Medicare Will Cost Me HOW Much?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Your clients are typically blindsided before I work with them. They believe that Medicare is “free” or is largely subsidized because, “I paid into the system my whole life and now I have to pay what?”

To put this in perspective, consider the calls you are likely getting with COVID-19 in the background.

“I was going to retire in 2021, but I’m outa here.”

Or, “I lost my job in April, and I’m not so sure I’ll be getting another one since I’m 66. I should look into Medicare and what it costs.”

A fair amount of those people that land on my doorstep are shocked at how much Medicare will cost them.

As in shocked.

Dr. R was turning 65 last fall and happened to work for a small physician group with fewer than 20 employees. Being in a small group of under 20, Medicare primary-payer rules require that he get his Parts A and B of Medicare in place. Pretty simply, “you have to.”

Since he had to, this is typically the time that I suggest that he and his wife leave the small-employer group insurance as well. That plan often then becomes only a pricey supplement to their Medicare government coverage.

We did just that. I walked them through what to do and when to do it. I gave them each a great Medigap contract and a Part D drug plan.

I got a voicemail a few months later from a cranky Dr. R. I called him back and he said, “Do you know that I’m paying almost $20,000 for this Medicare stuff?” (Ok, so he didn’t use the word “stuff”.)

“Yep, I sure do”. I know every detail of his package as his Medicare consultant.

Let me back up and discuss how I work so you can see how clients learn about these costs.

With a new consultation, I start with, “Ok, do you need Medicare coverage?” Some do; some don’t at age 65.

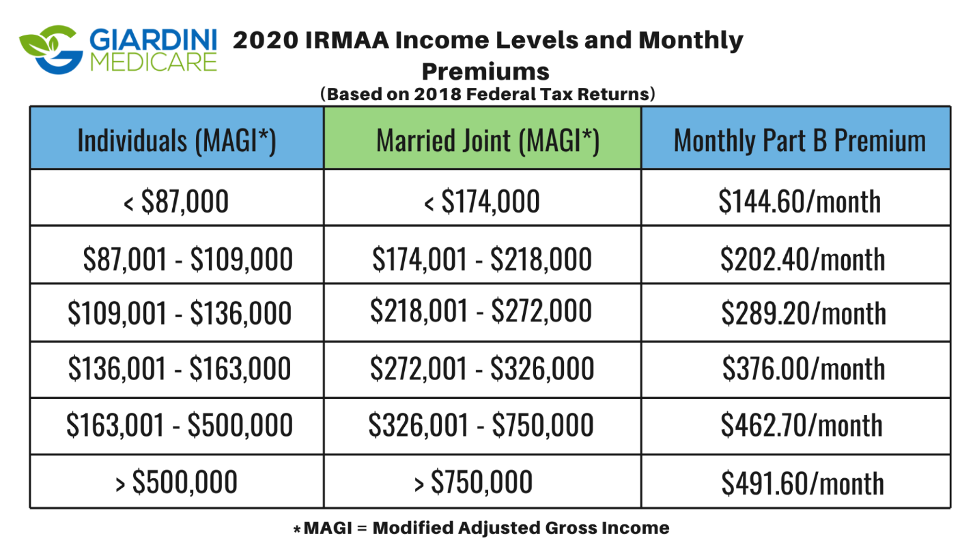

Ok, you do, Dr. R? Has anyone discussed with you how much it will cost? No? Let’s walk through that. I have to say, I can’t recall a person answering that question with, “Oh, yes, I realize that my premium to the government for Part B will be $289.20 per month. What else do I need to know?”

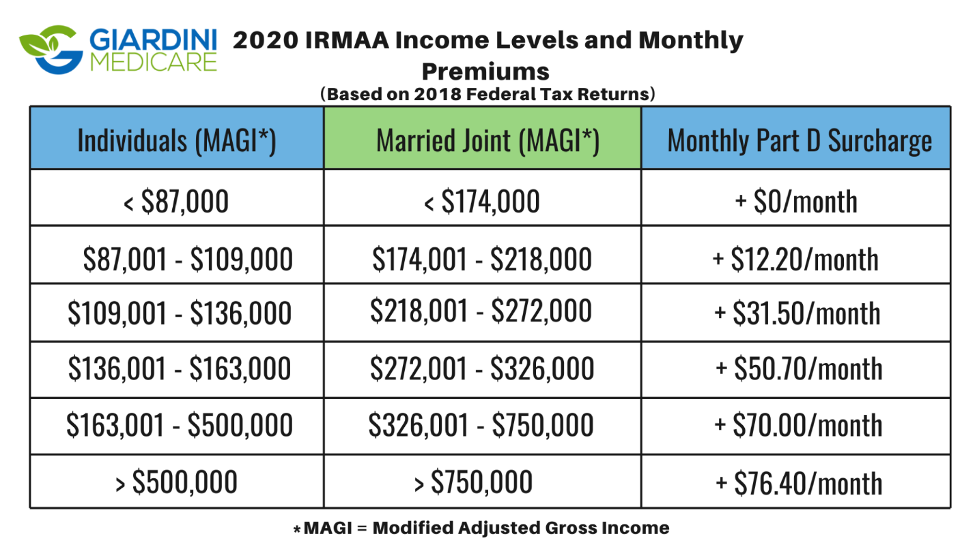

Then they say, “I have no idea.” I screenshare our IRMAA charts (below) and send them our follow-up YouTube Channel episode about Medicare’s cost.

Part B premiums

Part D premiums

What is IRMAA?

IRMAA is the income-related monthly adjustment amount charged to higher-income folks on Medicare. It’s a surcharge. It’s a tax. Whatever you’d like to call it, your clients who earn more will pay more.

After I tackle the conversation about how much Medicare will cost, then it’s time to talk about the products that they should secure to round out their coverage.

Now that Dr. R is actually paying the bills, it’s becoming more real to him each month. He and his wife are high-income earners. Each of them will pay $491.60 per month for Medicare Part B. That includes their IRMAA surcharge. They pay a surcharge on the Part D, which amounts to $76.40 per month.

Add to that their Medigap contract of $125.00 per person, per month and a Part D plan for $20.00 and you can see that each of them is paying a bit over $700 per month or $17,000 annually.

Thus, Dr. R’s sticker shock. He thought Medicare was supposed to be, “a great deal when you get older.”

Remember what your clients are seeing in the world of Medicare advertising. They will never see a TV commercial proudly stating, “You can have this Medicare Advantage plan for no cost each month, it includes free dental and vision coverage, a gym membership and all you’ll have to be sure to pay is your $491 each month in addition to your $76 surcharge to the government”.

And, when your client is speaking with friends about Medicare, rarely does that friend boast about paying their high-income surcharge. But they are happy to share their stories about how they get everything for free with their plans.

I speak with people who will swear they pay nothing for Medicare Part B. They’ll get their Medicare card out; they clearly have Parts A and B and insist that they pay zero and have done so for years. I help them understand that minor detail in their direct-deposit records for their Social Security each month: a Medicare Part B deduction. Whoops, you’ve been paying it all along.

Here are some suggestions to aid you in health care conversations.

Start the discussion early

Throw the word Medicare into conversations with your clients when they are in their early 60s. They don’t need to understand much more than, “Hey, when you get there, we need to understand that the amount you will pay is going to be tied to your income so let’s talk about income streams.” What a great topic for a financial planner.

IRMAA is based on modified adjusted gross income (MAGI). Simply say, “The government will look back two years at tax returns and compare that number to this chart so let’s plan best we can to navigate these charts.”

An aside, you will be the most brilliant advisor on the planet to your client as those conversations don’t take place very often. How do I know that? My question, “Has anyone discussed how much Medicare will cost you?” No, ok, let’s proceed….

Just by bringing up this concept about income levels and Medicare costs, they’ll at least have some idea when they get there.

A friend of mine has a very, very high-net worth, but pays the base Medicare Part B rate of $144.60. It’s all about income streams. And it can be navigated.

Redetermination at retirement

Let’s say that you have a high-net worth client earning $500,000 and he suddenly retires. His income stops, right? So, she says, “It’s not fair that I have to pay that higher amount since my paycheck stopped.”

That’s correct! I help people daily walk through the “redetermination process” with Medicare. If that person earning $500,000 has no paycheck going forward and is going to live off of $145,000 MAGI annually, then by all means, I can help him file the proper paperwork that essentially says to Social Security, “My paycheck is gone, my tax return will be less,” and 99.99% of the time, the person’s cost will be reduced to the lowest rate possible for Medicare Part B which is $144.60 this year.

If they don’t send in the form? Yes, their income will cycle through, meaning that every two years, as Social Security looks back at the tax return from the prior two years, the person’s income will be less and thus their Medicare premiums will be less as well. But, why wait? I get lots of “you’re a rock star” emails after the person wins their reduction. I can work with you to be the hero, too.

Part B penalty obsession

An odd part of Medicare planning is the world’s quasi-obsession with “the penalty.” Everyone seems to know about the Medicare Part B late-enrollment penalty. But not that many people are affected by it.

People would save more money over their lifetime if they understood the implications of IRMAA and Medicare instead of worrying about the Part B penalty that often has nothing to do with them and won’t affect them a bit.

Conclusion

Lay the groundwork early with a simple conversation about Medicare and its eventual costs. Remember that many of your clients had parents with very rich and generous retiree health benefits. Their parents didn’t complain of cost and lack of coverage. That’s not the case for many new retirees. Those costs are “on them” and they will be complaining like Dr. R.

Pay attention to IRMAA early, but not to the point of panic. Mention it and that we should be cognizant of its existence.

I’ve got Medicare tools and tips to help you and your clients.

I work with you, the advisor, because I don’t like getting Dr. R’s grumpy phone call any more than you do.

Let’s pre-empt it with a bit of planning.

Joanne Giardini-Russell is a Medicare nerd with Giardini Medicare (formerly Boomer Health Group), which was created to help those approaching Medicare eligibility or those currently enrolled in Medicare better understand what they are purchasing and how their choices may affect their long-term outcomes regarding care, finances, etc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All