Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

As two recent commentaries demonstrate, in their zeal to promote their agendas, asset managers are claiming that the humble 60/40 portfolio is doomed to the dustbin. But their analysis is flawed. The 60/40 will outlive us all.

Let’s start with a recent Yahoo Finance article titled 60% stocks and 40% bonds...not so fast, which caught my attention. The theme? “The simplest investing idea in the world may have died…60% stocks and 40% bonds...” Then, for drama, the editor included a photograph of a mock 60/40 graveyard with “RIP” on the tombstone.

He continued: “The traditional 60/40 mix, which has returned about 6% a year since 1970…might not be enough to generate the returns that investors have come to expect.”

Well, that explains it.

Except he is wrong.

The traditional 60/40 mix (60% U.S. stocks, 40% U.S. bonds) has not returned 6% a year since 1970. It returned around 9.3% yearly from 1970 through 2018. If it seems he didn’t miss it by much, an investment that returned 9.3% yearly would return 350% more cumulatively than an investment that returned 6% during this 49-year period.

However, even if he knew 60/40 returned 9.3% (he didn’t realize that the source he cited was after inflation), he would have written the same story. He felt so comfortable piling on the humble balanced portfolio that, no matter what the returns, he would have found an agreeable audience – or one oblivious to returns and fact checking.

Take Bank of America, which published a recent note called The End of 60/40. Authors Jared Woodard and Derek Harris, its global research portfolio strategists, wrote ominously,

The core premise of every 60/40 portfolio is that bonds can hedge against risks to growth and equities can hedge against inflation; their returns are negatively correlated…But this assumption was only true over the past two decades and was mostly false over the prior 65 years. The big risk is that the correlation could flip, and now the longest period of negative correlation in history is coming to an end as policy makers jolt markets with attempts to boost growth.

Here is how they illustrated it.

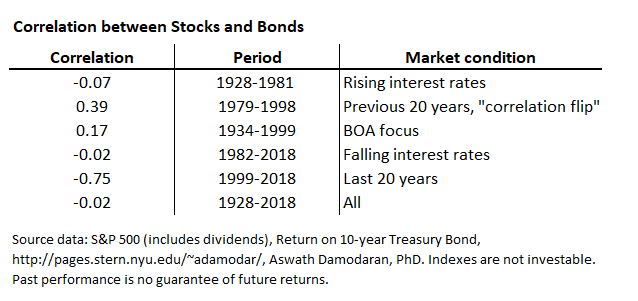

Unfortunately, the math does not add up here either, though they are correct that correlations were negative (-.75%) between stocks and bonds in the last 20 years. As shown below, during six comparative periods the correlation was only .17 for the BOA 65-year focus period (1934-1999) and was negative during rising and falling interest rate environments.

Correlation is a linear measure of two or more variables – in this case returns of stocks and bonds. A perfect negative correlation would result if stocks were up 10% and bonds were down 10%. This would be a great hedge but a lousy investment; you would never make any money.

High correlation is between roughly .50 and 1.00. Moderate correlation is between .30 and .49. Low correlation is .29 or less. Generally, the lower the correlation between assets, the greater the diversification value for the investor.

BOA wrote that a positive correlation of any value (even as low as .17), negates the hedge value of bonds to stocks. BOA cited low to moderate correlation that may happen between stocks and bonds for an unspecified time in the future, and it used non-representative research (S&P 500 and 30-year Treasurys) to build its case.

In addition to mis-characterizing correlation, no retail investor and few mutual funds buy 30-year Treasurys, yet this is what BOA paired with stocks to arrive at its thesis. There are 689 Allocation 50-70% funds, the category under which balanced funds go, in the Morningstar database. The average maturity of the bonds is 7.40 years – not 30 years.

Using 30-year Treasurys may have forced correlation measures up (since the higher return would have magnified bond returns) and better defended its turf. Additionally, BOA illustrated two-year rolling returns (see in graph above), which naturally show spikes that can occur – and remind us that 60/40 does not work every year. However, nothing in those short spikes indicates a trend or long-term correlation.

Here’s the rub. Even if it happened; even if the “correlation could flip,” would that be so bad? The correlation between stocks and bonds was negative for the last 20 years (1999-2018). The result? A 5.8% annualized return for a 60/40 portfolio. How about the dreaded correlation flip? For the preceding 20-year period (1979-1998), the correlation between stocks and bonds “flipped” to .39. This rising correlation scenario was the “end of 60/40” as we know it per BOA. What were the returns? 14.8% annualized (see below). Maybe a little correlation is not so bad?

There was no persistent long-term period where correlations were damagingly positive. When correlations were low to moderate, they were beneficial, as we see from 1979-1998.

Is it wrong to say, “The future of asset allocation may look radically different from the recent past, and it is time to start planning for what comes after the end of 60/40?”

Rising correlation is not the only faulty argument directed against balanced investing. Supposed narrowing returns are predicted as well by some. Here, the durability of 60/40 argument offers more than a statistics lesson.

See how the traditional balanced model compared against stocks for the entire period since the first S&P 500 index fund was launched in August of 1976.

The balanced portfolio returned 91% of the stock market with 47% of the risk, never had a negative five or 10-year return, or a single year with a double-digit loss. I cannot think of any investor who would not prefer those results to being 100% exposed to the stock market.

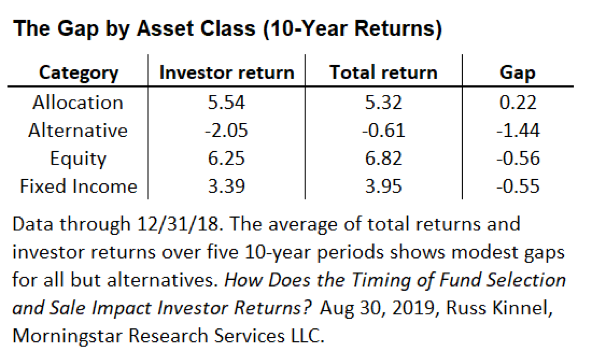

There is another reason why balanced investing will live longer than its enemies. Morningstar calls it “Mind the Gap” – the gap between investor and category return. It used to call it the IR-TR gap – investor-return, total-return gap, where much like Dalbar, Inc., it compares investor returns with the returns of the investment itself. Allocation and balanced funds tend to have higher investor returns than other categories. (see below) From the report:

“Balanced funds continue to have a positive gap, meaning investors enjoyed better returns than the average fund’s returns.” In other words…“These findings suggest that ‘boring’ funds work well because they aren’t as likely to inspire fear or greed. Also, timing simply has less impact on investor returns when a fund has lower standard deviation.”

Why is balanced such a subject of derision, or at least dismissal? My guess is that advisors and the media who follow them want to appear new, improved and innovative.

That’s cynical enough, but the reality is even worse. Despite claims that past performance does not predict future returns and you can’t time the market, asset managers – like Bank of America – are hopeful that you don’t believe that, and that they know something that you don’t. If you do, well here’s the latest better-than-best fund. It certainly can’t be 60/40 can it? It must be something (anything) new. Product creation always outpaces demand in a mature bull market.

But the industry is running out of ideas.

Am I being sentimental? No. The problem I have with “let’s just throw everything out and start over” is that we also throw away 90 years (1929 was the year Walter Morgan created the balanced fund) of good data and history.

Does Yahoo Finance and BOA seriously believe 60/40 hasn’t been tested? From 1929, the 60/40 model has survived well through four major wars, 14 recessions, 11 bear markets, and 113 rolling interest rate spikes (100+ basis points moves within 12 months, based on Moody’s Seasoned Aaa Corporate Bond Yield). What track record does your balanced replacement boast? To paraphrase Nick Murray, past performance does not guarantee future returns, but it is the best guide we have.

If you are building 60/40 weighted models for your clients, keep building. There is measurably more math, science, and history behind what you are doing than what your critics are saying. The goal is to design and build portfolios that your clients cannot outlive.

Balanced investing is the golden ratio of our industry. It has lived 90 years. It will outlive us all.

Andy Martin is co-founder and president of 7Twelve Advisors, LLC, researcher, and author of Dollarlogic: A Six-Day Plan to Achieving Higher Investment Returns by Conquering Risk, Arthur B. Laffer (foreword)

Read more articles by Andy Martin