This century is barely 20% complete, yet investors have suffered through three extreme bear markets. Let’s look at which asset classes provided the much-sought diversification to offset losses in U.S. equities.

It hasn’t been a stellar century for stocks. In fact, through the first quarter of this year, bonds performed as well as U.S. stocks and trounced international stocks. These are measured as the total return (including dividend reinvestments) of the Vanguard Total U.S. Stock Index, International Stock Index, and Bond index.

That’s because of the three bear markets we’ve so far experienced. We began with the dot-com tech bubble, when the “new age” economy meant that cash flow no longer mattered. It was simple to do an IPO with virtually no revenue or hope for profit and still get multi-billion-dollar valuations. Next was the real-estate/financial bubble, when we banked on the fact that real estate could never go down in value. That presumption allowed agencies to assign AAA ratings to complex mortgage derivatives backed by borrowers who had no prayer of meeting their obligations. Fast forward 11 years and the longest bull market in history, and the COVID crash that changed all of our lives.

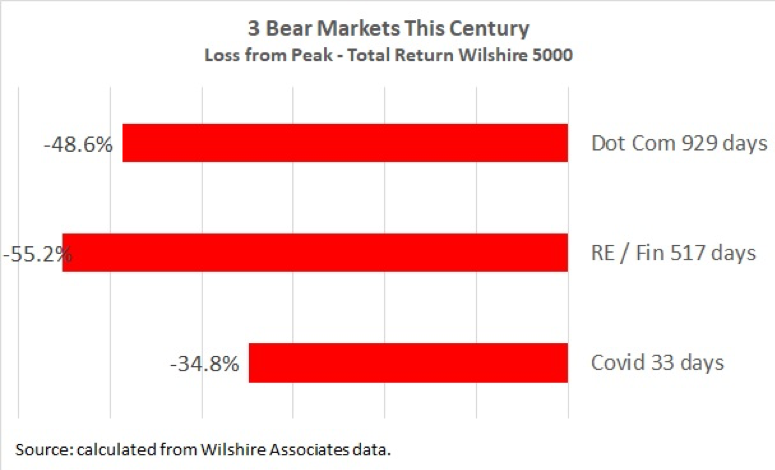

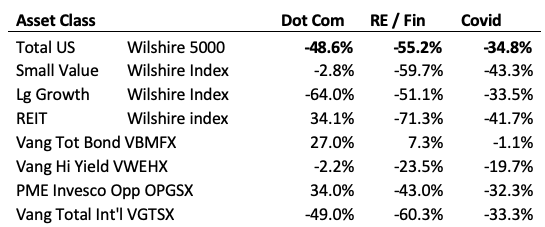

Among the three bears, the COVID crash has, so far, been the mildest, down 34.8% followed by a very rapid recovery after the bottom on March 23. But we don’t know if this crash is over. Markets remain as volatile as the data on the coronavirus itself. Though the dot-com bubble wiped out 48.6% of the U.S. stock market value, first place (so far) goes to the real estate bubble that wiped out 55.2% of the U.S. stock market value.

Your clients are certainly feeling more pain from the COVID crisis than the distant and faded memories of the first two bears, due to what’s known as “recency bias.” Yet there are two additional reasons the pain is far greater.

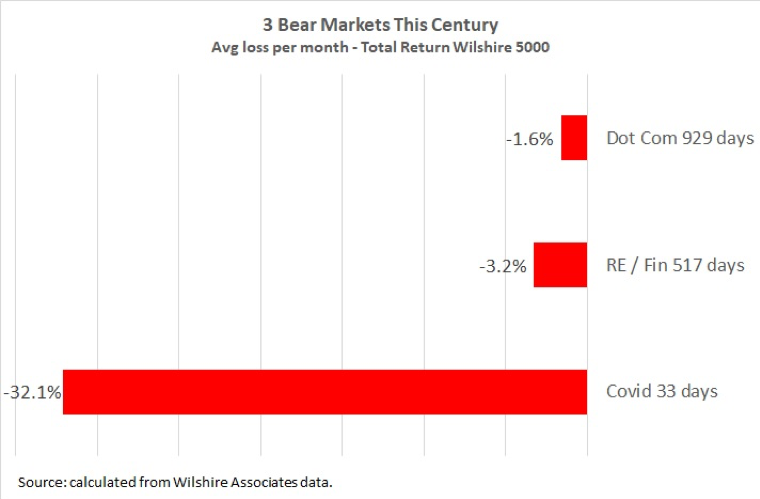

We are all older, meaning we have less human capital (years of earned income) and more investment capital. We have a double whammy of losing more money with fewer years to get it back. The second is the sheer speed of the losses. The dot com bubble took 929 days, losing only an average of 1.6% a month. The real estate bubble had a twice faster pace, losing 3.2% on an average month. But the COVID crash was shocking, with a pace of 32.1% in just over a month. That’s 20-times faster than the dot-com and 10-times faster than the real estate/financial bubble.

What worked during plunges?

Throughout the bears I’ve monitored what investment strategies worked to mitigate the losses. Some worked during every bear, some did with spotty success followed later by failures, and some didn’t work at all. In my review, I’ve excluded any asset class with a low or negative expected return. These include managed futures and options, where not a penny has ever been made before costs in the aggregate. I excluded other alternatives such as inverse-stock funds, market-neutral funds, and long-short funds. I also excluded expensive hedge funds due to unreliable data, though the evidence is strong that they have underperformed.

I compared broad U.S. stocks, measured as the total return of the Wilshire 5000 index, to:

- Small-cap-value tilt – Wilshire index

- Large-cap-growth tilt – Wilshire index

- REITs – Wilshire index

- High-quality Bond – Vanguard Total Bond (VBMFX)

- High-yield bond – Vanguard High Yield Corporate (VWEHX)

- Precious metals equity - Invesco Oppenheimer Gold & Spec Mnrl A (OPGSX)

- International stocks – Vanguard Total International (VTGSX)

I used funds that existed through all three bears. For Vanguard, these were the more expensive investor-share-class funds, though today ETFs and Admiral mutual fund classes are the better choice. For precious metals equities (PME), the choice was particularly hard. My vehicle of choice was the Vanguard Precious Metals Fund (VGPMX) until 2018 when Vanguard abandoned the PME mandate. Thereafter my choice was the Van Eck Gold Miners ETF (GDX). But for the purpose of this analysis, I used a large PME fund that existed throughout the period which was the Invesco Oppenheimer Gold and Special Minerals fund (OPGSX).

Dot-com bubble

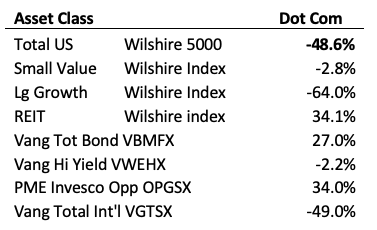

From the market peak on March 24, 2000 to the bottom on October 9, 2002, U.S. stocks lost 48.6% of their value. Owning international stocks provided no cushion. Those who believed in the new age economy saw large-cap-growth give up 64% of its value and found out cash flow really did matter. Four asset classes worked – REITs and PMEs gained 34%, total bond gained 27%, and small-cap-value lost only 2.8%. Junk bonds lost only 2.2%, but far short of high-quality bonds.

Real estate/financial bubble

For exactly five years (from the bottom on October 9, 2002 to the top on October 9 2007), U.S. stocks doubled and international stocks tripled. Sophisticated AAA-rated derivatives were sold, based on what would turn out to be insolvent mortgage borrowers. I saw many portfolios heavy in REITs and small-cap-value, counting on what worked in the dot-com bubble to work again.

This was not to be.

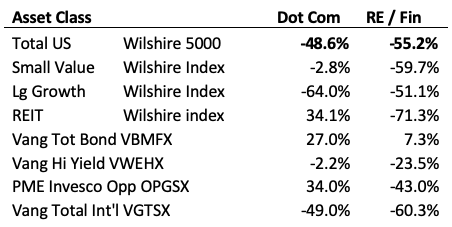

From October 9, 2007 to March 9, 2009, U.S. stocks lost 55.2% of their value and only high-quality bonds provided protection. Small-cap-value and REITs did far worse than the U.S. stocks and PMEs didn’t do much better. High-yield bonds performed more like stocks than high-quality bonds. In short, those who felt bulletproof by designing portfolios that worked during the dot-com bubble did worse than the market during this plunge. Those who chased the strong international stock performance from 2002 to 2007 paid the price as well.

COVID crash

After a record-long 11-year bull market, the real estate crash was followed by the shock and awe of the COVID crash. In less than five weeks, U.S. stocks lost 34.8%. While this was much faster than the real estate bubble, it wasn’t without precedence. During the real estate bubble, U.S. stocks gave up 29.1% in just two weeks. As in the past two bubbles, high-quality bonds generally held but high-yield again showed high positive correlation to stocks. REITs and small-cap-value, which worked so well during the dot-com crash, again did worse than U.S. stocks. While precious metals equities only slightly bested U.S. stocks during the crash, they came back with a vengeance, gaining 51% from the bottom on March 23 to May 1 of this year. Belatedly, PMEs acted as a great shock absorber.

Lessons learned from the three bears

What each bear has in common is that they are different. What worked in one bear usually did not work in the next. Counting on history to repeat itself based on one bear is like drawing a regression line from one data point. The causes of each bear were different and most asset classes performed differently.

The one asset class that failed or at least didn’t help much in all three bears was international stocks, as it has badly lagged overall so far this century. Yet, I believe in international investing for diversification. This is especially true with the mushrooming domestic debt.

High-quality bonds are where investors turned to in all three bears. High-yield failed miserably and didn’t provide much of a cushion or the source of funds to use for rebalancing. And that simple, but not so easy, rebalancing has worked brilliantly across all three bears. High-quality bonds allowed one to buy more stocks after the plunge and stocks have recovered in all three bears. It is better to buy stocks when they are on sale and sell after a surge. Capitalism will survive COVID and the next several bears as well.

Bears are a critical part of investing. Preparing our clients for them is key. This means developing the right portfolio asset allocation and preparing clients for the emotional toll it will take when bears happen. The one certainty about the next bear is that it will be different than the past.

We need to help our clients pick an asset allocation they can live with. This means understanding their willingness and especially their need to take risk, which requires far more than taking a risk-profile questionnaire. Take risks with stocks, but keep fixed income at the highest quality. Stick to that allocation no matter how bleak the news. I tell clients that, when it comes to investing, pain is a sign they are doing something right.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth