Whether to purchase long-term care (LTC) insurance is one of the most difficult and consequential decisions a retiree will make. Because of the complexity of the products and the uncertainty of needing care, very few have attempted – as I did below – to provide an objective analysis.

I’ve written less analytically about LTC insurance and hybrid solutions for AARP, a demographic where the subject is of the utmost importance. As evidence of the contentious nature of this topic, I have no shortage of emails telling me how stupid I am.

Framework for the analysis – probabilities and net benefits

We must understand the probability of needing care and, if so, for how long and at what cost. This is a distribution curve rather than a discrete, binary “yes” or “no.” If you end up needing LTC for 100 days or less, you may pay very little. Medicare could cover most of the costs if you are admitted to a Medicare-certified nursing facility within 30 days of hospital stay of three days or longer. If you stay 10 years, however, the costs could be staggering.

All insurance companies, even mutual insurance companies, need to cover their costs (including commissions) and make a profit. Thus, the odds are that buying LTC insurance will be the “wrong” decision, in the sense that the expected benefits, net of costs (including opportunity costs one could earn if they invested the premium) will be less than zero. But that’s the same as any insurance policy. We buy insurance because the consequences of being wrong are significant. An example is a high-income earner needing term life insurance, which is likely to expire worthless, because the consequences of dying early and leaving the family exposed are just too high.

Probabilities

Here are some high-level estimates of probabilities of needing nursing home care according to a 2017 study by the non-profit research company, the Rand Corporation:

1. Approximately 56% of Americans will need at least one day of LTC but only 32% will pay anything out of pocket. The study notes the 56% needing LTC is substantially higher than previous estimates.

2. Among women, 64.1% will have some nursing home stays, versus 50.6% of men:

- Women average 301 days.

- Men average only 141 days.

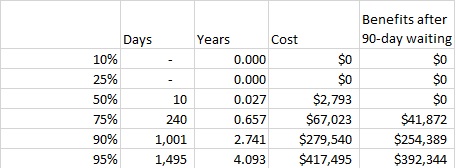

3. The probability distribution with combined genders looks as follows:

- 10th percentile – 0 days

- 25th percentile – 0 days

- 50th percentile – 10 days

- 75th percentile – 240 days

- 90th percentile – 1,001 days

- 95th percentile – 1,495 days

A 2015 US. government study provided by Lincoln Financial had slightly higher projections, but very similar numbers for the wealthiest quintile, likely to be our clients. These are estimates of needing any paid long-term services and support, which includes less intensive and less expensive care than a nursing home.

According to the Lincoln Financial Group, the national average annual cost of a nursing home is $102,000 a year. Thus, a policy with a 90-day waiting period and this amount of coverage would have about the following benefits, in today’s dollars:

There is a 5% probability of collecting $392,344 or more in benefits. The industry is quick to point the high costs, but I’ve never seen mentioned that there are also savings – especially if one is single since they would no longer need a house, car, insurance, be travelling, eating out, etc. Often one spouse becomes the caregiver, but might need care themselves later after the spouse has died. If that’s the case, they save quite a bit in expenditures.

Cost of LTC insurance – traditional and hybrid

In evaluating the decision to buy LTC insurance, I’m going to compare the costs to a bad-case scenario of a 1,495 day nursing-home stay. The two types of LTC insurance are the traditional LTC, and hybrid policies that sit on top of a life insurance chassis. I’m going to use the odds above, but those likely overstate the probabilities of needing care, because both types of LTC insurance have underwriting that tries to weed out those more likely to benefit. To make it personal, I’m evaluating policies for my wife and me with a $102,000 annual benefit. We are both 62-years old at the time of the quotes.

Traditional

To evaluate traditional LTC, I turned to Jesse Slome, executive director of the American Association for Long-Term Care Insurance. He quoted a policy with a combined annual premium of $7,587 for the $102,000 annual benefit with a 3% annual inflation escalator for the first 20 years only. My wife’s policy is far more expensive, as Slome said that roughly two-thirds of claims come from women. It has a 90-day elimination period and a five-year maximum benefit for each of us. If rates don’t increase, over 20 years, we’d pay $151,740 in premiums. Discounted at the 3% annual rate of the benefit, that amounts to about $116,262.

I made the problematic assumption that insurance rates don’t increase, given the huge increases of 50 to 100% or more some have experienced in similar policies. Slome blamed those rate increases on lower-than-expected lapse rates, lower interest rates and higher claims experiences than actuaries assumed. He was confident there will be few if any future rate increases.

I’m not so confident. Competition is lessening and I wrote in 2012 that long-term care insurance could even become extinct. Slome confirmed that there were now fewer than a dozen LTC insurance companies from a height of more than 80, as most have exited this business.

Using the probabilities previously noted from the Rand study, there is a 5% probability that each of us will have a stay of 1,495 days and collect a benefit of $392,000 or more, in today’s dollars. That translates to a 90% probability neither of us will have such an occurrence and a 0.25% probability both of us will. Should both of us spend five years or longer in a nursing home, we’d collect $1,020,000 in today’s dollars, or a benefit net of the premiums of about $903,738. Yet the probability of that happening is far less than 0.25% and is starting to approach lottery odds. A fairly bad case scenario is that one of us spends 1,495 days and collects a net benefit beyond the premiums of $276,083. And again, this is without any premium increases.

Because there would be substantial cost savings from not travelling, eating out, shopping, not needing a car or potentially even a house, we decided we can self-insure versus this option. I suspect many of our clients could as well.

Hybrid policies

Hybrid policies are gaining in popularity. These policies have several benefits, such as being able to pay up front and not having to worry about future rate hikes. They have death benefits and some allow the ability to surrender and get some of your money back. Because of these additional benefits, comparing hybrids to traditional is similar to comparing term to permanent life insurance. You can think of some hybrids as creating a pot of money that can be used for LTC or as a death benefit or even getting some of the money back while living for non-LTC needs.

I evaluated the Lincoln MoneyGuard III policy with a slightly lower $100,008 annual benefit, 3% compound inflation increases, and a seven-year benefit duration. This policy had no elimination period. Though the up-front cost was nearly four times the present value of traditional LTC insurance, at $405,036, the maximum we could collect was higher at $1.4 million in today’s dollars. We could have a net benefit of about $1 million in the incredibly unlikely event we both spend at least seven years needing care and use the maximum daily benefit.

But it’s unfair to compare the total costs to traditional. The policy has a 70% return of premium, meaning, at any time, we could surrender the policy and only be out 30% of what we paid and whatever inflation was in the meantime. In addition, there are death benefits totaling $435,080 if we each lived 20 years or longer, with higher amounts if we die earlier. Our heirs would make a small profit of about $30,000 in nominal dollars. Using life expectancy tables from the Society of Actuaries and the same 3% inflation, that amounts to only $217,393 in today’s dollars. It’s a net cost of $187,643 ($405,036 premium less the NPV of the $217,393 death benefit). It is a bit more expensive than the traditional LTC policy, but without the downside of potential rate increases.

At a 5% likelihood of needing 1,495 days (or more) of LTC, that amounts to about $409,309 in benefits in today’s dollars for each of us. It’s difficult to evaluate the net benefit after the cost of the premium, since there would be a death benefit for the person not needing long-term care.

Another way of looking at the economics is provided by Lincoln Financial in the illustrations they provided in the quote. Bill Nash, senior VP of MoneyGuard distribution, noted that using the maximum benefits for seven years starting at age 85 results in a tax-free 7.4% IRR for my wife and an 8.1% IRR for me. While I don’t think stocks will earn that return after taxes, I do believe that return has a far higher probability than using the full benefits.

With some cost savings after entering the home, I also decided to self-insure as I do for most of my clients, who are typically wealthy.

My conclusion from the numbers

If one needs LTC for an extended period, either type of policy will be very beneficial. But I don’t find the probability-adjusted benefits compelling. Buying LTC insurance has other risks, such as delaying retirement (because one has to work longer to pay for the policy), running out of money while not in a home, or even hyperinflation which, over a couple of decades, any of which would diminish the real benefits. Health care inflation currently far exceeds the CPIU. Another risk is that the government comes out with a subsidized plan that could be superior. Finally, I’ve heard stories about fights with insurance companies who have denied coverage.

Of course, it’s not a buy or don’t buy decision. I’ve reviewed two very rich policies, but one could partially self-insure by buying a scaled down version with lower benefits. Though I’d consider longer elimination periods or lower daily benefits, I wouldn’t skimp on the number of years the benefit pays out. One should buy insurance for a catastrophic event – a long stay in a nursing home.

I spoke to Michael Hurd, one of the authors of the Rand study, who told me, “One important reason most people don’t buy LTC insurance is that Medicaid provides insurance of last resort.” I’m told, however, that quality of care can vary greatly.

Beyond the numbers

While I’ve tried to make these analyses as close to comparable as possible, it’s quite imperfect with many assumptions that can be challenged.

What’s not in this analysis are life decisions. For example, I did not consider whether one would prefer to be at home and how much of a burden would it be for one spouse to have to care for the other. Potential dementia of one party could make it virtually impossible for the other spouse to be the caregiver.

Carolyn Rosenblatt, author of The Boomer's Guide to Aging Parents: The Complete Guide and web site AgingInvestor.com, said not to underestimate “caregiver burnout” among family members giving care. Still, she suggested a better plan than buying LTC insurance is to be active, eat healthy and maintain a strong social network of family and friends.

Steve Vernon, a research scholar for the Stanford Center for Longevity, author of Retirement Game-Changers, suggested discussing LTC with the entire family and having a plan for such a possibility. Family fighting over what’s best for mom or dad can be avoided by everyone agreeing on a plan.

Conclusion

There is no good solution for funding LTC. Vernon pointed out that building home equity could be a possible solution. He also observed that even a not-so-good solution is better than no solution at all.

Author’s note: In researching this piece, both data and coverage were inconsistent. Use this piece as points to consider in your own analysis. In addition to people mentioned in this piece, I appreciate the helpful contributions from Joe Tomlinson, Carolyn McClanahan, and Robert Huebscher.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

More Fixed Income Topics >