Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Critics of the federal deficit should recognize the imperfect nature of the debt-to-GDP ratio. By a more reasonable measure, our fiscal indebtedness is not high by historical standards.

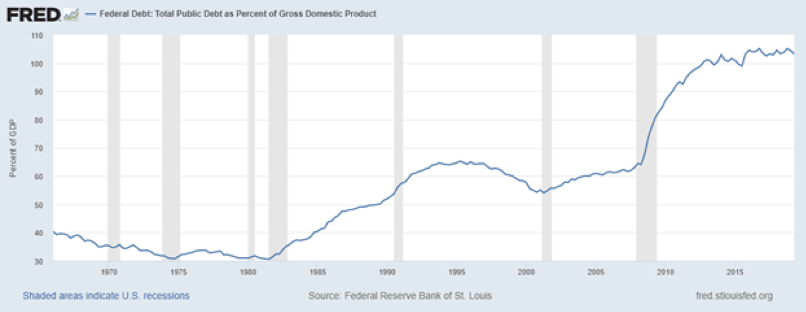

The measure of the inherent risk of the U.S. federal government's debt most commonly used is the ratio to gross domestic product. It is certainly the one that provokes the greatest concern from financial commentators and scholars. As the data from the St. Louis Fed illustrates, we are living in a country whose debt-to-GDP ratio has been increasing rapidly for four straight decades. From a low of .31-to-1 in 1974 and the early 1980s, the debt-to-GDP has risen to 1.03-to-1.

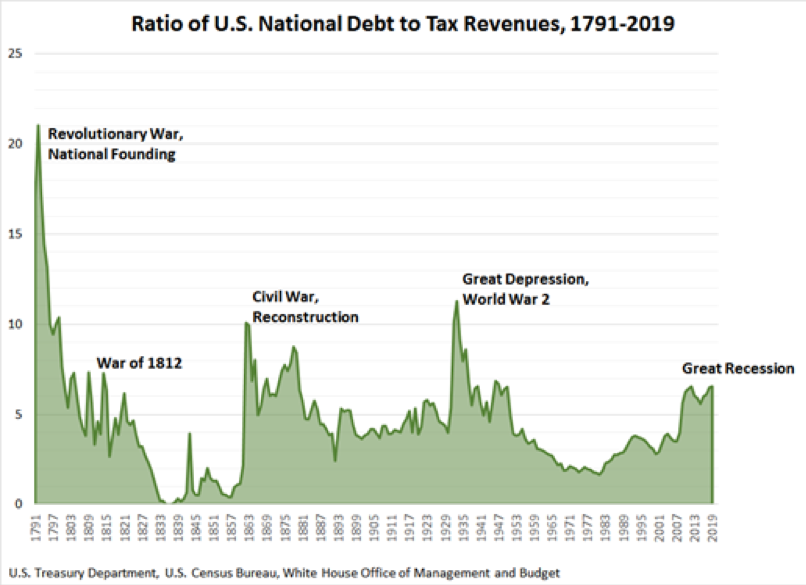

If the U.S. were a private corporation, the debt-to-GDP ratio would be expressed as the ratio of total debt to annual revenues. But that is not a commonly-used yardstick in analyzing the creditworthiness of a for-profit company. Instead, analysts use the ratio of debt to cash flow and other measures that calculate how much money a company collects and keeps, after taxes. If this kind of yardstick were used to evaluate the federal government's credit rating, the measure would be the ratio of national debt to federal tax revenues. Craig Eyermann at The Independent Institute recently produced a picture of that relationship for the entire history of the U.S., using the historical data from the census, Treasury and OMB.

Since Congress began authorizing the Treasury to sell IOUs (debt), the ratio of national debt to annual tax revenues has averaged 5-to-1. When the U.S. began borrowing money in 1791, the country's debt-to-taxes ratio was over 20-to-1. It took a third of a century – until 1820 – for that ratio to decline to what would become the historical average. Whether President Monroe or any chief executive is to be given credit for the country's balance sheet and income statement, there is no question that the voters approved of what Monroe had done in his first term. When he ran for re-election, he not only won every state – as Washington had – he would have won every electoral vote but for William Plumer of New Hampshire, who, contrary to the voters’ instructions, chose John Quincy Adams. Monroe and Adams and Jackson combined to produce the only period in American history in which the federal government entirely paid down its debts.

Thanks to the revival of trade after the panic of 1819, the first sustained real estate bubble in the country's history and the absence of any foreign wars, federal revenues from tariffs on imports and sales of federal landholdings boomed enough not only to pay off all outstanding Treasury IOUs but also to create a surplus large enough for "distribution" to become the campaign issue for the 1836 presidential election.

That was and will be, until the country defaults outright, the one and only time that the U.S. did not owe somebody somewhere the promise to pay them dollars. Thanks to the panic of 1837 and the Mexican war, Congress quickly went back to spending money it had not collected. After the 1856 election there was again the possibility of paying off all federal debts; but that disappeared with the world's first coordinated financial meltdown, the panic of 1857.

By the end of 1861, the debt-to-tax ratio had literally exploded, going from 1-to-1 to 10-to-1, a level reached again only in the Great Depression. Yet, despite with the enormous cost and devastation of the Civil War, the country was able to return within two decades to a ratio of between 4 and 5 to 1.

What is, in retrospect, even more remarkable is that this occurred even as the world economy had its second coordinated slump (the panic of 1873) and President Grant compelled both the Treasury and the U.S. banking system to operate on a permanent specie-redemption standard.

With the Great Depression and World War II, the debt-to-tax ratio erupted again; but, as with the Civil War, this measure of the country's financial risk showed remarkable resiliency. By President Eisenhower's first term, even with the added expenses of the Korean and Cold Wars, the ratio had declined to 4-to-1. The next three decades offered the only actual example of a country paying off its debt through inflation. The debt was not actually paid off; on the contrary, it continued to increase. But, thanks to the automatic escalations in the country's income and employment tax revenues from rising price levels, tax collections outpaced debt increases. By President Reagan's first term the debt-to-tax ratio was below 2-to-1, a level not seen since before the Civil War.

Since the early 1980s, whether one uses GDP or tax revenues as the denominator, the trend for the country's debt ratio has not been good news. Debt-to-GDP has increased 332%, and debt-to-taxes has increased 216%. But, as the data from two and a quarter centuries indicate, it is possible and even likely that the country can recover from its current SNAFU ("Situation Normal All Fouled Up") if the country avoids a foreign or domestic fighting war. If that tragedy can be avoided, the history of the debt-to-tax ratio presents a good argument that the present indebtedness of the federal government is worrisome but hardly unprecedented.

The historical record says that, even as Congress continues to borrow and spend on things other than war, the country's private incomes and the tax revenues those earnings produce can grow even more. When wars end, not only do the slaughter and waste stop but the policy horrors of price controls, conscription, and "excess" profits taxes also disappear, even as the country manages somehow to continue to mismanage its enormous debts.

Stefan Jovanovich manages the portfolio for The NJT Company, Inc., a family office.

More Tax Planning Topics >