Robo advisors offer commoditized investment solutions for those in the accumulation phase. But planning a retiree’s withdrawal strategy is much more complex. I examine new research that offers a way to algorithmically determine how to draw down one’s savings.

Researchers have proposed a variety of ways for retirees to turn savings into income, including such methods as the 4% rule or relying on required minimum distributions (RMDs). Methods proposed have typically been generic and not customized for individual retirees. Researchers at CANNEX, a Canadian retirement-research firm, have proposed an approach where the pattern of withdrawals reflects individual client attitudes toward risk. I’ll describe their proposed approach, provide my assessment, and offer more general comments on withdrawal strategies.

With the shift to defined-contribution plans, the retirement template has evolved to accumulating savings during the working years and then placing the responsibility on individual retirees to determine how to spend their savings during retirement. Spending funds too quickly risks old-age poverty, and being too frugal risks missing out on opportunities for enjoyment.

Of course, retirees could just buy annuities (along with delaying Social Security) and not be concerned about outliving their savings. This strategy makes sense to cover essential expenses. But there’s still the issue of timing discretionary spending, and there are retirees (or their advisors) who are not comfortable with annuities, and therefore face bigger challenges spending down savings.

Individual retirees will differ in how comfortable they are spending more early in retirement and risking coming up short in old age. That leads to the question of whether withdrawal strategies can be developed that adjust for such individual differences.

The CANNEX adaptive-withdrawal strategy

CANNEX recently published a white paper that proposed its adaptive-withdrawal strategy (AWS), which incorporates what it referred to as “longevity risk aversion.” Basically, those who are more concerned about outliving their assets should spend less in the early retirement years in order to hold onto more savings for later in life if needed. The specific method it proposed for coming up with spending recommendations involves economic utility analysis. The white paper doesn’t get into the utility function math, but the inspiration for this method goes back to research by Professors Huang and Milevsky at York University in Toronto, who published the 2011 paper, “Spending Retirement on Planet Vulcan.” This paper provided an in-depth description of the approach, including the utility math. It certainly will be worth reading the CANNEX white paper to gain a fuller understanding of what the CANNEX authors are proposing, and the “Planet Vulcan” paper for those who wish to delve into the supporting math.

A difficulty in customizing its approach for financial planning clients is that it requires specific numerical assumptions to do the utility math – a risk aversion coefficient and a personal discount rate. However, it is feasible to put in reasonable numbers for assumptions and propose general conclusions about retirement withdrawals, as the authors do in the white paper. This type of research can be useful.

The CANNEX authors make the argument that their approach to retirement planning produces higher withdrawals earlier in retirement, when retirees are able to get the most out of spending. Their approach incorporates variable longevity, so any utility from spending money later in retirement is discounted by an increasing probability of not living that long. They also confirm that higher levels of guaranteed lifetime income (Social Security, pensions or annuities) enable higher withdrawals early in retirement.

CANNEX’s criticism of other approaches

The authors compared their approach to results using the 4% rule and RMDs. They make the argument that the 4% rule is inefficient because it fails to adjust to investment performance, which can lead to extremes of either depleting savings during retirement or leaving a large bequest after sacrificing retirement spending unnecessarily. This is old news, as many researchers, including myself, have made the case for dynamic withdrawal strategies that adjust for investment performance.

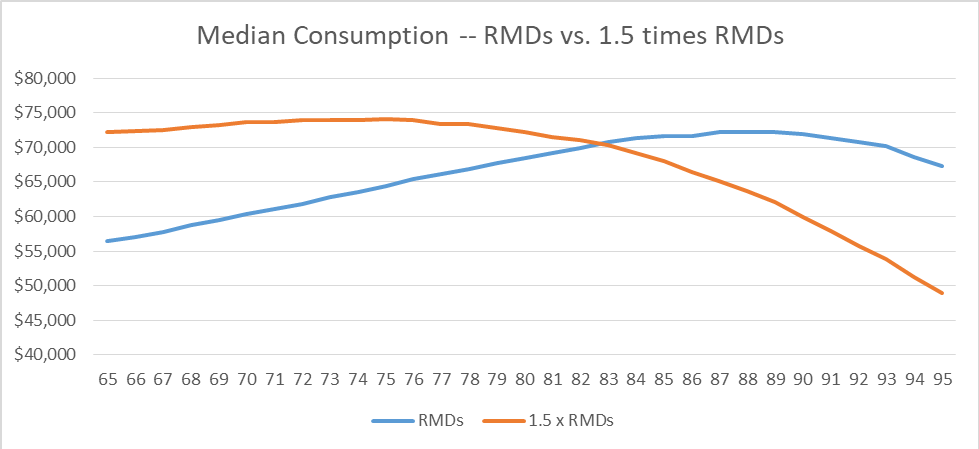

The authors noted that the RMD approach has the advantage of being dynamic, in that the RMD percentages apply to current portfolio values. But they criticize the method as being too stingy in the early retirement years. They show withdrawals under this method do not peak until about age 90, whereas with their adaptive approach, withdrawals start at a higher level, grow more gradually than with RMDs, and peak around age 80.

In their criticism of the RMD approach, the authors cited a 2017 Stanford study as advocating RMD withdrawals. I happen to be a co-author of that study, which was co-sponsored by the Stanford Center for Longevity (SCL) and the Society of Actuaries (SOA). Our research found that the RMD approach performed well compared to a number of other strategies. Unfortunately, the CANNEX folks were apparently unaware of subsequent SCL/SOA research published in July 2019, where we focused on the Spend Safely in Retirement (SSIR) strategy, including variations of the RMD method. These included multiplying RMDs by a factor such as 1.25 or 1.5, or setting aside separate funds, for example, a “travel bucket,” for additional spending during the early retirement years.

The chart below compares RMD withdrawals with a withdrawal pattern where RMDs are multiplied by 1.5. It turns out that the 1.5-times RMDs approach closely matches the CANNEX withdrawals depicted in the charts in their white paper, although, admittedly, the 1.5-times withdrawals has not been fine-tuned for individual risk preferences.1 These consumption paths are based on the same example used in the CANNEX white paper – $1 million of savings at age 65 and annual Social Security benefits of $25,200.

One particular aspect of the CANNEX AWS is that it treats longevity as variable, while many of the software systems used by advisors treat retirement as lasting for a fixed period, such as 30 years. It turns out that adding the realism of variable longevity to modeling retirement has a big impact on results, similar to the way Monte Carlo modeling of investment performance provides much more useful information and often different conclusions than assuming fixed returns. The only other planning software I am aware of that uses variable longevity is AACalc (available as free software). A quick AACalc test with the example used in the CANNEX research produced a similar retirement spending recommendation.

Challenges

Designing software that will make individualized retirement withdrawal recommendations presents a series of challenges for the CANNEX authors and others. I’ll briefly list some of these challenges here:

Utility analysis – There is only a tenuous link between utility analysis and future realized wellbeing. The particular type of utility function used by the CANNEX authors assumes what is known as constant relative risk aversion (CRRA) and time-separate utility – that the utility of a given year’s consumption is independent of consumption in prior years. This is the type of utility function most commonly used in research. However, some economists have argued for assuming habit-forming utility with year-to-year dependence, where people are assumed to be particularly averse to decreases in consumption. This is closely related to the Kahneman/Tversky concept of loss aversion.

To add more to the muddle, psychologists like Daniel Gilbert argue that people are not good at anticipating how their wellbeing will be affected by future happenings. In particular, people respond more positively to adversity than they predict they will. My own view is that CRRA time-separable utility is of some use in research – level consumption is preferable to consumption that bounces around from year to year, but it’s a mistake to try to be too precise with utility analysis.

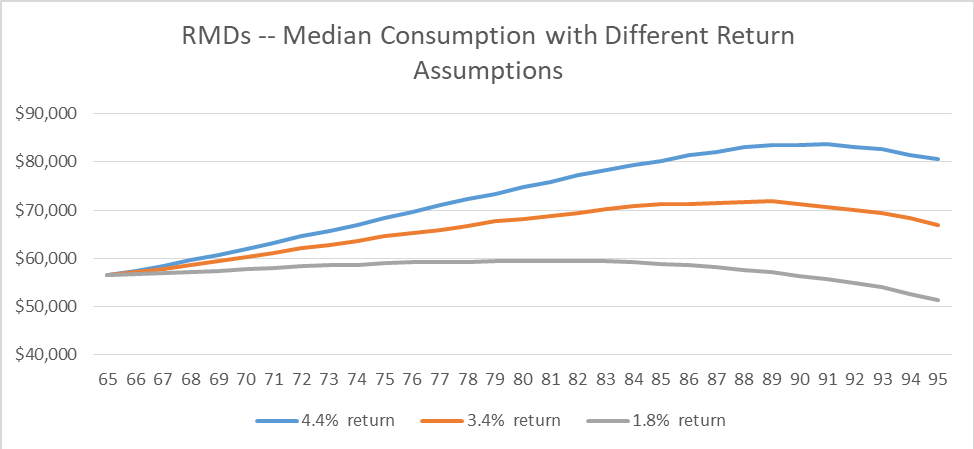

Future investment returns – Under any dynamic withdrawal strategy, the shape of future withdrawals will depend on what happens with actual investment returns. For example, in the chart below I show three different withdrawal paths for RMD withdrawals for a 60/40 stock/bond portfolio – a 4.4% average portfolio real return based on the CANNEX assumptions, a 3.4% average return based on my own assumptions and a more pessimistic 1.8% assumption. The latter recognizes that real interest rates are close to zero and assumes future real stock returns averaging 3%, reflecting the Shiller CAPE at an elevated level of about 30 until recently. With the 1.8% assumption, the withdrawals produced stay quite flat before beginning to taper off after age 80. Besides longevity risk aversion, we also have aversion to future average return uncertainty to consider in planning a withdrawal strategy.

LTC – The CANNEX approach accelerates withdrawals and consumption into the early years after retirement by reducing consumption in later years, when people are less likely to be active or even alive. However, many people feel the need to hold onto savings because of the risk that they may end up needing significant long-term care (LTC), and only a small minority buy insurance for this risk. There are no easy answers about how people should make withdrawal plans in light of this risk, but it is important that clients have a plan for dealing with the LTC risk, and it may be necessary to adjust retirement spending plans in light of this risk.

Withdrawal strategies – not “one-size-fits-all”

The choice of the most appropriate withdrawal approach will differ depending on whether an advisor is involved. Those of average or below-average means likely will not be able to afford the services of a good-quality advisor, so they may have to depend on whatever generic advice their retirement plan sponsor can provide or what they can learn on their own.

The key objective of the SCL/SOA research mentioned earlier was to develop strategies for generating retirement income that can be implemented by plan sponsors without an undue burden, and utilized by employees with minimal individual guidance. The SSIR strategy involves making the most out of Social Security (delay to age 70 for individuals and coordinated strategies for couples) and utilizing a simple generic strategy such as RMDs for systematic withdrawals of remaining savings. The leader of the Stanford/SOA project, Steve Vernon, referred to guaranteed lifetime income from Social Security and any pensions or annuities as a “retirement paycheck,” and the systematic withdrawals, which will vary from year to year, as an annual “retirement bonus.” An advantage of using RMDs or RMDs times a multiplier for the bonus part is that plan sponsors already provide annual RMD information to participants. For many participants, Social Security will make up most of retirement income, so it’s questionable if more customized approaches applied to remaining savings are either needed or feasible.

At the other extreme of wealth and income are those sufficiently well off so that they can afford top-quality advisory services. These folks don’t need retirement planning based on formulas, no matter how customized. Instead, they need detailed plans, updated annually, that take into account all the nuances of their financial lives, including uneven cash flows, such as paying off a mortgage, buying or selling a second home, or providing financial support for grandchildren attending college. Those types of cash flows don’t fit into formulas.

I see possible potential for more customized formula approaches, such as the CANNEX strategy, in the middle ground currently targeted by robo-advisors or those who mix robo with limited in-person advice. However, there are a lot of challenges to determine the best ways to offer customized retirement spending advice. What CANNEX is working on is a start, but there is much more to understand.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

1 The IRS has proposed modest decreases in RMDs that will become effective in 2021. Over the age-range 65 – 90, the decreases will average about 7%. 1.6 times RMDs under new rules will produce withdrawals similar to 1.5 times with current RMD factors.

More Alternative Investments Topics >