Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Baby Boomers are arriving at retirement with large accumulations that have not yet been exposed to federal income tax (FIT) and are grappling with ways to access those assets without incurring inordinate tax bills. The 2017 Tax Cuts and Jobs Act contains provisions that enable Boomers to liberate their pre-tax assets at highly favorable tax rates. I describe a program that synchronizes the distribution of pre-tax assets with availability of generationally-low tax rates, while keeping the dictates of Medicare, Social Security and the governing IRS tax code firmly in view.

The program is suitable for Baby Boomers confronting retirement with large pre-tax accumulations. Importantly, the program is designed to avoid the Income-Related Monthly Adjustment Amounts (IRMAA) that can raise Medicare Part B and Part D premiums in retirement by over 140%. I show how to open up headroom for the planned distributions by deferring income and capital gains on the Boomer’s taxable investments. I also discuss the chronology related to the moving parts of the program.

Introduction

Since the 1970s, Congress has passed numerous bills meant to encourage retirement savings by deferring taxation on contributions and subsequent earnings. In addition to the “alphabet soup” of tax-qualified 401(a), 401(k) and 403(b) plans enabled in eponymous sections of the tax code, various other deferred-compensation arrangements and employee stock option plans can contribute to Boomer pre-tax balances. According to the Investment Company Institute, a trade group, $17.6 trillion was held in defined-contribution and IRA plans alone as of March of 2019, about half owned by Baby Boomers (i.e., those born between 1946 and 1964). Fidelity reports that the number of its own customers with a 401(k) balance of $1 million or more jumped to a record 196,000 in the second quarter of 2019.

The 2017 Tax Cuts and Jobs Act

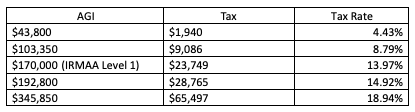

The 2017 Tax Cuts and Jobs Act reduced tax rates across the board and made other changes to the tax code. For a married couple taking the standard deduction of $24,400, the following are the applicable 2019 tax rates at key income breakpoints:

During the remaining years of the 2017 Tax Cuts and Jobs Act, taxpayers with an adjusted gross income at the $170,000 level can expect to pay an average tax rate of about 14%.

Medicare considerations

Since 2011, couples on Medicare with a modified adjusted gross income (MAGI) over $170,000 have been paying an additional monthly premium or IRMAA for their Medicare Part B and D coverages. (MAGI is calculated as adjusted gross income (AGI) plus tax-exempt interest income.) (According to the Centers for Medicare and Medicaid Services, IRMAA affects fewer than 5% of current Medicare beneficiaries.) In order to avoid IRMAA, MAGI must not exceed $170,000. (IRMAA is invoked if MAGI exceeds $170,000 by even a dollar.) In order to maximize the amount of MAGI available for the liberation of pre-tax assets, competing sources of taxable income must be removed or deferred to the extent possible.

Taxable investments

In order to open up MAGI headroom, Boomers could reposition their taxable investment accounts to defer income and capital gains indefinitely by only holding zero-dividend stocks (like Berkshire Hathaway Inc. Class B (BRK.B) and Alphabet Inc. Class A (GOOGL)). Were they to keep holdings in the form of mutual funds or ETFs, they would lose control to the fund manager of the realization of capital gains and losses. More importantly, they would not get to deduct internal fund losses instigated by the fund manager that exceed internal fund gains. Boomers may also want to reconsider their use of tax-exempt bonds since tax-exempt interest is part of MAGI.

Social Security considerations

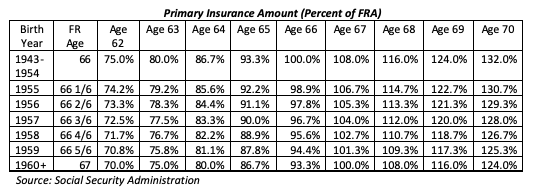

To free up additional MAGI, Boomers should consider delaying receipt of Social Security until age 70, whereupon benefits increase by up to 32% over the amount available at full retirement age (between 66 and 67 for Boomers; see table below). The obvious disadvantage to delaying Social Security benefits, of course, is that the recipient collects benefits for a shorter period of time. Anyone considering such a delay should first perform the appropriate break-even analysis using a realistic estimate of remaining life expectancy that reflects the person’s particular health situation and lifestyle.

Required minimum distributions

Required minimum distributions (RMD) are distributions a taxpayer must make from tax-deferred retirement plans like 401(k) and IRA plans annually starting in the calendar year he or she reaches 70.5 years of age. For someone turning 70 in the calendar year they turn 70.5, the initial required distribution is 3.65% of assets, increasing to 5.35% after ten years. RMDs can be burdensome or inconvenient to taxpayers. Enacting a program to liberate pre-tax assets prior to age 70.5 can reduce or eliminate a taxpayer’s ultimate exposure to required minimum distributions.

Tax payments

A married couple taking distributions from their pre-tax assets equal to the 2019 IRMAA limit of $170,000 would incur a tax bill of $23,749, as shown above. The couple could simply direct their broker/administrator to tax-withhold the $23,749 from proceeds, leaving the remainder for household needs. To the extent such post-tax amounts are in excess of household needs, the couple could direct moneys to a Roth IRA. Actually, the couple could direct the entire $170,000 to a Roth IRA. In this case, money to pay taxes and for household needs would have to come from outside sources. A year-by-year program of partial Roth conversions up to the annual IRMAA limit in conjunction with a taxable investment account positioned to maximally defer taxable income and capital gains can be a powerful way to build wealth for heirs in a highly tax-efficient manner.

Investor suitability

The objective of this strategy is to synchronize the distribution of pre-tax assets with availability of generationally-low tax rates, while keeping the dictates of Medicare, Social Security and the governing IRS tax code firmly in view. The strategy is suitable for taxpayers with substantial headroom in their yearly MAGI that would be necessary to make the strategy viable. Retirees in their early 60s with the ability to control their MAGI are especially suitable for the strategy.

Method

Joe Boomer was born on January 1, 1956 and retired on December 31, 2018 with $1,190,000 in his company 401(k) account. Joe is in good health and plans to delay receipt of Social Security until January 1, 2026, when he turns 70. He qualifies for the maximum Social Security benefit which is expected to be about $48,000 per year in 2026. He turns 70.5 in 2026 and therefore would be required to begin RMDs in that year. Outside of a non-interest-bearing checking account and his primary residence, Joe has no other assets or taxable income.

Joe decides to begin an orderly program to convert his 401(k) account to a Roth IRA in order to enjoy the favorable tax rates under the 2017 Tax Cuts and Jobs Act, which expires in 2025. Joe wants to keep taxable distributions at $170,000 each year to avoid IRMAA. He calculates that his Social Security benefit will be sufficient income for him and his wife once he reaches age 70.

Joe realizes that he will need liquid assets to pay Roth conversion taxes, his Medicare premiums and for household needs. For 2019, the first year of the program, these outlays are:

Ignoring interest and inflation, Joe would need a balance in his non-interest-bearing checking account of about $450,000 to fund seven years of outlays. He and his wife plan to sell their primary residence for $450,000, its assessed value, and relocate to a rental property in a low-cost state in the American southwest.

After seven years, at the January 1, 2026 completion of the program, Joe will have successfully redirected the entirety of his 401(k) assets into a Roth IRA, fully satisfied his FIT obligations at a highly favorable tax rate, and positioned his Roth IRA for years of tax-free growth and ultimate delivery to his heirs as a tax-free inheritance. Since Joe is in good health, he might live for twenty years or more after he reaches age 70. Assuming a real return of 6.5% per year for stocks, he very well might pass along a tax-free estate in excess of $4 million (2019 dollars) to his heirs.

Furthermore, he will have commenced Social Security at the maximum possible benefit and avoided any exposure to RMDs or to IRMAA exactions. His sole taxable income will be his $48,000 Social Security benefit, thereby incurring a total FIT rate of about 5%.

Joe and his wife will rely on Medicare during retirement. Generally, Medicare pays 80% of doctor and/or hospital bills, leaving the rest up to Joe. He feels comfortable that his Roth IRA balance can safely be tapped for Medicare co-pays if need be. (Joe also takes comfort in the knowledge that medical expenses are tax-deductible to the extent that they exceed 7.5% of his adjusted gross income.)

Potential pitfalls

Changes to the tax code could undercut this kind of liberation program. For example, Congress could raise tax rates prior to 2026 or limit the attractiveness of a Roth IRA. Congress could also reduce Social Security benefits or make the IRMAA more burdensome.

Conclusion

The 2017 Tax Cuts and Jobs Act presents a generational opportunity to liberate pre-tax assets at highly favorable tax rates. It is possible to devise a program to methodically tap pre-tax assets in a manner that observes the dictates of Medicare, Social Security and the governing IRS tax code. Baby Boomers approaching retirement with large pent-up pre-tax accumulations can benefit from this type of liberation program.

Anson J. Glacy, Jr., ASA, CERA, CFA, is a financial professional with extensive risk management and value optimization experience in the consulting, asset management and corporate settings. He presently serves as managing director at Prescriptive Analytics GmbH

Read more articles by Anson J. Glacy, Jr.