Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Since the financial crisis, households have de-levered while federal debt has marched upwards. But the net cost of the combined debt, measured as the “cost of carry,” is at a level that historically signals an oncoming recession.

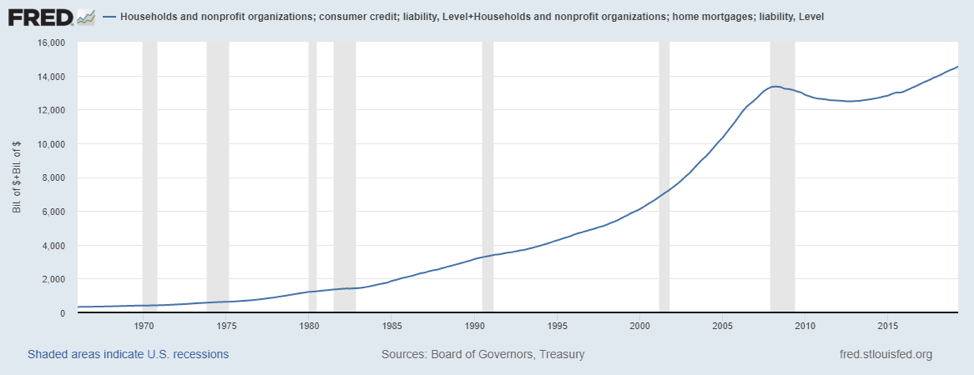

The data from the St. Louis Fed for the total debt owed by households and nonprofit organizations since 1966 paints a picture that can hardly be offered as a portrait of domestic thrift.

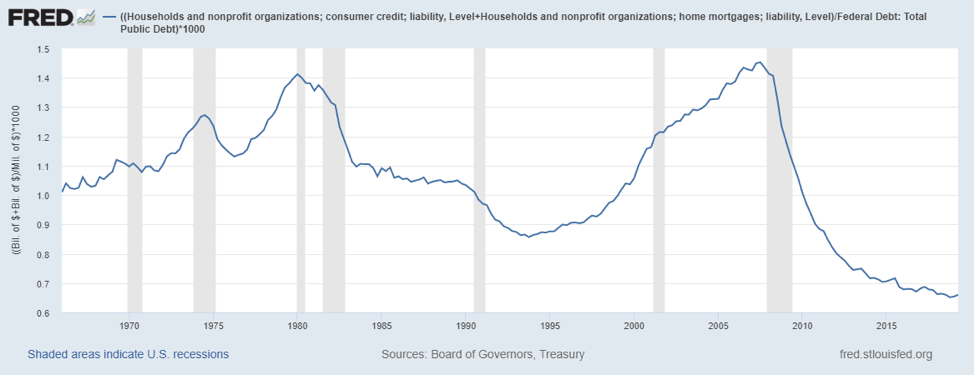

But, when their borrowings are compared to the accumulation of debt by the U.S. government, American consumers at least seem to have been aware of the idea of limits. Since 1966 the ratio of household to federal IOUs has been as high as 1.45 to 1 as low as .67 to 1 – where the ratio is now according to the most recent data from FRED.

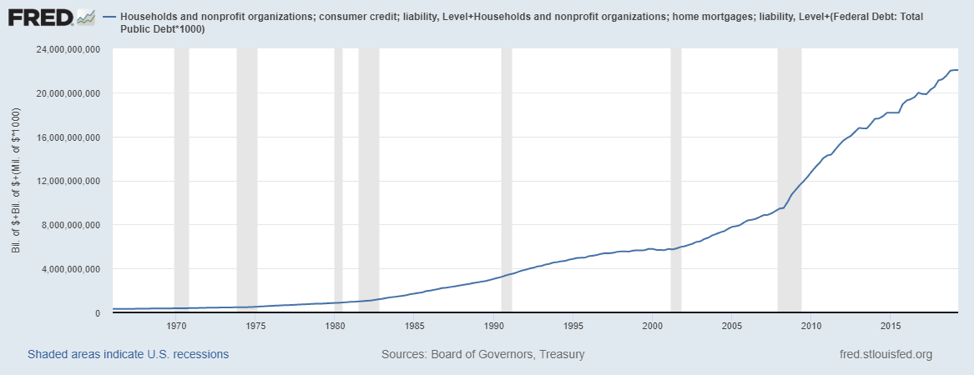

The current “low” ratio is largely a result of the extraordinary acceleration in federal borrowing. When household and federal debt are combined, the picture is one of constant increase.

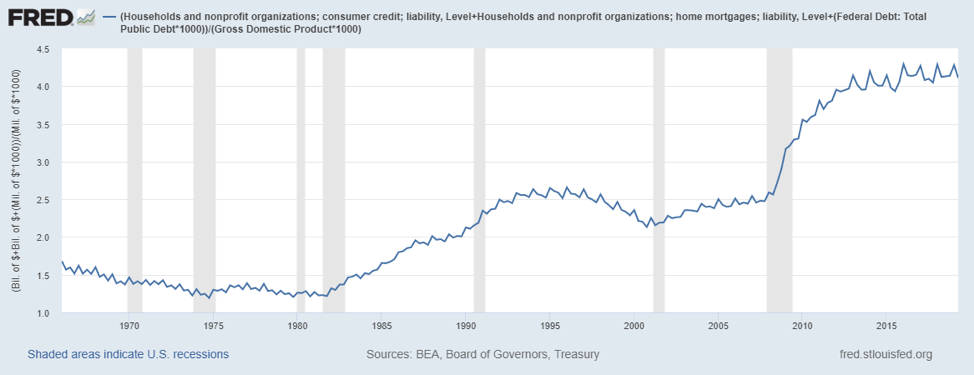

The good news, if any, is that the ratio of total household and federal debt to GDP has stabilized. The country, measured as a whole, is keeping its overall debt leverage steady.

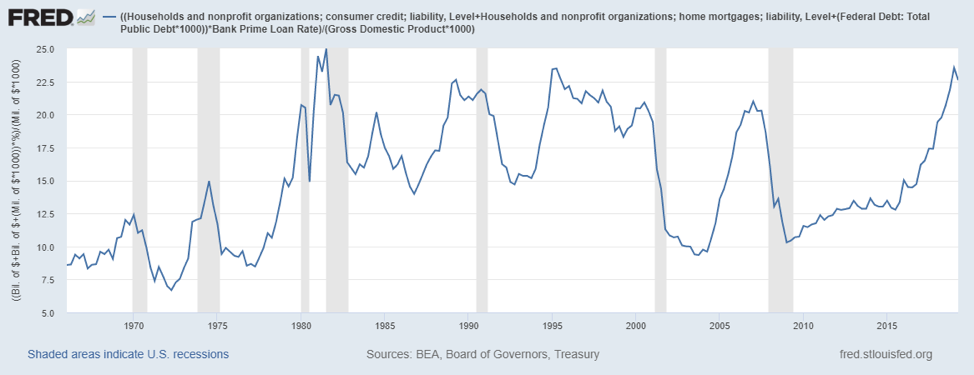

The bad news is that the ratio of the cost of carry for total household and federal debt to GDP is, once again, at an historical extreme. Whenever the cost of carry/GDP ratio has stayed above 20-to-1 for more than a single quarter, a U.S. recession has followed within a year or so. The one exception was the second half of the 1990s; but that period was the exception to almost every rule.

Stefan Jovanovich manages the portfolio for The NJT Company, Inc., a family office based in Nevada.

Read more articles by Stefan Jovanovich