Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Investors lose massive amounts due to panic selling in down markets. More can be done about this perennial problem.

This article identifies one critical action that can be taken to stem panic-driven losses. That action is based on a full understanding of the timing, cause and prudent use of financial instruments that can avoid much of the loss.

To appreciate the solution, it is essential to agree on what the problem really is.

Understanding the problem

Understanding begins with knowing when the losses occur.

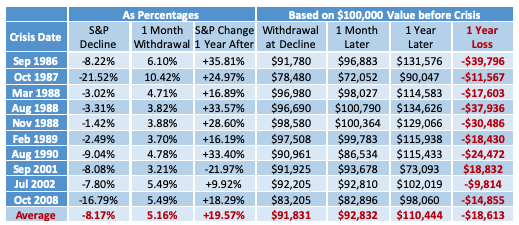

More than 70% of losses over the last 35 years originated in 10 very short crisis periods. Those crisis-period losses were then compounded in succeeding years because the loss lowered the investment during the crisis periods.

The timing of losses is evident from the increased withdrawal concurrent with each of these crisis periods, compared to market conditions that followed (measured by the S&P 500). These withdrawal rates all exceed the normal withdrawal rate of 2.70% per month. The normal 2.70% rate is sustainable by market appreciation and additional investments. The average for the crisis periods (5.16%) is not sustainable. The difference (2.46%) is driven by approximately 3.2 million households, or about three of every 100 clients who panic in each crisis.

The 10 periods that comprised the 70% of the losses were:

The historical data favors remaining invested in nine out of 10 cases. The prudent response to those crises was to take no action during the market turmoil. However, a panicked investor is more likely to focus on the exceptions:

- October 1987: Markets continued to decline after initial loss; and

- September 2001: Markets had not recovered after a year.

Even in those cases where withdrawal was wise, reentry into the market still carried unknown risks.

While these high-profile crises illustrate extremes and represent over 70% of lost returns, the remaining 30% should not be ignored. The most recent 35-year (420-month) history shows a pattern that underscores the conclusion from the 10 crises: The prudent course was to take no action.

In the overwhelming number of cases, recovery took place in a short time:

- 65.0% in 1 month

- 76.9% in 2 months

- 85.3% in 3 months

- 93.0% in 12 months

- 95.8% in 24 months

- 100.0% in 67 months

This history of quick recoveries suggests that if a withdrawal is done, reentry should take place within the first month to capture the bounce that usually takes place immediately after a decline.

Root cause

The withdrawals that result in the material loss of return are brought about by panic. The panic occurs when the investor fears loss, fueled by reinforcement from various sources, including press coverage, promotional material, social media, friends and family, investor statements, websites, phone centers and HR Benefits departments.

The common problem is that the panicked investor is offered no alternative but to withdraw, resulting in a loss of return.

Failed attempts at solutions

Great efforts have been expended over the last 25 years to curb irrational selling in the face of market declines. Those efforts have been successful when investors are open to rational and objective arguments.

The efforts have failed to address the problem of the momentarily irrational investor who acts out of fear. The following critique explains the reasons for the failures and why another more appropriate solution is necessary.

Underlying these failures are four false assumptions about panicked investors:

1. False assumption: We need to educate investors

- Need for education as a preemptive solution undoubtably exists, but is unrelated to the panicked investor who has a “fight or flight” mindset.

- Faced with mortal financial danger:

- Educated investors still panic

- Human instinct is fight or flight

2. False assumption: Investors need a better assessment of risk

- Risk tolerance evaporates in the face of panic

3. False assumption: Investors need the funds

- Yes, some but not all. Less than 50% of withdrawals during crisis are used to satisfy current economic needs.

4. False assumption: Investors have a better alternative

- This is untrue, since most proceeds go to cash/equivalents.

Any effective solution to the panicked withdrawal must occur while panic still exists, before the withdrawal mistake is made. The solution requires:

- Preparation to recognize the panic;

- Coverage at every point of contact with the panicked investor; and

- An alternative that avoids further loss.

Detecting the panic

Preparation requires the ability to recognize the panic without probing questions that could trigger panic by asking them. Asking an investor, “Are you panicked?” can cause that investor to panic!

Preparation is necessary for both human and electronic contacts. This preparation involves careful observation of what an investor says and does as well as carefully worded questions that reveal the panic.

A summary of a panic detection strategy is presented in the “i-PRT Advisor’s Guide, A key to improving investor returns & asset retention.”

Points of contact

The panicking investor will reach out in the most comfortable way to withdraw from the market. This will typically be a familiar point of contact where trust is high. The point of contact the investor chooses must be capable of detecting the panic and have a process in place to manage it. After panic is detected, the investor may be redirected elsewhere if the point of contact is inappropriate for the situation at hand.

Points of contact include human contacts:

- Advisors

- Sales assistants

- Phone center representatives

- HR Benefits managers

- Online chats

- E-mail

- Recipients of written correspondence

Technology contacts:

- Websites

- Interactive voice response (IVR) systems

- Mobile apps

Every point of contact should be capable of detecting the panic, preventing a worsening of the situation and either redirecting the investor or presenting an alternative that will protect the remaining assets.

The better alternative

An essential requirement to avoiding the cost of panic is offering a credible alternative that is aligned with the investor’s state of mind. The overwhelming concern for panicked investors is the fear of more losses.

Most investors are aware that withdrawal will achieve this protection, but few know of other alternatives for relief.

Market testing has shown that offering a solution that provides protection will generally be received positively. It demonstrates an understanding of what the investor is feeling.

Of the many financial alternatives, the one best suited for the panicked investor was found to be an index put. With a simplified description tailored to the investor’s specific situation and offered during the panic, the investor readily accepts the protection without forfeiting the appreciation that is very likely to follow.

Using puts for investment protection is not a new strategy, but it is new to retail investors. When used to relieve investors’ temporary panic, certain guidelines are required to avoid speculation and ensure that investors take no unnecessary risk:

- Use only index puts that are the best match to the investor’s portfolio. Index puts provide the liquidity and simplicity that is appropriate for retail investors.

- Protect only the volatile portion of the portfolio. Assets allocated to cash and fixed income do not need this protection and simply increases the cost of the protection.

- Puts should be limited to what is needed to avoid further losses. Beyond this point, puts become speculative and costly.

The alternative to making the withdrawal mistake is best described to an investor as insurance against further losses. I recommend the following practices when offering this alternative:

- Offer only in response to an investor’s expressed desire to withdraw funds. The index put is not an alternative to an investment or risk-management strategy. Its use is intended for investors seeking to abandon their investments in response to recent market losses.

- Make it clear to investors that the strategy is seldom the best economic alternative. The best choice is most often to take no action. It is used only when the best choice is off the table due to the investor’s fear of market conditions.

- Emphasize that the index put protection is a preferable to withdrawal.

- Explain that the strategy is never an answer to long-term concerns. Such concerns are far more effectively handled by investment or financial planning practices.

This alternative strategy has been further developed into an online tool and is described in greater detail here.

Louis S. Harvey is the CEO of DALBAR. He can be reached at [email protected] or via TWITTER at @LouHarvey44

Read more articles by Louis S. Harvey