Reverse mortgages have been receiving considerable attention in recent years as a retirement planning tool, with particular focus on the line of credit (LOC) feature. Retirees may be able to use a LOC to provide additional funds for retirement or in more specialized ways such as supplementing retirement savings portfolios during stock market downturns. Much of the research on such uses, including my own, has involved building full financial planning models that incorporate LOCs.

However, it is useful to narrow the focus to the performance of LOCs, as one would for any financial investment. That is the approach I will take in this article to provide an additional perspective for analyzing reverse mortgages.

The example

This article is based on an example of a 65-year-old individual owning a $350,000 home and utilizing a LOC, and the loan parameters are generated using the calculator provided by the National Reverse Mortgage Lenders Association (NRMLA). Under HUD rules, this individual can obtain a reverse mortgage LOC with a gross amount of $183,050. The up-front costs for setting up the LOC – loan origination, mortgage insurance, closing costs – are estimated to be $15,326 and, assuming those are borrowed as part of the reverse mortgage, the net amount available as a LOC is $167,724. This borrowing source will be accessible as-needed, and repayment will not be required until the borrower permanently leaves his or her home. Also, the loan is nonrecourse, and the borrower’s repayment obligation is capped at 95% of the appraised value of the home – no worries about deficiency payments as with a conventional mortgage.

The interest rate for the LOC loan is a variable rate based on 1-month LIBOR plus add-ons for loan origination and mortgage insurance. The initial loan rate is 4.64% based on the NRMLA calculator, although lenders do have some flexibility in setting loan rates and front-end charges. A unique reverse mortgage feature is that the LOC does not remain fixed at the initial amount, but, instead, any unused LOC grows at the variable loan rate.

My analysis is pre-tax, and LOC borrowings are, indeed, tax free. There may be some deductibility of loan interest at the time of repayment, but the tax rules on this are not completely settled.

Measuring LOC performance

We now turn to the task of determining how best to assess the performance of the LOC as a financial instrument. The basic structure involves periodically borrowing funds as withdrawals from the LOC and then repaying the loan when the reverse mortgage is closed out. In the most straightforward cases, the repayment is simply the loan balance, i.e. the accumulation of the withdrawals at the variable interest rate charged for the reverse mortgage loan. But there are a couple of additional considerations that may also affect the performance measurement:

- If the up-front costs of setting up the reverse mortgage are borrowed as part of the reverse mortgage, they will also accumulate interest charges and be included in the total loan balance.

- If, at the time of loan repayment, the reverse mortgage loan balance exceeds 95% (i.e., if the value of the home declines over the loan period, or if the mortgage balance grows above this threshold) of the appraised home value, the nonrecourse character of the reverse mortgage limits the required repayment to this 95% value.

More generally the “repayment” can be thought of as the difference between: (1) the home value that would have been realized without a reverse mortgage and (2) the actual home value (if any) realized after reverse mortgage loan payoff.

The reverse mortgage cash flows can be depicted as a column on an Excel spreadsheet divided into monthly or annual cells with the borrowings entered where they occur and the repayment at the end. Initially, I thought that LOC performance could be measured similar to a loan interest rate by simply calculating the internal rate of return (IRR) on the column of cash flows – typically positive periodic withdrawal flows followed by a negative repayment. However, as I did examples with IRRs, it became clear that this measure was incomplete because it didn’t reflect the length of the loan. For example, if one borrows money at a very high interest rate, but only for a short period of time, the financial impact will be small. To measure the financial impact fully, it is better to not only use the IRR, but also the present value of the flows.

With any present value calculation, there is the question of what discount rate to use. In this case, it’s appropriate to use a risk-free interest rate since the reverse mortgage is a bond-like instrument and the borrower is required to abide by the contract terms. I found it most useful to state the dollar flows in real rather than nominal terms to reflect inflation-adjusted spending power. On this basis, the appropriate risk-free rate would be close to zero, reflecting current TIPS yields, thus providing a convenient rationale for calculating present values by simply summing the positive and negative real dollar flows.

Applying performance measures

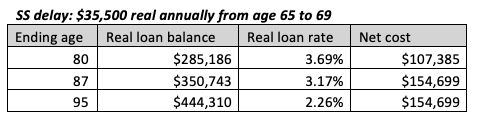

I provide two examples to demonstrate the use of performance measures – one based on borrowing from the LOC early in retirement and the other for late-in-life borrowing. For both of these examples, all dollar amounts are expressed as real 2019 dollars, and all interest rates are real interest rates after inflation is removed. The first case assumes that an individual retiring at 65 has decided to defer claiming Social Security to age 70, and will utilize annual borrowings from an LOC to provide bridge funds to support the first five years of retirement. The individual wishes to use the LOC to the limit and I estimate that withdrawing $35,500 annually, increasing with inflation, for five years will use up the LOC. The following chart shows performance based on alternative time horizons for when the reverse mortgage ends and the loan is repaid.

The real loan rates (IRRs) decrease as the ending age increases. This occurs because the impact of the assumed $15,326 of up-front costs is being is being spread over a longer time horizon. For ending ages 87 and 95, the LOC loan balances have grown to exceed the 95% of the home value repayment cap of $332,500, so having repayment limited by the cap holds down the real loan rates.

The final column shows that there is a substantial cost associated with the strategy – at least a present value of $100,000. (The reason the values for age 87 and 95 are the same is because in both cases the repayment is capped at a real $332,500 and, although the durations are different, the real discount rate is zero.) What’s happening here is that the real loan rate is between 2.26% and 3.69%, and the assumption is that real interest rate for bond investing reflects the current TIPS rate of close to zero. So we have a case akin to borrowing money at a higher real interest rate than one can earn on bond-like investments. In terms of pure economics, it would make more financial sense to use retirement savings for the bridge funding than borrow via a LOC.

The calculation of an IRR real loan rate implicitly assumes that the retiree in the example places as much value on leaving a bequest as on retirement consumption. There are, indeed, individuals and couples who place a very high priority on leaving a bequest. But at the other extreme there are those for whom leaving a bequest doesn’t matter at all. For such individuals, one could change the net-cost calculations to completely zero out the repayment; these net costs would then become benefits equal to the real value of funds withdrawn from the LOC – basically free money. Of course there are also in-between cases where clients discount bequests somewhat compared to their own consumption, and it’s not easy to determine an exact trade-off for such clients.

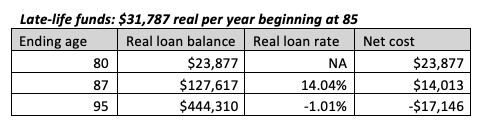

The second example is similar to using a deferred-income annuity (DIA) for longevity insurance (or a QLAC version thereof), but without the longevity protection. The plan is to take level real amounts ($31,787) from the LOC beginning at 85, since this amount is the estimated level real withdrawal that would zero out the LOC at age 95. Cases ending at 80 or 87 would not zero out the unused LOC.

For the age-80 case, there are no LOC withdrawals, so there is simply a repayment of the $23,877 real loan balance from borrowing $15,326 of up-front costs to set up the reverse mortgage. For the age-87 case there is a net cost of about $14,000, but for the age-95 case there is a net benefit of about $17,000 because of the $332,500 cap, which has a bigger impact by time horizon. The age-95 case is a rare example where the reverse mortgage by itself actually “makes money” for the borrower, even assuming that leaving a bequest is highly valued. For all three ages, the net costs are much lower than those for the previous Social Security-delay example, because the late-in-life loans have a much shorter time horizon from borrowing to repayment.

The real loan rates for this example highlight the shortcomings of focusing only on this measure. For the age-80 case, there is no IRR because there is only a repayment – no other cash flows. The age-87 case shows a high real loan rate because the borrowed cash flows are very short term (from age-85 start to age-87 repayment), so the borrowing of front-end setup costs has a disproportionate impact. The negative IRR for the age-95 case reflects there being a net benefit rather than a cost.

Coordination with investment portfolio

I haven’t provided an example for this category of reverse mortgage use, but this strategy uses reverse mortgage LOC withdrawals to support retirement spending when the investment portfolio performs poorly. For example, one such strategy involves taking withdrawals from the regular investment portfolio, except in years when the stock market produces a negative return, in which case withdrawals are taken from a reverse mortgage LOC. There’s been research on variations of this approach, which have clearly shown benefits in terms of retirement outcomes. However, I am uneasy, because such strategies, viewed retrospectively, produce net costs rather than benefits in a pure financial sense. To make such strategies work in terms of the economics, it’s necessary to discount the value of bequests and/or assume a higher discount rate for present value calculations than I advocate using.

Other considerations

There may also be non-economic reasons for using a reverse mortgage LOC. For example, a borrower may feel more relaxed about volatility in their investment portfolio if they have an unused LOC in place and growing at an attractive rate. A client might also feel wealthier and more comfortable early in retirement if they are using reverse mortgage borrowing for extra spending in those years rather than taking a substantial bite out of their retirement savings. Such considerations get into behavioral biases rather than pure economics. Advisors need to decide between accommodating such biases versus attempting to coach clients to see things differently.

There’s more to reverse mortgage advice than just presenting numbers.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

For this article he received valuable insights from Wade Pfau and Shelley Giordano, but he takes responsibility for the analysis and views expressed here. Both these individuals have authored books on reverse mortgages, which he highly recommends, and notes that the second editions of both are updated to reflect the latest changes in applicable federal rules. Links to those books are available on this page.

More Active Management Topics >