Adoptees of bucket strategies were rewarded over the past two months, as their cash reserves have buffered them psychologically from the market decline. Such strategies avoid taking withdrawals from stocks when the market is down, as it is now. But do bucket strategies provide a financial benefit – as some claim – or are any benefits purely behavioral?

Prominent thought leaders in retirement planning advocate for bucket strategies, but there are studies that demonstrate such strategies perform poorly. However, my research shows that those studies rely too heavily on a narrow set of historical data, and should be viewed skeptically. I’ll sort out the arguments and provide results from my own analysis.

Background

The first bucket strategy was developed by financial planning pioneer Harold Evensky in 1985. This was a two-bucket approach with a cash bucket holding five years of retirement spending, and a longer-term investment bucket consisting mostly of stocks. When the stock market performed poorly, withdrawals were taken from the cash account to avoid selling stocks in a down market, and when the stock market did well withdrawals were taken from the investment bucket, and investments from this bucket were also sold to replenish cash.

The most prominent advocate for bucket strategies is Christine Benz, director of personal finance at Morningstar. The particular strategy she advocates is a three-bucket strategy – two years of retirement withdrawals in cash, an intermediate bucket of five or more years of spending held mostly in bonds, and a longer-term bucket held mostly in stocks. Again the strategy is to use cash when stocks are down and utilize the longer buckets they have performed well. This approach keeps an allocation balance between the two longer buckets.

Neither Evensky nor Benz has claimed that a bucket strategy provides superior financial performance (assuming one could agree on a definition of “superior”). They tout the primary benefits as providing peace of mind for clients and making it easier for clients to stay-the-course when investment markets are in turmoil.

Estrada study

Professor Javier Estrada of the Spanish IESE Business School has published a comprehensive 2018 study that compared three different bucket strategies to static strategies that maintain a constant asset allocation. He assumed retirement withdrawals for 30-year periods based on the classic 4% rule (level real withdrawals) and measured how the bucket and static strategies performed in terms of sustainability – i.e., whether and when the strategies ran out of money. He used historical investment performance data from 1900 to 2014 across 21 countries segmented into rolling 30-year retirement periods. His methodology and conclusions were described in detail in this 2019 Advisor Perspectives article by Larry Swedroe (see also the extensive APViewpoint conversation on his article).

Although Estrada worked with a vast amount of data, the data did not result in a lot of retirement plan failures, i.e. savings depleted before year 30. When Bill Bengen developed the 4% rule in the early 1990s, his objective was to come up with a withdrawal strategy that would not have failed historically based on U.S. data. By bringing in international data, Estrada found more plan failures, but still not a lot.

For the U.S., 30-year retirements commencing in 1966 have produced worse outcomes than any of the earlier 30-year scenarios Bengen studied, and 1966 retirements play a prominent role in Estrada’s study. I’ll focus on this specific retirement year to provide my own comparison of bucket versus static strategies. (Michael Kitces did a 2014 study on bucket strategies with particular focus on 1966 retirements, a year that has become the “poster child” for the worst year to have retired. It is notable because stocks lost approximately 70% of their inflation-adjusted value from 1966 to 1982.)

1966 retirements

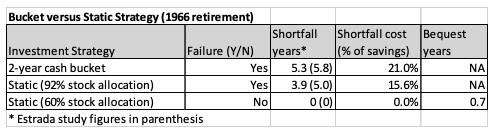

I ran a test for a 30-year retirement beginning in 1966 by using the simplest of the bucket strategies from the Estrada study. I set up an initial portfolio with cash equal to two years of withdrawals based on the 4% rule (level real annual withdrawals equal to 4% of initial savings) and the remainder of the portfolio in stocks, so the overall allocation was 92/8 stocks/cash. I assumed cash earned a real return of 1%, and year-by-year returns for stocks were from Ibbotson data for large-company stocks starting in 1966.

I used the following rules for managing the buckets:

- If the stock return for the previous year was negative, the annual withdrawal was taken from cash if sufficient cash was available.

- If the stock return for the previous year was positive, the annual withdrawal was taken from stocks and the cash bucket was refilled if needed.

I tested this bucket strategy against two static strategies that maintained a constant stock/cash mix over the full 30-year retirement. One strategy utilized a 92% stock allocation to match the initial bucket strategy allocation, and the other assumed a more typical 60% stock allocation. The results are shown in the chart below.

For strategies that failed before reaching 30 years, I measured the failure in shortfall years, e.g. 5.3 means running out of money at 24.7 years. I also included a shortfall cost measure where I state the dollar amount of the shortfall as a percentage of initial savings. For the strategy that didn’t fail, I stated the bequest amount in years to make it comparable to shortfall years. Estrada also provided a shortfall years measure and I have included his U.S. results for this measure as well.

For this particular retirement year (1966), we see that the bucket strategy performed worse than either of the two static strategies. Of those two strategies, the 60% static allocation performed better than the 92% stock allocation. So the biggest difference between static and bucket strategies from both Estrada’s and my results comes from the shift to a more favorable asset allocation rather than from the bucket-to-static shift with a similar asset allocation.

Although my results are based only on a single retirement year and the Estrada study used 86 rolling 30-year periods, about 95% of those rolling periods did not produce failures. The 1966 retirement is significant in Estrada’s total results for the U.S. This leads to the question: How can we expand the testing to obtain a more robust result, one that is not as heavily influenced by a small sample of failures?

More robust results

Estrada expanded his sampling by utilizing data from 21 countries. To the extent that other country stock performance is not perfectly correlated with the U.S., this would provide a more robust sample. He showed results for this expanded data set in his Exhibit 3. The failure rates are significantly higher than for U.S. alone, and again he showed better results for static allocations than bucket strategies. However, the performance differential for static versus buckets is much less than the results for the U.S. This leads to the question of whether there is enough of a differential to support the claim that static allocations are financially superior to bucket strategies?

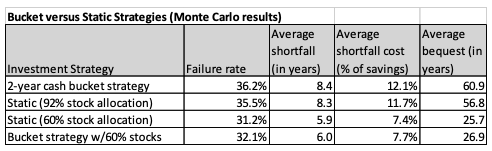

To generate more robust results, I ran an experiment using Monte Carlo-generated returns so that there were no limits on the number of independent scenarios that could be generated. I assumed stocks would produce an arithmetic average real annual return of 5% with a standard deviation of 20% and again assumed a 1% fixed return for cash. I assumed stock returns to be independent from year-to-year, and a quick check of 1926 – 2019 data showed a year-to-year correlation coefficient of -0.00069, so I was comfortable with this independence assumption.

The chart below is similar in format to the earlier 1966 chart and shows the results from the Monte Carlo runs. The average shortfall cost measure incorporates both the failure rate and the average shortfall and I consider it the best summary risk measure.

The top two lines of the chart compare the bucket strategy I described earlier with a static strategy holding the same initial asset allocation. The static strategy does slightly better on failure measures and slightly worse for bequests, but the results are virtually equivalent overall. Although my study was limited in scope, these results are at odds with Estrada’s conclusion that bucket strategies produce inferior financial results.

The bottom two lines compare a 60% stock allocation with a two-bucket strategy where the long-term bucket has been altered to a stock/bond mix so that initial portfolio mix is 60% stocks. Again the results are virtually equivalent. These results for the 60% stock allocation indicate that bucket strategies may benefit from utilizing stock/bond mixes for the longer-term investments. This can be accomplished with a two-bucket strategy by holding a stock/bond mix in the non-cash bucket or with a three-bucket strategy incorporating an intermediate fixed-income bucket. The asset allocation chosen will have a much bigger impact on outcomes than whether or not a bucket strategy is used.

Equivalence rationale

A logical argument supports the Monte Carlo results that show equivalent results. I mentioned earlier that the year-to-year historical correlation of stock returns was virtually zero. This means that there is no advantage or disadvantage gained from a bucket strategy based on one-year stock performance. In effect, a bucket strategy is equivalent to an asset allocation strategy where the investment mix varies slightly from year to year in a random manner. If one uses a static allocation that closely matches the resulting overall average investment mix in a bucket strategy, the results will be equivalent.

Bucket strategy promotion

I mentioned earlier that the two leading advocates for bucket strategies have not claimed that bucketing produces superior financial outcomes. Unfortunately, others in the advice profession have not been as restrained. I have seen claims that bucket strategies can reduce sequence of returns risk or have been shown to increase a portfolio’s longevity. It might seem logical that a strategy designed to avoid selling stocks in down markets should provide superior financial performance. However, there’s no evidence to support such claims. They depend on an assumption that year-to-year stock returns are negatively correlated, whereas the historical data shows virtually no correlation.

Conclusion

When I began this research, I thought I would be writing a negative article about bucket strategies, but now I come out in the middle. I don’t agree with the Estrada study that claims inferior financial performance for bucket strategies, but I also reject the claims by some advisors that such strategies produce superior financial performance.

If bucket strategies provide peace of mind and help clients stay with their long-term plans, then that is a positive benefit. The caveat is that the fees associated with employing bucket strategies need to be reasonable in relation to the behavioral benefits provided.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

Read more articles by Joe Tomlinson