Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

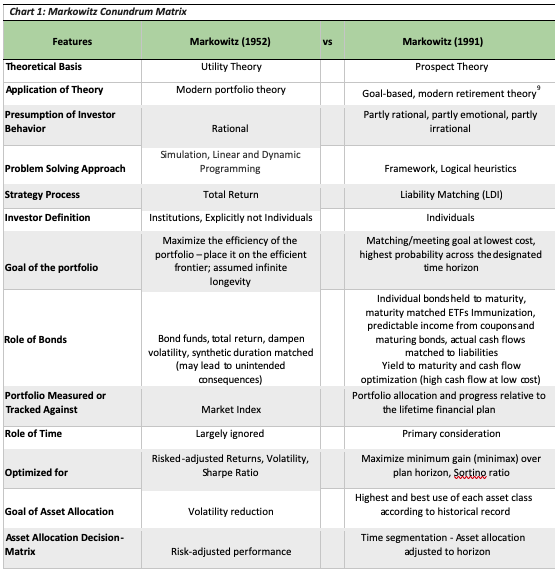

Our article, The Markowitz Conundrum, highlighted Harry Markowitz’s own personal tension as he reflected upon the way his 1952 work, Portfolio Selection1, was being applied by advisors for individuals. In 1991, Markowitz2 wrote that most investment advisors implement portfolios as if individual clients were institutions. The institutions Markowitz was originally trying to help were in the mutual fund industry.

By contrasting multiple features of Markowitz 1952 with Markowitz 1991, we offer an evaluation matrix as a tool that challenges the suitability of the advisory industry’s application of modern portfolio theory (MPT) investing for an individual’s portfolio. We hope this comparison matrix will encourage advisors to re-think the current default application of MPT for the individual investor.

MPT is rooted in utility theory’s view of the world. One of the core tenets of utility theory is that investors are rational. When the term, “investors” is applied to institutions, the investor can properly be described as rational. Institutions typically manage portfolios in perpetuity by policies and through a governance structure of highly trained and sophisticated boards.

Yet, one of the outgrowths of MPT has been the broad acceptance by all sorts of investors, without distinction to whether an investor is an institution or an individual.

In 1991, Markowitz distinctly pointed out that the term “investor” has been potentially mis-applied to also include individuals. In his words:

The “investing institution” which I had most in mind when developing portfolio theory for my dissertation was the open-end investment company or “mutual fund.”

Additionally, individuals do not typically order their personal investments through a governance structure or for a permanent time horizon. The connection between institutions and individuals is stark. Institutions are rational. However, individuals need a planning and investment approach that cannot only accommodate individual needs, emotions, and behavior, but also has been built directly for individuals, taking into considerations that they may not always behave in the same manner as institutions.

The counterargument to utility theory is Daniel Kahneman’s prospect theory3. Prospect theory acknowledges human behavior as sometimes irrational or emotional and points out that individual investors are loss averse4. The recent ascendancy of prospect theory’s application of behavioral finance offers helpful ways to deal with the characteristics of individual investors’ behavior through framing, uncovering and dealing with biases.

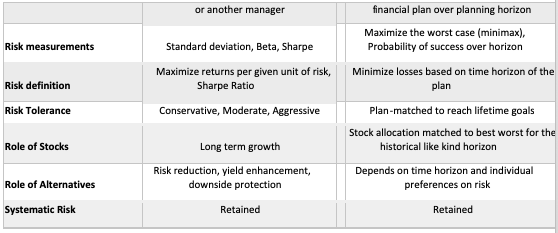

Individual investors are caught in a trap if they are using MPT, primarily because the theory demands institutional rationality and an unbound time horizon. Prospect theory exposes the dissonance in MPT’s application to individuals. For example, individual retirees do not typically exhibit institutional rationality due to errors in judgment and cognitive decline, nor do they have an unbounded time horizon.

While the bedrock take-away of Markowitz’s Portfolio Selection5, the principle of diversification, has application to individuals, expansion of this principle to individuals should be viewed skeptically. The individual investor is a derivative focus within MPT, not the primary focus.

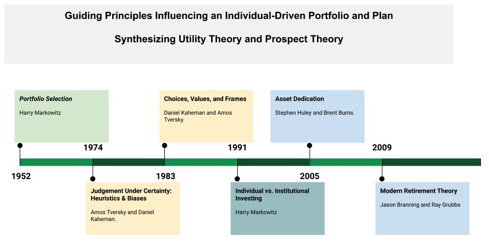

Utility theory and its antithesis, prospect theory, need a synthesis that is rooted in the individual investor. That synthesis should take the best learning from both theories and apply them to the individual investor. Advisors seeking a rational synthesis for individual investors may look to a comprehensive, guardrail-type framework for decision -making and an individually designed portfolio solution with a dedicated portfolio approach6.

One rational synthesis, built from the perspective of an individual investor, can be constructed from the best of both underlying theories. Any proposed synthesis for individual investors, especially those in or approaching retirement, should be established upon a set of particular priorities for individuals: longevity and conditions within longevity7. These priorities are then liability-matched between the plan and portfolio construction. Additionally, the plan and portfolio are matched to the individual’s hierarchy of goals over the projected time horizon.

Liability-driven investing can effectively prioritize asset allocation assignments in a portfolio because the allocation is based on the projected annual income need over the targeted portfolio horizon. For example, if an individual wanted to build her plan to weather The Great Depression, assuming she has sufficient assets, she could buy 16 years of bonds to cover essential/base expenses and then commit the balance of the portfolio to stocks. Historically, beyond 16 years, stocks would have been the cheapest asset class and most effective way to fund the income need for year 17.

Finally, a synthesis of utility and prospect theories will offer a robust solution for loss aversion. Therefore, a synthesis must exhibit safety-first guidelines,8 yet need not be safety only.

Jason K. Branning, CFP® and M. Ray Grubbs, Ph.D. are principals with MRT, LLC a retirement education firm based in Ridgeland, MS. Additionally, Jason is an investment advisory representative of Asset Dedication, LLC, an SEC registered investment advisor and Ray is a tenured professor at Millsaps College in Jackson, MS.

CHART 2: Synthesizing Utility Theory & Prospect Theory for Individual Plans and Portfolios

1 Markowitz, Harry. “Portfolio Selection*.” The Journal of Finance, vol. 7, no. 1, 1952, pp. 77–91., doi:10.1111/j.1540-6261.1952.tb01525.x.

2 Markowitz, H. “Individual versus Institutional Investing.” Financial Services Review, vol. 1, no. 1, 1991, pp. 1–8., doi:10.1016/1057-0810(91)90003-h.

3 “26.” Thinking, Fast and Slow, by Daniel Kahneman, Farrar, Straus and Giroux, 2015.

4 “Chapter 29.” Thinking, Fast and Slow, by Daniel Kahneman, Farrar, Straus and Giroux, 2015.

5 Markowitz, Harry. “Portfolio Selection*.” The Journal of Finance, vol. 7, no. 1, 1952, pp. 77–91., doi:10.1111/j.1540-6261.1952.tb01525.x.

6 Huxley, Stephen J., and J. Brent. Burns. Asset Dedication: How to Grow Wealthy with the next Generation of Asset Allocation. McGraw-Hill, 2005.

7 Branning, Jason, and Ray Grubbs. 2010. “Using a Hierarchy of Funds to Reach Client Goals.” Journal of Financial Planning’s Retirement Distribution Supplement (December). p. 31-33.

8 Pfau, Wade D. and Cooper, Jeremy, The Yin and Yang of Retirement Income Philosophies (November 10, 2014). Available at SSRN: https://ssrn.com/abstract=2548114 or http://dx.doi.org/10.2139/ssrn.2548114

9 Branning, Jason and Grubbs, Michael, Modern Retirement Theory: Reaching Client Goals in Every Market (December 1, 2009). Available at SSRN: https://ssrn.com/abstract=3419038 or http://dx.doi.org/10.2139/ssrn.3419038

10 “Safety Zones, Danger Zones, and the Critical Path: Visualizing U.S. Asset Class Returns Based on Time Horizons, Size, and Style,” published in the Retirement Management Journal, Vol. 7, No. 1 (2018).

Read more articles by Jason Branning, M. Ray Grubbs