Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

We're in a transition period from a bull to a bear market and from an economic expansion to a contraction (recession). Anyone who denies this is either ill-informed or a perma-bull. Or both.

Where do you stand at this important crossroad in market history? Are you a bull? Are you a bear? Where are you getting the information that supports your view? And how confident are you in that view?

These aren't idle questions. These are the questions every investor should be answering if they are serious about reaching financial security and independence with at least some help from their investments.

.

I'm going to lay out the bull and the bear case. You can decide which is more compelling. Personally, I'm a nervous bull who is sitting on 35% cash and watching every development in the market and the economy as this transition unfolds.

The bull case

-

The Trump put

The belief that President Trump won't allow the market to crash or the economy to tip over before he gets re-elected in 2020. He's got too much to lose, and he will stop at nothing to keep the financial markets healthy and growing.

“Trump was effective in helping the markets when it came to tax policy in 2017 and now in coming to an agreement with China,” said Peter Boockvar, chief investment officer at Bleakley Advisory Group. “Every time he talks about talks going well with China, that’s what the markets want to hear. If he says something good, the markets are going to rally.”

This argument has widespread appeal, but a closer look reveals some problems. Not only does Trump lack the tools to make this happen, his policies are putting even more pressure on the market and the economy. Tariffs are one example of this.

- The Fed put

The widespread belief that the Fed will not allow a recession or bear market to happen on Powell's watch. What tools are available to the Fed for this purpose? Cutting rates, printing money, and using that money to support market prices (indirectly – the Fed can't buy stocks like China and Japan can).

- The trade war put

The belief that President Trump, master negotiator that he is, will prevail over Xi in the worsening trade war. When that happens, the economy and stock market will rocket higher and money and jobs will come pouring into the U.S. from China. This scenario may not unfold. It could go the other way.

- The consumer spending put

The belief that robust employment has encouraged consumers to spend more and more as the 2020 election nears. There is evidence of an uptick in spending, so this argument is fair. The question is – will it last?

- The infrastructure spending put

This includes the belief that both houses of congress will pass a new, massive spending bill to rebuild America's crumbling infrastructure. It also includes the belief that corporations will embark on an aggressive capital spending campaign that will create jobs, boost wages, and keep the economy going.

- There is no alternative to stocks (TINA)

The stock market will keep going up because bonds are paying next to nothing and stocks at least pay a dividend.

“The market is making several assumptions,” says Blackstone Group strategist Byron Wien. “There will be some sort of a trade deal with China in the next six to nine months. Interest rates and inflation will remain low, and the stock market is attractive, with stocks yielding more than bonds.”

- Fear of missing out (FOMO)

Hard lessons were learned after the 19.9% market rout from September to December of 2018. Investors who bailed out mostly got burned twice – once when they sold near the bottom, and again when they waited too long to get back in, if they ever did. Those scars take a long time to heal, so this time around it seems more risky to miss out on further market gains than it is to sell too soon.

The bear case

- Punk corporate earnings

- Stretched equity and bond valuations

This one gets a little wonky, so I'll try to make it more user-friendly.

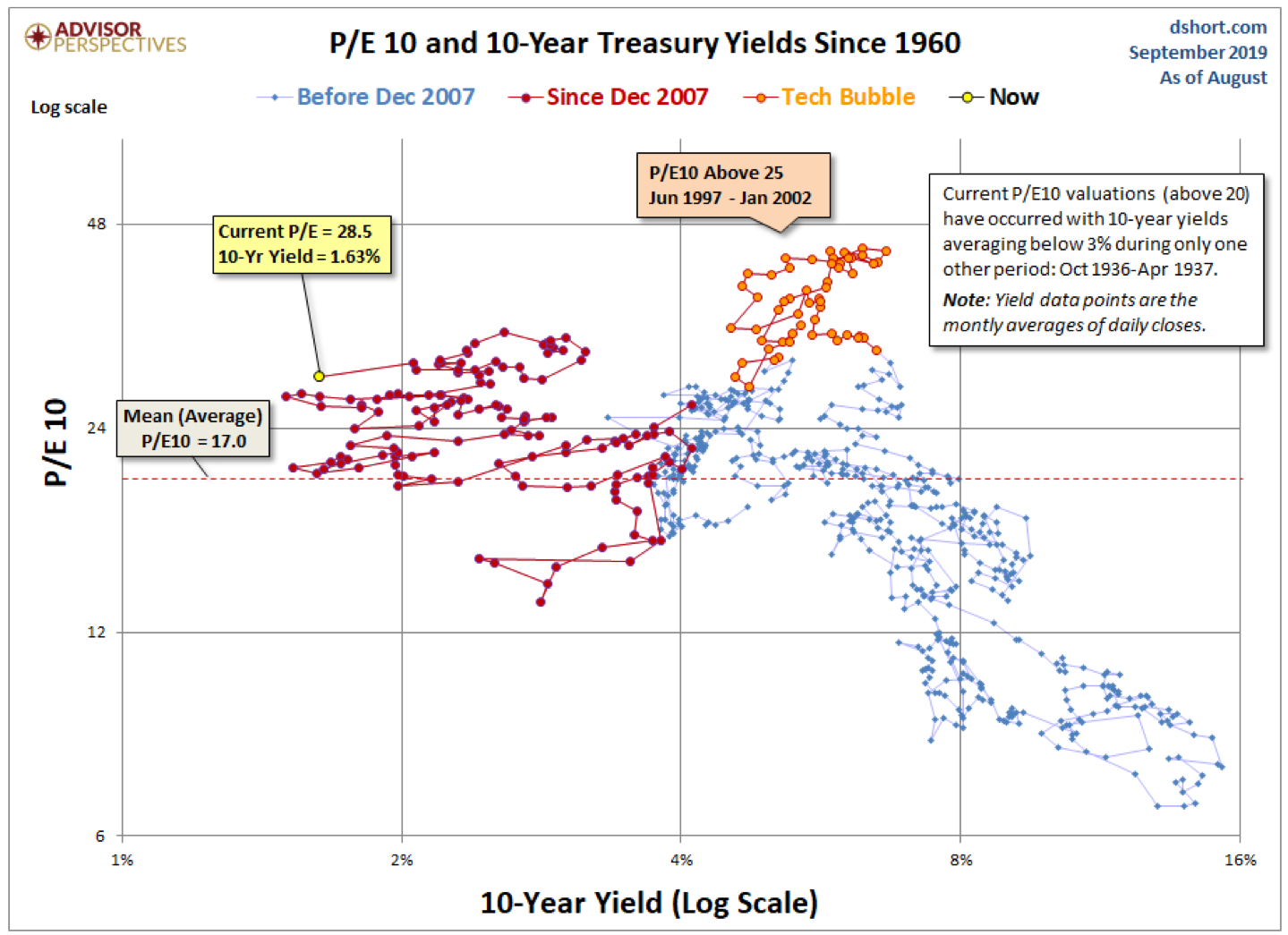

The chart below, from Jill Mislinski, shows the relationship between the yield on the 10---year Treasury bond and the P/E 10. The P/E 10 is a valuation measurement created by Pulitzer Prize winning economist Robert Shiller, a Yale finance professor.

What this calculation does is smooth the market P/E to remove year-over-year volatility by including earnings for the past 10 years. The result is a long-term view of how expensive the market is today, compared to its valuation over the past ten years.

In the months following the Great Financial Crisis, we have essentially been in uncharted territory. Never in history have we had 20+ P/E10 ratios with yields below 2.5%. The latest monthly average of daily closes on the 10-year yield is at 1.63%, which is close to its all-time monthly average low of 1.50% in July 2016.

- The global debt bubble

Here's how much the U.S. Government is in hock to creditors, both foreign and domestic:

$22,531,817,693,305.66

That's 22.5 trillion dollars. The good news is that interest payments on this debt are very affordable... for now. But does anyone think that rates will stay this low forever? There will be a day of reckoning as some point.

- Weakening market internals

I publish this table in my monthly letter to subscribers. It tracks the movement of key measures of market health. The number scale is 1-10, with 1 being the strongest reading for that indicator, and 10 being the weakest.

- Inverted Treasury yield curve

The Treasury yield curve has been inverted since April. 2019, and it's getting worse.

- August payrolls came in light

Forget the media spin and punditry hype. This was a bad number. The only thing that saved the day was government hiring of Census workers.

- Manufacturing is weakening

How can a car plant in Kentucky or a steel plant in Pennsylvania justify ramping up production when a tariff war is raging between U.S., China, Mexico, Canada, and Europe?

- AAII bears outnumber bulls by 16%

Many believe that this is a contrary indicator. The idea is that retail investors who fill out this survey are usually wrong about where the market is headed next. That may be the case today, but what if it's not?

- Investors are seeking shelter in low volatility stocks

The S&P 500 Low Volatility index has returned 12.5% over the six months ended Sept. 4, outperforming the S&P 500’s 6.3% return by more than six percentage points. That, observes the Leuthold Group’s Jim Paulsen, is one of the strongest six-month periods for low-vol stocks since 1989.

- Heightened geopolitical risks

Geopolitics usually don't have much influence on the global capital markets. But think about a shooting war with Iran, North Korea, Pakistan, Russia, or even – God forbid – China. What kind of damage could that do to the global economy, which depends on trade between these global players?

- A no-deal Brexit

U.K. Prime Minister Boris Johnson is doing his best to pull the U.K out of the European Union without a trade deal in place. One could say that he's trying to out-Trump Trump by demonizing the opposition and attempting to shut down Parliament. I don't see how this will end well.

- $17 trillion in negative-yielding global government debt

Aside from the inexplicable fact that investors have now parked $17 trillion in government paper that guarantees a negative return, the thing that concerns me is the mis-pricing of risk that goes with it. When rates are negative, it sets off a chain reaction of behavior that isn't based on normal financial theory.

Institutions who are mandated to hold a certain amount of A-rated sovereign debt will blindly obey that mandate, damn the consequences. Furthermore, think about the multi-billion dollar investment fund that sees the stock market as more dangerous than a guaranteed negative return because at least the sovereign paper will be repaid in full.

The smart money case

- Stay invested but reduce market exposure in predefined steps

- Go against the grain

European stocks have been hampered by the lack of a dynamic tech sector and a large weighting in banks (which have badly trailed their U.S. peers), energy (one of the global markets’ worst sectors), and economically sensitive stocks like autos.

Part of the bull case for European stocks is that yield-starved European investors will gravitate to equities, given that government bond yields are low or negative, with the German 10-year Bund at -0.6%.

And U.S. benchmark oil has outperformed the global benchmark this year, leading prices in recent weeks to the narrowest spread in more than a year. Analysts say the move isn’t about the trade war.

- Avoid high-risk markets like junk bonds, leveraged loans and unicorn IPOs

The floundering prospects for an initial public offering of the We Co., parent of WeWork, shouldn’t come as a surprise. The company is exhibit A for the ills of the unicorn market – private businesses with $1 billion-plus valuations – at a time when public-market investors are souring on several of them. Uber Technologies is down nearly 30% from its IPO price after hitting a new low this past week.

- Gravitate to lower-risk markets like muni bonds and CEFs, value stocks, and low-volatility stocks

- Nibble around the edges of clean energy stocks and ETFs

- Seek refuge in utility companies and ETFs, especially potable water

- Look for reasonably priced stocks and ETFs that invest in robotics, AI, and cyber security

- Turn off CNBC and other financial media outlets that traffic in fear and greed

- Sell any holding that you bought on the recommendation of someone else unless you understand what they do, how much money they're making, and where the money is coming from

Final thoughts

This article addressed the friction between bulls and bears. What makes this period in market history just a little different than other periods is the degree to which each camp is dug into their beliefs and their investment posture.

This friction is at least in part due to the political divide in the U.S. and elsewhere. Bulls appear to believe that the country, the economy and the stock market are on the right path and that better days are ahead. The political part of this is the belief that campaign promises of America first will bear fruit.

Specifically, millions of jobs coming back from China to the U.S., a revival of the beleaguered coal industry, massive spending to repair our crumbling infrastructure, corporate tax cuts that will spur capital spending and create millions of new high-paying jobs, tax cuts that will enable middle class consumers to open their wallets again, and the elimination of the horrendous government debt that has been racked up by George W. Bush and Barack Obama.

At least part of the optimism on display by the bulls is based on their belief that these campaign promises will come to pass. I don't have a problem with optimism. Optimism is good. But so is reality, history, and arithmetic.

Bears can sense that something isn't right with this rosy scenario. Maybe that's why every time the market gets close to, or makes a new high, the bears come out in force to spoil the bulls' party.

I attended a Tony Robbins seminar recently and what I heard was that all it takes to achieve great success and happiness in life was adopting a belief that whatever you can imagine will be manifested by sheer force of will. But is that really how life works? Not in the stock market. And not in the economy. These two realms only care about the numbers. Not the promises, or the predictions, or the positive energy that comes from a seminar.

The stock market is relentless in ferreting out extremes in valuation and shifting economic trends. That's why mean reversion is such a powerful force in finance. We're now at a place where valuations and stock market returns are at extreme levels. They can become even more extreme, but why would a rational investor bet their life savings on that prospect?

Erik Conley is former head of equity trading, Northern Trust Bank, Chicago. Teacher, trainer, mentor, market historian, and perpetual student of all things related to the stock market and excellence in investing.

More Tax Planning Topics >