Their main thesis was to explain the equity risk premium (the excess return of stocks over bonds) through two behavioral biases, loss aversion and mental accounting. Loss aversion is the tendency to feel greater pain in losses than pleasure in gains. Tversky and Kahneman estimated that losses weighed roughly twice as much in disutility versus utility experienced through gainsvii. Put another way, a $5 loss is twice as painful as the pleasure of gaining $5. Mental accounting, in this instance, refers to our preferences in evaluating financial outcomes over finite periods. We typically look at our portfolios at least once a year if not more frequently. The combination of these two biases leads to myopic loss aversion.

In the short run, equities have a wide dispersion of returns, as referenced in figure 1. Evaluating our performance more frequently inevitably leads to seeing losses. Those losses then weigh heavily on our decision making, and often derail our initial decision to invest in equities. Myopic loss aversion thus leads us to make short-term decisions on long-term goals.

Economic theory teaches us that money is fungible, i.e, regardless of which purpose the dollar is used for it is all the same. For example, a dollar in our retirement funds should be viewed in the same way as a dollar in our savings account. Unfortunately, this is what often leads to myopic loss aversion. We are viewing our net worth as one bucket.

To mitigate myopic loss aversion, I propose looking at the problem in a different light. Mental accounting, in this sense, can work to our benefit by segregating accounts into separate buckets to be used during distinct time frames.

The goal of any investment strategy is to optimize the utility gained from the “tokens” you have. The optimal strategy is to match those tokens to the utility (consumption) they are used for, instead of viewing all tokens as the same. In this sense you would have a bucket for your near-term tokens, a bucket for the mid-term, and a bucket for the long-term. You would then invest those tokens in the optimal instrument that has the highest risk-adjusted probability of return over those periods. Since our near-term bucket would match consumption in the present, it would be most optimal to have that in stable, less volatile investments. For the long-term bucket you would want to have investments that provide for the highest probability of return, regardless of volatility because the consumption of those tokens is not a concern in the present. You would continually roll this strategy as time passes by adding or subtracting from each bucket to match your estimated consumption in each period.

Don’t blindly put all your long-term monies in equities. A prudent asset allocation strategy, based on your goals, risk tolerance and time frame is always necessary. Investing presents risks, and the more frequently you review your statements the greater probability of seeing a loss. Asking yourself what that investment is for, and, more specifically, when you will need those tokens may help mitigate myopic loss aversion. If, historically, the tokens have always been worth more 20 years from now, why concern yourself with the value today, tomorrow, or three months from now. What matters most is the value of those tokens in the future, because that is when they will be used for consumption.

“Proper investment strategy is as much of a psychological as an intellectual challenge.” – Jeremy Siegel Stocks For the Long Run

Krisna Patel, CFA is a financial planner located in Zionsville, IN. He can be reached at [email protected], twitter, linkedin, or through his blog www.theunbiasedadvisor.net.

i I realize that if you go to Chuckie Cheese now, tokens have turned into a card with token credits

ii JP Morgan Guide to Markets: https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-the-markets. Bucket C is a hypothetical cash bucket with a range of 0-2%

iii This comes out to roughly 3.53% annualized inflation

iv JP Morgan Guide to Markets: https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-the-markets. Bucket C is a hypothetical cash bucket with a range of 0-2%

v Figure 2

vi https://www.nber.org/papers/w4369

vii http://www.sscnet.ucla.edu/polisci/faculty/chwe/austen/tversky1991.pdf

Read more articles by Krisna Patel

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.