Is the lack of a size premium due to the performance of small-growth stocks in general? Or is it due to penny stocks, IPOs, stocks in financial distress and lottery-like small-growth stocks (those with poor profitability and high investment)? Several recent studies answer those questions.

Let’s begin by looking at the data that shows the disappearance of the size premium, with a focus on small-growth stocks. Then I will discuss three research studies that collectively show why the size premium should not be written off by advisors.

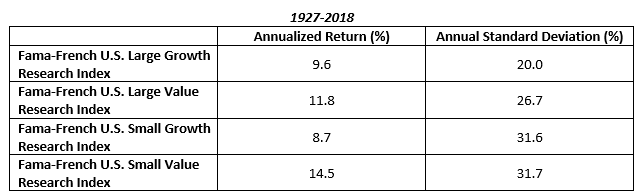

A major anomaly for the capital asset pricing model (CAPM) and the competing asset pricing models (such as the Fama-French three-, four- and five-factor models as well as the Q-factor model) is the performance of small-growth stocks. As you can see in the table below, using data from Ken French’s data library, small-growth stocks have had by far the worst performance among the four asset sub-classes, despite experiencing far greater volatility than large-growth stocks. And small-growth returns were well below those of small-value stocks, while experiencing virtually the same volatility. The rest of the data shows returns positively correlated with risk (large value has provided higher returns than large growth and small value higher returns than small growth).

The performance of small-growth stocks has been so poor that over the 50-year period ending 2018, they underperformed even long-term Treasury bonds (6.5% versus 7.9%) while experiencing more than twice the volatility (25.8% versus 12.0%). Over the same period, large-growth, large-value and small-value stocks returned 9.8%, 11.5% and 14.0%, respectively.

Such poor performance has also been found for penny stocks, stocks in bankruptcy and IPOs – all have experienced lower returns than we would expect (i.e., are anomalies for asset pricing models and market efficiency). Behavioralists explain these outcomes as the result of the “lottery effect,” or a preference for investments that exhibit positive skewness in returns. Positive skewness occurs when the values to the right of (greater than) the mean are fewer but farther from the mean than are values to the left. In other words, investors are willing to accept low average returns in exchange for the possibility of getting some extremely positive outcomes. You can think of it as investors searching for the next Google or Apple.

Using Morningstar’s data, we see that while small-growth stocks make up only about 2% of the total market capitalization, they are about one-third of the capitalization of small stocks. This creates a challenge (a hurdle to overcome) for the size premium, as the small-growth stocks “pollute” the size factor – if not for the performance of small-growth stocks, the size premium would be larger and more persistent.

The size effect was first documented by Rolf Banz in his 1981 paper, “The Relationship Between Return and Market Value of Common Stocks,” which was published in the Journal of Financial Economics. After the 1992 publication of Eugene Fama and Kenneth French’s paper, “The Cross-Section of Expected Stock Returns,” the size effect was incorporated into what became finance’s new workhorse asset-pricing model, the Fama-French three-factor model (adding value and size to the CAPM’s market beta).

Unfortunately, the size premium basically disappeared in the United States after the publication of Banz’s work. Using data from Ken French’s data library, from 1982 through 2018, the size premium in U.S. stocks was just 0.7% on an annual average basis and 0.3% on an annualized basis. The lack of a significant size premium over the past 37 years has led to much debate on the subject.

Controlling for quality

Cliff Asness, Andrea Frazzini, Ronen Israel, Tobias Moskowitz and Lasse Pedersen, authors of the January 2015 paper “Size Matters, If You Control Your Junk,” examined the problem of the disappearing size premium by controlling for the quality factor (QMJ, quality minus junk).

They note: “Stocks with very poor quality (i.e., ‘junk’) are typically very small, have low average returns, and are typically distressed and illiquid securities. These characteristics drive the strong negative relation between size and quality and the returns of these junk stocks chiefly explain the sporadic performance of the size premium and the challenges that have been hurled at it.”

The authors also found: “Small quality stocks outperform large quality stocks and small junk stocks outperform large junk stocks, but the standard size effect suffers from a size-quality composition effect.” In other words, controlling for quality restores the size premium.

The authors thus concluded that the challenges to the size premium “are dismantled when controlling for the quality, or the inverse ‘junk’, of a firm. A significant size premium emerges, which is stable through time, robust to the specification, more consistent across seasons and markets, not concentrated in microcaps, robust to non-price based measures of size, and not captured by an illiquidity premium. Controlling for quality/junk (the QMJ factor) also explains interactions between size and other return characteristics such as value and momentum.”

Further, Asness, Frazzini, Israel, Moskowitz and Pedersen found that “Controlling for junk produces a robust size premium that is present in all time periods, with no reliably detectable differences across time from July 1957 to December 2012, in all months of the year, across all industries, across nearly two dozen international equity markets, and across five different measures of size not based on market prices.”

They also noted: “When adding QMJ as a factor, not only is a very large difference in average returns between the smallest and largest size deciles observed, but, perhaps more interestingly, there is an almost perfect monotonic relationship between the size deciles and the alphas. As we move from small to big stocks, the alphas steadily decline and eventually become negative for the largest stocks.”

Another important finding from the study was that higher-quality stocks were more liquid, which has important implications for portfolio construction and implementation.

The authors found similar results when, instead of controlling for the quality factor, they controlled for the low-beta factor – high-beta stocks (those lottery tickets) have very poor historical returns. High-beta stocks tend to be those same low-quality stocks. In addition, they found that small stocks have negative exposure to two relatively newer factors, profitability (referred to as RMW, or robust minus weak) and investment (referred to as CMA, or conservative minus aggressive). High-profitability firms tend to outperform low-profitability ones, and low-investment firms tend to outperform high-investment ones.

Building on the findings of the above paper, Ron Alquist, Ronen Israel and Tobias Moskowitz, members of the research team at AQR Capital Management, also examined the impact of quality on the size effect in their May 2018 paper, “Fact, Fiction, and the Size Effect.” To summarize, they noted:

- The size effect diminished shortly after its discovery and publication.

- Because small-cap stocks typically have higher market betas than large-cap stocks, part of the size premium may simply be the equity market risk premium in disguise (CAPM alphas account for these beta differences).

- The size effect is dominated by a January seasonal effect; there is a large (more than 2% over the full period, though just 1% since 1976) and statistically significant (with a CAPM t-stat greater than 5 in the full period and greater than 2 since 1976) premium in January but nowhere else.

- It does not work for other asset classes outside of individual equities.

- It is not robust to other measures of size that do not include market capitalization (such as number of employees, sales and book value of equity).

- It has not been statistically significant outside the United States.

- It is found mostly in microcaps (the bottom 5% of all stocks); thus, it is more difficult to implement (making the control/minimization of trading costs critical).

However, they “save” the size effect by demonstrating that it is made much stronger (and implementation costs are reduced) when size is combined with the newer common factors of profitability, quality and defensive (low beta) – the return premium is greater for other factors in small stocks. Alquist, Israel and Moskowitz noted: “Controlling for quality resurrects the size effect after the 1980s and explains its time variation, restores a linear relationship between size and average returns that is no longer concentrated among the tiniest firms, revives the returns to size outside of January and simultaneously diminishes the returns to size in January – making it more uniform across months of the year, and uncovers a larger size effect in almost two dozen international equity markets, 30 where size has been notably weak. These results are robust to using non-market based size measures, making the size premium a much stronger and more reliable effect after controlling for quality.”

We now turn to another paper that addressed the disappearing premium.

Further evidence

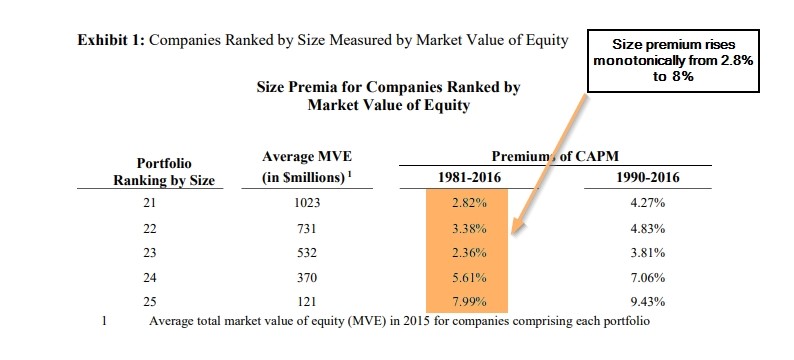

Roger Grabowski of Duff and Phelps contributed to the literature on the size factor with his November 2018 paper, “The Size Effect Continues to be Relevant When Estimating the Cost of Capital.” To study the size premium, he created quintile portfolios of the smallest companies. He excluded financial services companies because the regulated nature of banks and insurance companies causes their underlying characteristics to differ from those of nonregulated companies. He also excluded speculative start-ups, distressed (i.e., bankrupt) companies and other high-financial-risk companies. (These groups of stocks are often referred to as “lottery stocks.”) Grabowski wrote: “This methodology was chosen to counter the criticism of the size effect by some that the size premium is a function of the high rates of return for speculative companies and distressed companies in the data set.” His database covered the period 1981 through 2016 (the post-Banz period).

As shown in the table below, he found that, when ranking by market cap, the size premium increased monotonically from 2.8% in the first quintile to 8.0% in the fifth. In addition to market cap, he also examined the results based on ranking by net income. He found the same monotonic increases – the premium increased from 1.7% (first quintile) to 6.6% (fifth quintile). When ranking by net assets, the premium also increased monotonically, from 2.2% (first quintile) to 6.4% (fifth quintile). Similar results (though not exactly monotonic increases) were found when ranking by EBITDA (earnings before interest, tax, depreciation and amortization) – the premium increased from 3.4% (first quintile) to 6.0% (fifth quintile).

When Grabowski examined the subperiod 1990 through 2016, he found very similar results across all size metrics, with premiums tending to increase as size decreased – and in the case of two of the four metrics, the increase in returns was monotonic across quintiles.

Grabowski also examined whether the size premium is a proxy for other risk characteristics. For example, he found that smaller companies tend to have higher leverage and lower operating margins, and much greater volatility of that margin. For example, when breaking the market into 25 portfolios by market cap, the volatility of operating margin for the smallest stocks was about five times that of the largest stocks. Those are clear indicators of increased business risk. He also found that business risk, as measured by the unlevered asset beta (i.e., greater asset beta indicates greater business risk), generally increases as size decreases. He found these relationships to be robust to the various size metrics he used.

Summarizing, Grabowski noted: “Small companies are believed to typically have greater expected rates of return compared to large companies because small companies are inherently riskier.” However, as the AQR team demonstrated, to get the best results, you have to “control for junk,” eliminating the lottery stocks from the eligible universe.

We have one more paper to review, a new study that tackles the issue of the size premium in a similar manner to that of the AQR team.

Further research

Stefano Ciliberti, Emmanuel Sérié, Guillaume Simon, Yves Lempérière, and Jean-Philippe Bouchaud (CSSLB hereafter), contribute to the literature with their study “The Size Premium in Equity Markets: Where Is the Risk?” which was published in the July 2019 issue of The Journal of Portfolio Management. The authors “argue that market capitalization is not an optimal indicator of an otherwise genuine size effect. Indeed, the dependence of a stock beta on market capitalization is nonmonotonic, which induces spurious biases in a (market neutral) portfolio construction. The resulting SMB portfolios have a strong short low-volatility exposure. To isolate and identify the contribution of the size factor, we propose instead the average daily volume (ADV) of transaction (in dollars) as an alternative indicator of size.” As an alternative to market cap, CSSLB offer a CMH, or cold (low ADV) minus hot (high ADV), factor. Following is a summary of their findings:

- Neutralizing for beta (controlling for the low volatility effect – the lowest volatility stocks outperform the highest volatility stocks), both the short leg (large ADVs) and the long leg (small ADVs) are profitable and statistically significant. There is a size effect using CMH.

- CMH portfolios do not exhibit skewness.

- Extremes in both directions are more common for small stocks. Even if large upside events are more likely than large downside events for small stocks, because extreme tail events may dominate the average utility of an investment, safety-first considerations might be enough to deter market participants from investing in these stocks. This scenario is consistent with a risk-based explanation.

The authors noted that, “SMB portfolios are anticorrelated with portfolios that invest in low-vol stocks and short high-volatility stocks. Because the low-vol effect is statistically significant, such a negative exposure must necessarily degrade the performance of SMB.” Summarizing their findings, they stated: “Our main conclusion is at odds with the idea that the size premium is a myth. On the contrary, we find that, when measured in terms of dollar turnover (ADV) rather than market capitalization and once β-neutralized and low-vol neutralized, the size effect is alive and well … with a long-term t-statistic of 5.1.” Their findings are consistent with those of the other papers we have reviewed – controlling for quality and low beta (as well as the new factor of investment), thereby eliminating the lottery stocks, improves performance and restores the size premium.

The size premium’s disappearance may be a function of this “black hole” rather than a problem that impacts the entire asset class – if you screened out the black hole stocks, there would be a size premium that could be captured. Said another way, it’s the higher-quality small-cap stocks that explain the size premium. The other conclusion is to be sure to avoid those junky lottery stocks.

Implementation: Does size effect survive transaction costs?

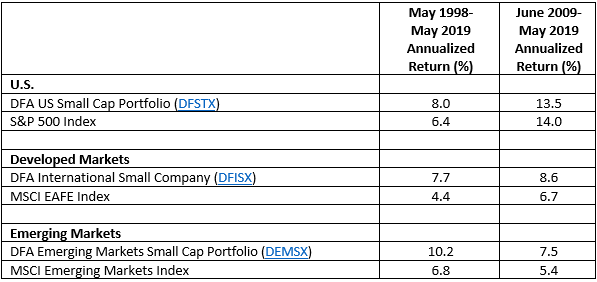

Based on research showing evidence of the small-growth anomaly, Dimensional has long used screens in its fund construction rules to eliminate lottery stocks (that is, penny stocks, IPOs, stocks in bankruptcy and small growth stocks with high investment and low profitability). Thus, by reviewing the results of the firm’s small-cap funds, we can determine if there has still been a small-cap premium that investors could have captured, not only in the United States but also in developing and emerging markets.

So that we can use all live funds, we will examine the more than 21-year period from May 1998 through June 2019. We will also examine the last 10 full years of the period (July 2009 through June 2019). (Full disclosure: My firm, Buckingham Strategic Wealth, recommends Dimensional funds in constructing client portfolios.)

For the more than 21-year period from May 1998 through May 2019, in each case there was a realized size (small) premium, ranging from 1.6% to as much as 3.3%. Over the more recent 10-year period ending May 2019, while there was a small underperformance (-0.5%) in the U.S., there was a 1.9% premium in developed-international small stocks and a 2.1% premium in emerging-market small stocks. These results are over the period where supposedly the size premium had disappeared. These results are net of not only expense ratios but all implementation costs, while index returns do not include any costs that would be incurred by live funds. Long live the size premium (controlling for junk)!

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 130 independent registered investment advisors throughout the country.

More Fixed Income Topics >