Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

It isn’t just how much the Fed cuts rates that matters; it is how soon they do it.

You don’t have to go far to hear calls for the Federal Reserve to not cut rates because they need to, “save ammunition” for when things are really bad. This imagines that the rate cut itself is the countervailing force against economic weakness.

But it doesn’t work that way.

Outside of a questionable psychological effect, the change in rate isn’t important, it is the level of the rate and for how long it persists. In fact, the Fed’s stimulative effect is more potent the sooner it is used, because lowering interest rates sooner will cost borrowers less than lowering them later.

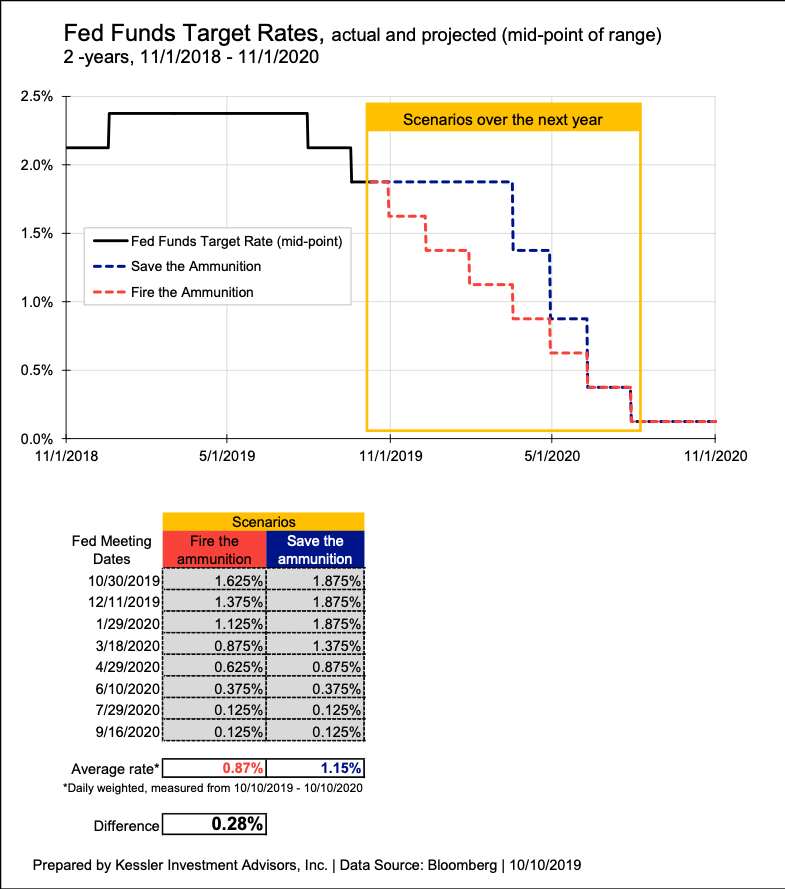

In order to illustrate this, consider two scenarios. In the first scenario, “fire the ammunition,” the Fed cuts 0.25% at each of the next seven meetings to get down to the prior Fed low – a range of 0-0.25%. In the second scenario, “save the ammunition,” the Fed doesn’t cut rates again until March of next year and subsequently lowers 50 basis points three times, then 25 basis points once.

In both scenarios, the Fed has lowered to 0.125% by July of next year. These scenarios shouldn’t be construed as predictions, but rather were arranged to illustrate the concept. See the chart below for a graphical representation. For simplicity, I considered the Fed Funds target rate to be the mid-point of the target range.

If you compare the average interest rate over the next year between the two, it doesn’t take much imagination to guess that the, “fire the ammunition” scenario costs a borrower less than the, “save the ammunition” scenario. And it isn’t a trivial amount. It would cost 0.28% less on average for the whole year.

And so, lowering earlier could generate more than a full rate cut worth of stimulus. The stimulating effect of rate cuts is not just how much the Fed cuts, but also how soon they do them. There are reasons left to be cautious in cutting rates, but saving ammunition isn’t one of them.

Eric Hickman is president of Kessler Investment Advisors, Inc., an advisory firm located in Denver, Colorado specializing in U.S. Treasury bonds.