Investment Lessons from 2019

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEvery year, the markets provide us with lessons on prudent investment strategies. Many times, markets offer investors remedial courses, covering lessons it had taught in previous years. That’s why one of my favorite sayings is that there’s nothing new in investing, only investment history you don’t yet know.

The year 2019 supplied a dozen important lessons. As you may note, many of them are repeats from prior years. Unfortunately, too many investors fail to learn them – they keep making the same errors. We’ll begin with my personal favorite, one that the market, if measured properly, teaches each and every year.

Lesson 1: Active management is a loser’s game

Despite an overwhelming amount of academic research demonstrating that passive investing is far more likely to allow you to achieve your most important financial goals, the majority of individual investor assets are still held in active funds.

Last year was another in which the large majority of active funds underperformed despite the fact that the industry claims that active managers outperform in bear markets. Vanguard S&P 500 ETF (VOO) outperformed 77% of active funds in their category, returning 31.4%. Yet, 2019 provided a great opportunity for active managers to generate alpha through the large dispersion in returns between 2019’s best-performing and worst-performing stocks. For example, in terms of price-only returns, 10 stocks within the S&P 500 Index were up at least 82.6%, with two more than doubling in value. Using data from S&P Dow Jones Indices, the following table shows the 10 best returners.

To outperform, all an active manager had to do was overweight those big winners, which outperformed the index by at least 50%. On the other hand, 10 stocks lost at least 25.4%, with the worst performer losing 60% on a price-only basis.

To outperform, all an active manager had to do was underweight, let alone avoid, these dogs, each of which underperformed VOO by at least 56%.

This wide dispersion of returns is typical. Yet, despite the opportunity, year after year, in aggregate, active managers persistently fail to outperform.

The results make it clear that active management is a strategy that can be said to be “fraught with opportunity.” Year after year, active managers come up with excuses to explain why they failed and then argue that next year will be different. Of course, it never is.

Lesson 2: Diversification is always working; sometimes you like the results and sometimes you don’t

Everyone is familiar with the benefits of diversification. It’s been called the only free lunch in investing because, done properly, diversification reduces risk without reducing expected returns. However, once you diversify beyond a popular index such as the S&P 500, you must accept the fact that, almost certainly, you will be faced with periods, even long ones, when a popular benchmark index, reported by the media on a daily basis, outperforms your portfolio. The noise of the media will then test your ability to adhere to your strategy.

Of course, no one ever complains when their diversified portfolio experiences positive tracking variance (i.e., it outperforms the popular benchmark). The only time you hear complaints is when it experiences negative tracking variance (i.e., it underperforms the benchmark). As the table below demonstrates, 2019 was just such a year. To show the returns of various equity asset classes, I used the asset class funds of Dimensional. ((Full disclosure: My firm, Buckingham Strategic Wealth, recommends Dimensional funds in constructing client portfolios.)

In many ways, 2019 was similar to 1998 in that U.S. stocks outperformed international stocks, and large and growth stocks outperformed small and value stocks. What’s important to understand is that we want to see a wide dispersion of returns. If we didn’t, when one asset class performed poorly, we could expect them all to perform poorly, and to similar degrees.

Wide dispersions of returns also provide us with opportunities to rebalance the portfolio, buying the underperformers at relatively lower prices at a time when their expected returns are now higher, and selling the outperformers at relatively higher prices at a time when their expected returns are now lower. Of course, that requires discipline, which is a skill that most investors don’t possess. The table below provides one example demonstrating the importance of adhering to your plan.

Lesson 3: Valuations cannot be used to time markets

We entered 2019 with U.S. equity valuations at very high levels. In particular, the popular metric known as the Shiller CAPE 10 was at 28.3, well above the historical average of about 17. And basically, we had been above that just two other times, in the late 1920s and the late 1990s, and both were followed by severe bear markets. We did enter 2018 at around the same level, and that year saw the S&P 500 lose more than 4%.

Cliff Asness’ 2012 study on the CAPE 10 found that when it was above 25.1, the real return over the following 10 years averaged just 0.5% – virtually the same as the long-term real return on the risk-free benchmark, one-month Treasury bills, and 6.3 percentage points below the U.S. market’s long-term real return. This concerned many investors, possibly leading them to reduce, or even eliminate, their equity holdings. However, there was still a wide dispersion of outcomes – the best 10-year forward real return was 6.3%, just half a percentage point below the historical average, while the worst was -6.1%.

In addition, what many investors may not have been aware of is that when using traditional price-to-earnings (P/E) ratios, history shows there is virtually no correlation between the market’s P/E and how the market performs over the subsequent year. The following is a good reminder of that.

In December 1996, the CAPE 10 was at virtually the same lofty level at which we began 2017 (that is, 27.7). The highly regarded, at least at the time, Chairman of the Board of the Federal Reserve Alan Greenspan gave a talk in which he famously declared the U.S. stock market to be “irrationally exuberant.” That speech, given in Tokyo, caused the Japanese market to drop about 3%, and markets around the globe followed. The next three years saw the S&P 500 Index return 33.4%, 28.6% and 21.0%, producing a compound return of 27.6%.

While higher valuations do forecast lower future expected returns, that doesn’t mean one can use that information to time markets. And you should not try to do so, as the evidence shows such efforts are likely to fail. This doesn’t mean, however, that the information has no value. You should use valuations to provide estimates of returns so you can determine how much equity risk you need to take in your portfolio to have a good chance of achieving your financial goals. However, expected returns should only be treated as the mean of a potentially wide dispersion of outcomes. Your plan should be able to address any of these outcomes, good or bad.

Lesson 4: The stock market and the economy are two very different things

While the U.S. economy continued to grow during the year, avoiding a recession many had predicted, growth slowed as the economy was negatively impacted by the ongoing trade dispute with China and the uncertainty it created. While the first quarter of 2019 produced a GDP growth rate of 3.1% (up from 2018’s 2.9% rate), the second and third quarter growth rates came in at just 2.0 and 2.1%, respectively. The estimate from the Philadelphia Federal Reserve’s Fourth Quarter 2019 Survey of Professional Forecasters was just 1.7% for the fourth quarter, producing a full year estimate of 2.3%. And since the market is forward looking, we should consider that the current estimate for this year’s GDP growth is lower, at just 1.8%. The market ignored the slowing economy and turned in its best performance since 2013.

Lesson 5: Ignore all forecasts

One of my favorite sayings about the market forecasts of so-called experts is from Jason Zweig, financial columnist for The Wall Street Journal: “Whenever some analyst seems to know what he’s talking about, remember that pigs will fly before he’ll ever release a full list of his past forecasts, including the bloopers.”

You will almost never read or hear a review of how the latest forecast from some market “guru” actually worked out. The reason is that accountability would ruin the game – you would cease to “tune in.” But forecasters should be held accountable. Thus, a favorite pastime of mine is keeping a collection of economic and market forecasts made by media-anointed gurus and then checking back periodically to see if they came to pass. This practice has taught me there are no reliable economic and market forecasters. Following is a small sample from this year’s collection. I hope they teach investors a lesson about ignoring all forecasts, including those that happen to agree with their own (that’s the nefarious condition known as “confirmation bias” at work). I typically collect the ones calling for really bad things to happen – with history demonstrating that far fewer bad things happen than are predicted by gurus.

We’ll examine four predictions, beginning with this one from December 25, 2018: “Experts have warned that the volatility seen in global stock markets isn’t going to end anytime soon with numerous risks only exacerbating investor fears.” Mark Jolley, global strategist at CCB International Securities, warned: “I think the worst is yet to come next year, we're still in the first half of a global equity bear market with more to come next year.” Simon MacAdam, global economist at Capital Economics, warned investors, “Many of the financial and economic indicators that turn first around business cycle peaks are now flashing red in advanced economies.” He added, “This is consistent with our view that the recent loss of momentum in the world economy will develop into a more severe slowdown in 2019.” Investors who were scared off by such warnings missed out on the strongest market for U.S. stocks since 2013.

Our next forecast comes from Goldman Sachs, often called “the smartest guys in the room.” On January 7, 2019, they advised investors to bet on a weaker dollar after comments from Federal Reserve Chairman Jerome Powell boosted the chances that the central bank would pause interest rate increases. Strategist Zach Pandl wrote: “Combined with net softer US data for December, we think a more data-dependent Fed creates space for further dollar downside. We’re therefore recommending short DXY (or a basket with approximately these weights), with an initial target of 93.0.” What is particularly interesting about this forecast is that Goldman got it right in terms of the Federal Reserve’s actions. Not only did the Fed stop raising rates, but they eventually cut them three times during 2019. Despite those cuts, the market ignored Goldman’s warning and DXY ended the year at 97.

Our third forecast comes from well-known economist and asset manager Gary Shilling, who warned investors that “the slowing global economy is heading toward a period of deflation and likely recession.” The markets ignored Shilling, as the rate of change in the CPI was basically unchanged, and there wasn’t anything close to a recession.

Our fourth forecast comes from Bob Doll of Nuveen. Doll forecasted that the market would be up 8% and that bonds would be flat. While he got the stock market’s direction right, that isn’t saying much, as the S&P has provided negative returns in just 15 of the last 70 years. And his forecast of an 8% return was more than 30% below the average annual return of the market, which is 11.9%. His forecast for bonds was way off too, with Vanguard’s Long-Term Treasury ETF (VGLT) returning about 15%. Doll’s advice on where to look for the best returns was also off the mark. He warned: “Advisors should diversify across asset classes and geographies. He argued that one “just can’t buy large-cap U.S. equities.” He added, “You once did well with that strategy, but now you have to be more diversified.” He was wrong on both counts because not only did U.S. stocks far outperform international stocks, large stocks outperformed small stocks in the U.S. (see Dimensional table above).

To be fair, there were some forecasts that turned out right. For example, Gary Shilling’s aforementioned forecast of deflation and recession led him to forecast a sharp drop in interest rates. He was right, at least directionally, as he forecasted that the 10-year Treasury would fall from around 2.7% to 1%. It ended the year at around 1.9%. And Peter Hayes and Sean Carney of BlackRock wrote about “great expectations” for municipal bonds in 2019, recommending longer-duration bonds. Their forecast was based on a net negative supply of municipal bonds accompanied by greater demand for them from investors, and an accommodative Fed. Vanguard’s Long-Term Tax-Exempt Bond Fund (VWLTX) returned about 8.5%, outperforming shorter-term bonds.

Lesson 6: “Sell in May and go away” is the financial equivalent of astrology

One of the more persistent investment myths is that the winning strategy is to sell stocks in May and wait until November to buy back into the market. Let’s look at the historical evidence. Using Ken French’s data library, since 1926 it is true that stocks have provided greater returns from November through April than they have from May through October. That may be the source of the myth. The average premium of the S&P 500 Index over one-month Treasury bills averaged 8.4 percentage points per year over the entire period. And the average premium of the portfolio from November through April was 5.7% compared to just 2.5% for the May through October portfolio. In other words, the equity risk premium from November through April has been more than twice the premium from May through October. Furthermore, the premium was negative more frequently for the May through October portfolio, with 34% of the six-month periods having a negative result compared to 27% of the six-month periods for the November through April portfolio.

From 1926 through 2018, the S&P 500 Index returned 10.0% per year. Importantly, the May through October portfolio had a positive equity risk premium of 2.5% per year, which means the portfolio still outperformed Treasury bills on average. In fact, a strategy that invested in the S&P 500 Index from November through April, and then invested in riskless one-month Treasury bills from May through October, would have returned 8.3% per year from 1926 to 2018, underperforming the S&P 500 Index by 1.9 percentage points per annum. And that’s even before considering any transactions costs, let alone the impact of taxes (you’d be converting what would otherwise be long-term capital gains into short-term capital gains, which are taxed at the same rate as ordinary income).

Let’s see how the strategy performed in 2019. The S&P 500 Index returned 3.4% from May through October, outperforming riskless one-month Treasury bills (which returned 0.9%) by 2.5 percentage points. While the last year the “sell in May” portfolio outperformed the consistently invested portfolio was 2011, you can be sure that, come next May, the financial media will be raising the myth once again.

A basic tenet of finance is that there’s a positive relationship between risk and expected return. To believe that stocks should produce lower returns than Treasury bills from May through October, you would also have to believe that stocks are less risky during those months – a nonsensical argument. Unfortunately, as with many myths, this one seems hard to kill off.

Lesson 7: Inflation wasn’t, and isn’t, inevitable

One of the most persistently asked questions I’ve received since 2009 has been some version of the following: “What should I do about the inevitable rampant inflation problem we’re going to face because of the huge fiscal and monetary stimulus that’s been injected into the economy?” While that risk has existed, the fact is that since 2008, we haven’t had a single year in which the CPI exceeded 3%. In fact, 2011 is the only year it exceeded 2.5%.

A related myth persists among many investors as well. I frequently hear concerns about the exploding growth rate of our nation’s money supply. This belief likely has been fueled by certain commercials – you know, the ones that recommend buying gold because central banks are printing money like we’re experiencing Weimar Germany all over again.

The fact is that M2, a broad measure of the money supply, hasn’t been growing at rates that suggest rampant inflation should be expected. For the 10-year period from December 21, 2009, through December 16, 2019, the Federal Reserve Bank of St. Louis reports that the rate of growth in M2 was 6.2%.

Since, as Milton Friedman, one of our greatest economists, noted, “Inflation is always and everywhere a monetary phenomenon,” the factual data doesn’t support the view that we should have expected rampant inflation. In fact, despite the fears of many investors who seem certain we will see massive inflation, neither the bond market nor professional economists are expecting anything of the kind.

We can at least get an estimate of the market’s forecast for inflation by looking at the difference between the year-end 1.9% yield on 10-year nominal bonds and the 0.2 yield on 10-year Treasury Inflation-Protected Securities, or TIPS. The difference is just 1.7 percentage points. Clearly, investors, in aggregate, don’t appear concerned about rampant inflation. As for economists’ expectations, the Federal Reserve Bank of Philadelphia’s Fourth Quarter 2019 Survey of Professional Forecasters has a 10-year forecast of inflation averaging just 2.2% at an annual rate. Again, they don’t believe rampant inflation is likely, let alone inevitable.

Don’t get the wrong idea – the risk that inflation could increase dramatically is still present. It hasn’t happened so far because, even though the monetary base has been increasing rapidly (as the Fed’s balance sheet expanded through its bond-buying program), the velocity of money (as measured by M2) has fallen pretty persistently from about 2.0 at the end of 2007 to just under 1.5 at the end of 2019, a drop of 25%.

That said, there remains the risk that if or when the velocity of money begins to rise, inflation could increase. Of course, the Fed is well aware of this risk and would likely act – reverse its bond-buying program and raise interest rates – to prevent inflation from taking off.

Lesson 8: They are called “risk premiums” for a reason

Many investors have been bemoaning the fact that the value premium – the excess return of value stocks relative to growth stocks – seems to have disappeared, turning negative for the past decade in the U.S. – although all of the outperformance has come in the last three years.

The trouble with this line of thinking, however, is that stock returns are extremely noisy from a statistical perspective. Thus, even a decade isn’t long enough to make a definitive statement about any strategy that invests in a risky asset class or investment factor. In fact, the historical evidence demonstrates that all risky assets/factors experience long periods of underperformance. If that were not the case, there would be no risk for long-term investors, and there should be no other kind. The following example makes this point.

The table below shows the performance of value stocks and the S&P 500 Index for various periods ending in 1999. (Fama-French data is from Ken French’s website.)

As you can see, U.S. value stocks underperformed over each of the periods. And the data even looks similar to today’s figures in terms of the performance gap. Now let’s jump forward just one year, to the end of 2000, and see how the world looked.

Moving forward just one single year, we find that value stocks now outperformed over each of the periods. The lessons are that there is a lot of volatility in factor performance and that even long periods of underperformance can be reversed over very short timeframes.

Let’s turn now to some other examples of risky assets performing poorly over very long periods.

Consider the nine-year period from 2000 through 2008, when the S&P 500 Index lost 28% and underperformed riskless one-month Treasury bills (which returned 31%) by a total of 59 percentage points. Even over the longer 13-year period 2000 through 2012, one-month Treasury bills outperformed the S&P 500, 1.7% versus 2.1%. The S&P 500 also underperformed one-month bills over the 15-year period ending 1943 (0.6% versus 0.7%) and over the even longer 17-year period ending 1982 (6.8% versus 7.1%). Cumulatively, those three periods represent half of the last 90 years. Hopefully, such long periods wouldn’t prove long enough to convince you that stocks shouldn’t be expected to outperform one-month Treasury bills. Consider the even longer 40-year period from 1969 through 2008, when the U.S. total stock market (CRSP 1-10 Index) returned 8.8% and underperformed the 8.9% return of long-term U.S. Treasury bonds. And in case you are wondering how those recently outperforming growth stocks did over that same 40-year period, the Fama-French U.S. Large Growth Research Index returned 8.5%, and the Fama-French Small Growth Research Index returned just 4.7%. (Data is from Ken French’s Data Library.)

Consider also the performance of international and emerging market stocks, which have underperformed over the most recent 10-year period. Using data from Portfolio Visualizer, for the period 2010 through 2019, the Vanguard Total [U.S.] Stock Market ETF (VTI) returned 13.3% per year, outperforming both the Vanguard FTSE Developed Markets ETF (VEA) and the Vanguard FTSE Emerging Markets ETF (VWO), which returned 6.1% per year and 7.5% per year, respectively.

Many investors will take a look at such performance and conclude that investing internationally is a bad idea. After all, 10 years is a long time to them. However, we get an entirely different view if we move back in time and look at the performance of the prior seven years, from 2002 through 2008.

During this period, again using data from Portfolio Visualizer, the Vanguard 500 Index Fund (VFIAX) lost 1.6%, underperforming the Vanguard Developed Markets Index (VTMGX), which returned 4.0%, by 5.6 percentage points a year, and the Vanguard Emerging Markets Stock Index (VEIEX), which returned 10.9%, by 12.5 percentage points a year. An investor making decisions at the start of 2009 based on the prior seven years of performance would have made a very poor choice. The lesson is that all risky assets go through long periods of underperformance.

Unfortunately, far too many investors put too great an emphasis on recent, short-term performance when considering investment decisions. The media tends to exacerbate the problem as opposed to helping investors stick to a disciplined strategy.

Chasing past performance can cause investors to buy asset classes after periods of strong recent performance, when valuations are relatively higher and expected returns are lower. Alternatively, it can lead investors to sell asset classes after periods of weak recent performance, when valuations are relatively lower and expected returns are higher.

In fact, investors who chase recent performance are systematically buying high and selling low. A better approach is to follow a disciplined rebalancing strategy that systematically sells what has performed relatively well recently and buys what has performed relatively poor recently.

When evaluating your asset allocation, recent performance should not be a factor in the decision. Smart investors know that all investment strategies that entail risk-taking will have bad years, or even many bad years in a row. That’s the nature of risk. After all, if this wasn’t the case, there wouldn’t be any risk. With that knowledge, smart investors know that recency is their enemy, and patience and discipline (accompanied by rebalancing) are their friends.

Lesson 9: The world isn’t flat, and the diversification of risky assets is as important as ever

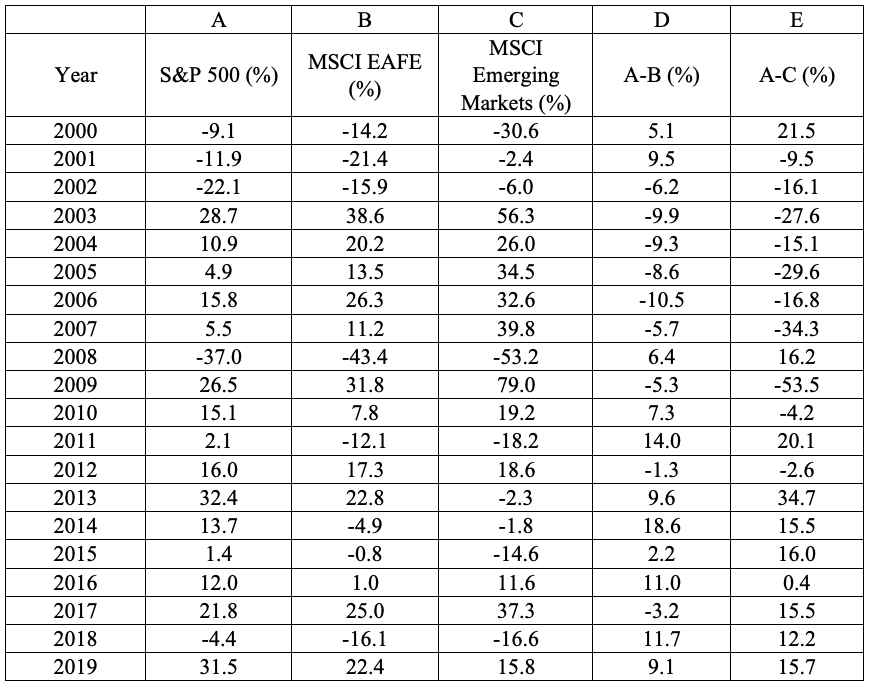

The financial crisis of 2008 caused the correlations of all risky assets to rise toward one. This led many in the financial media to report on the “death of diversification” – because the world is now flat (interconnected), diversification no longer works. This theme has been heard repeatedly since 2008. Yet, diversification benefits come not just from correlations, but the dispersion of returns as well. And wide dispersion of returns in almost every year since 2000 demonstrates there are still large diversification benefits.

There were only three years of the 20 when the difference in returns between the S&P 500 Index and the MSCI EAFE Index was less than 5%. On the other hand, there were 11 years when it was at least 8%. There were also only three years when the return on the S&P 500 Index was within 10% of the return of the MSCI Emerging Markets Index. There were seven years when it was at least 20% and three when it was at least 30%. The largest gap was more than 53%.

The data presents powerful evidence that the investment world is far from flat and that there are still significant benefits in international diversification.

Lesson 10: The road to riches isn’t paved with dividends

Despite the fact that traditional financial theory has long held that dividend policy should be irrelevant to stock returns, over the last 10 years we’ve seen a dramatic increase in investors’ interest in dividend-paying stocks. This heightened attention has been fueled both by hype in the media and the current regime of interest rates, which are still well below historical averages.

The low yields available on safe bonds have led even once-conservative investors to shift their allocations from such fixed income investments into dividend-paying stocks. This is especially true for those who take an income, or cash flow, approach to investing (as opposed to a total return approach, which I believe is the right one).

How did that strategy work in 2019? According to data from S&P Dow Jones Indices, the 423 dividend-paying stocks within the S&P 500 Index (equal weighting them) returned 29.2%, underperforming the non-dividend payers, which returned 33.6%, an outperformance of 4.4 percentage points. In addition, Vanguard’s High-Dividend ETF (VYM) returned 24.2%. It has also underperformed the S&P 500 in seven of the last eight years (the exception was 2016). And over the last 10 years, VYM returned 12.9% per year, underperforming VFIAX (Vanguard’s 500 Index Fund), which returned 13.5%.

Lesson 11: The correlation of returns of stocks and bonds is time varying

From 1926 through 2019, using Ken French’s Data Library, the correlation of the S&P 500 Index to long-term (20-year) Treasury bonds has been close to zero (0.07). A zero correlation means that when stock returns are higher (lower) than their historical average, it’s a coin toss whether long-term Treasury bonds will also provide higher (lower) returns than their historical average. And correlations are time varying.

In 2019, both provided above average returns. While VOO (Vanguard’s S&P 500 ETF) returned 31.5%, VGLT (Long-Term Treasury ETF) returned 14.3%. On the other hand, in 2008 the S&P 500 lost 37% while long-term Treasury bonds returned almost 26%. Investors should also be aware that they can both produce negative returns at the same time. There have been five years when both the S&P 500 Index and long-term Treasury bonds produced negative returns (1931, 1969, 1973, 1977 and 2018). The worst of those years was 1969, when the S&P 500 lost 8.5% and long-term Treasury bonds lost 5.1%. There have been 20 years when the S&P 500 produced a positive return and long-term bonds produced negative returns. And finally, there have been 18 years when the S&P 500 produced negative returns and long-term bonds produced positive returns.

The lesson is that correlations are time varying. And given the historically high valuations of stocks and the historically low level of interest rates, investors should not lose sight of the fact that there have been times when longer-term bonds have not provided shelter from the storm-rocking equities.

Lesson 12: Don’t let your political views influence your investment decisions

One of my more important roles as director of research at Buckingham Strategic Wealth and Buckingham Strategic Partners involves helping prevent investors from committing what I refer to as “portfolio suicide” – panicked selling resulting from fear, whatever the source of that fear may be. The lesson to ignore your political views when making investment decisions is one that rears its head after every presidential election. In fact, it became much more of an issue after the 2016 election because of the divisive views held by many about President Trump.

We often make mistakes because we are unaware that our decisions are being influenced by our beliefs and biases. The first step to eliminating, or at least minimizing, such mistakes is to become aware of how our choices are impacted by our views, and how those views can influence outcomes. The 2012 study “Political Climate, Optimism, and Investment Decisions,” by Yosef Bonaparte, Alok Kumar and Jeremy Page, showed that people’s optimism toward both the financial markets and the economy is dynamically influenced by their political affiliation and the existing political climate. Among the authors’ findings were:

- Individuals become more optimistic and perceive the markets to be less risky and more undervalued when their preferred party is in power. This leads them to take on more risk, overweighting riskier stocks. They also trade less frequently. That’s a good thing, as the evidence demonstrates that the more individuals trade, the worse they tend to do.

- When the opposite party is in power, individuals’ perceived uncertainty levels increase and investors exhibit stronger behavioral biases, leading to poor investment decisions.

Now, imagine the nervous investor (and I had discussions with many of them) who reduced their allocation to equities (or even went to zero) based on views about the Trump presidency. While investors who stayed disciplined have benefited from the market’s very strong performance over the past three years (with the S&P 500 providing a total return of more than 50%), those who panicked and sold have not only missed the bull market but have persistently faced the incredibly difficult task of figuring out when it would once again be safe to invest.

Similarly, I know of many investors with Republican leanings who were underinvested once President Obama was elected. Over the past three years, it is Democrats who have had to face their fears. The December 2016 Spectrem Affluent Investor and Millionaire Confidence surveys provided evidence of how political biases can impact investment decisions.

Prior to the 2016 election, with a victory for Hillary Clinton expected, those identified as Democrats showed higher confidence than those who identified as Republicans or Independents. This completely flipped after the election. Those identified as Democrats registered a confidence reading of -10 while Republicans and Independents showed confidence readings of +9 and +15, respectively.

If you lose confidence and sell, there’s never a green flag that will tell you when it’s safe to get back in. Thus, the strategy most likely to allow you to achieve your goals is to have a plan that anticipates there will be problems and to not take more risk than you have the ability, willingness and need to assume. Additionally, don’t pay attention to the news if doing so will cause your political beliefs to influence your investment decisions.

Summary

Even smart people make mistakes. What differentiates them from fools is that they don’t repeat the same behaviors, expecting different outcomes. This year will surely offer us more lessons, many of which will be remedial courses. And the market will provide opportunities to make investment mistakes. You can avoid making errors by knowing your financial history and having a well-thought-out plan. Reading my book Investment Mistakes Even Smart Investors Make and How to Avoid Them will help prepare you with the wisdom you need. And finally, consider including in your new year’s resolutions that you will learn from the lessons the market teaches.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All