Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The conventional approaches to limiting downside losses, such as put options, portfolio insurance or market timing, are either too costly or cumbersome to implement. We propose a “black swan” strategy that combines Treasury securities with equity call options in a barbell fashion.

We show that this strategy has effectively limited losses during periods of extreme market stress, while participating in a significant portion of upside during equity bull markets.

Avoiding losses

Ten years (and 300+% later) into the longest bull market ever, the memories (and lessons) of the 2007-2009 shock waves are slowly being relegated to the back recesses of investors’ memory banks. However, astute students of financial history recognize the movie we saw during the Great Financial Crisis was simply a remake of prior episodes, going all the way back to Dutch Tulip Bulbs of 1637. While history never repeats in the same way, a different version of another crisis is only a matter of time. An average investor may be excused for thinking the stock market trend lines of the last few years will continue uninterrupted. But advisors have a fiduciary duty to ensure client portfolios are appropriately prepared for the next market “adjustment.”

Several approaches are available for protecting portfolios from a 20% or worse bear market, such as moving a notch (or two) down on the risk scale, buying protective puts, using stop-loss orders or employing more advanced strategies such as constant proportion portfolio insurance (CPPI). Assuming the well-accepted investing maxim that short of getting lucky, market timing is practically impossible, every portfolio insurance/risk reduction strategy ends up suffering from some combination of the following problems:

- The financial cost – whether explicit or opportunity – of implementing the strategy; and

- The cost associated with continual monitoring of the strategy.

Some insurance strategies entail not only a financial cost but also periodic monitoring, reversal of positions, and investing in a new tranche every few weeks or months. Lowering the risk profile of a portfolio from what is appropriate based on the investor’s degree of risk aversion will certainly insulate a portfolio somewhat from the downturn. However, the opportunity cost of missing out on a large portion of the market upswing can be substantial. Investing in a low-risk portfolio due to investors’ fear of market downturns can delay retirement because of lower returns on the portfolio.

In the wise words of the investing legend, Peter Lynch: “Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in corrections themselves.”

Other popular portfolio insurance approaches, such as CPPI, work well in theory but require significant rebalancing, monitoring, frequent transactions and the unappealing requirement of selling as the market falls. In addition, as the portfolio floor is reached, the investor is entirely out of the market. There will be no upside appreciation if the market rebounds. Furthermore, at what point in time is a reallocation to equities implemented with a new set floor? This makes CPPI difficult to implement.

Prospect theory and decades of work in the area of behavioral finance clearly point to a need to pay special attention to the downside capture of any investment strategy. Absent an intentional focus on limiting downside capture, behavioral investor biases will inevitably lead to decisions during (and after) a bear market (or even a correction) that will be detrimental to the portfolio in the long term. The most recent bear market of 2007-2009, for example, left many portfolios, even ones that were appropriately diversified, down 20 to 30%.

Thus, investors in March, 2009 (at the start of what has turned out to be the longest bull market ever) were not only left with the hard mathematical reality of starting out from a much lower base than what existed in October, 2007, but also a large percentage uninvested after shifting to “safer” investments during the financial crisis. As investors stayed away from risk in 2009 and 2010, they missed out on the high returns typical of early recovery periods after a bear market (the S&P 500 was up 92% from March 9, 2009 to December 31, 2010).

Thus, the search for the holy grail continues that limits downside risk, allows participation during bull markets, and minimizes both implicit and explicit implementation costs. Striking a balance between these issues will not only spare the portfolio of the hard work required to recover from bear market lows but, more importantly, investors will be more likely to stick to the mutually agreed upon optimal strategy – especially through adverse conditions.

Alternative to classic portfolio insurance

In a recently published paper, we examined such an approach and argued for a barbell-type strategy where 90% of the portfolio is invested in Treasury instruments (or an investment-grade bond fund) and the other 10% is used to buy call option long-term equity appreciation securities (LEAPS) on the S&P 500 (“Leaping Black Swans,” Vol. 28, No. 1, February 2019, Journal of Investing, William Trainor, Indudeep Chhachhi, and Christopher Brown). The primary impetus for this strategy came from a desire to provide significant protection during black swan events such as the one experienced in 2008-2009. Thus, we named this a “black swan portfolio.” As detailed in the paper, the black swan portfolio is far superior to the protective put strategy based on Sharpe and Sortino ratios, omega, value-at-risk, and expected shortfall. The latter four statistics measure downside risk. While CPPI metrics are similar to the black swan strategy, CPPI is subject to both large gap risk (sudden large market moves causing the floor to be breached) and continual required adjustment in response to market movement. In contrast, the black swan portfolio, like other index-based strategies, has the set-it-and-forget-it element.

On November 6, 2018 Amplify ETFs launched SWAN, an ETF based, in large part, on the research referenced above. The SWAN ETF (like the S-Network BlackSwan Core Index that it tracks) invests 90% of the money in a range of Treasury maturities from two to 30 years with the intent of matching the duration of a 10-year T-Bond. The remaining 10% of the portfolio is invested in two separate tranches (December and June) of in-the-money, LEAP call options on S&P 500.

Historical evidence

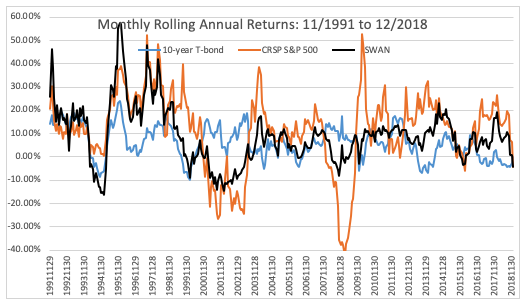

With the caveat that short-term performance may not be indicative of the future performance of a product, SWAN weathered the early volatility in the market as it was designed to do. In the seven weeks from November 6 to December 24 2018, SWAN was down 6.2% compared with a drop of 12.3% in S&P 500 over the same period. As the post-Christmas market sentiment shifted, SWAN also participated in the market rebound; as of August 16, 2019, SWAN was up 10.4% compared to 3.9% for the S&P 500 (since the Nov. 6, 2018 inception of SWAN). To attain a better idea of returns expected in the future, monthly data back to 1990 were calculated using the SWAN methodology. Figure 1 shows the monthly rolling one-year returns for the S&P 500, a constant 10-year Treasury, and the simulated SWAN portfolio.

A black swan portfolio can and will lose money at times. Theoretically, the worst possible return is a market decline of 5% or more where the option values approach zero combined with a large upward move in 10-year yields. This could and has occurred, such as the 12-month period ending Jan 31, 1995, when 10-year constant maturity T-bonds lost 6% coupled with a virtually flat market. During this one-year holding period, the synthetic SWAN lost 16%. (The worst historical annual return for a constant 10-year Treasury was -10.6%, in the year ending May 1959.) However, during significant market distress, such as 2000-2001 and 2007-2009, the synthetic SWAN maintained most of its value, as only 10% of it was exposed to the equity market.

A perfect example of the effectiveness of the black swan portfolio to reduce downside risk was 2008; the black swan portfolio declined 8.29% versus The S&P 500’s decline of 37.59%! The cost of this protection is mitigated due to the upside exposure attained from using leverage that options provide. On average, the black swan portfolio should participate in approximately 50-60% of market gains via the options plus the return from the Treasury securities. By avoiding large losses during market declines, the overall participation rate relative to investing 100% in the S&P is appealing.

Since 1991, the synthetic SWAN based on the ETF has an annualized return of 8.56% relative to the 10.01% of the S&P. A black swan portfolio will increasingly lag the market during sustained rallies. As an example, from January 2010 to December 2018, the S&P was up 11.70% annually, while the synthetic SWAN portfolio averaged 8.14%. These results have been confirmed using bootstrapped data to simulate 10,000 unique annual returns. Again, the idea is simple: If you can avoid a 40% loss, you do not need to earn 67% just to reacquire what is lost. The black swan strategy can help alleviate the need to have an extremely long-time horizon if an investor wants/needs exposure to the market.

Implementing a black swan strategy

Which clients and investors are best suited for a black swan-type strategy in their portfolios? As an advisor, what guidance should you provide to those investors with regard to the optimal allocation to a black swan strategy? Is incorporating a black swan strategy within a portfolio a long-term hold or a market-timing tool?

At its simplest, the black swan strategy takes advantage of the flight-to-safety phenomenon in the market that leads investors flocking to Treasury securities (and other high-quality bonds) during periods of stock market turbulence and uncertainty. This creates a number of planning opportunities that have historically remained elusive or have required more complex investment tools.

First and foremost, a black swan strategy is an ideal candidate for investors who are in the withdrawal phase of their portfolio (spending assets that have been accumulated over a lifetime) or in the last decade of the accumulation phase. Market crashes are the bane of an investor in or approaching retirement. There is either little or no time to make up losses, as an investor is forced to continually withdraw funds from a depleted portfolio. While much has been written (Campbell, Koedijk, & Kofman, 2002; Sandoval, 2012) on how traditionally negatively correlated assets tend to move together during periods of extreme market stress, Treasury securities often become more negatively correlated during such times (for example, the long-term Treasury bond index was up more than 20% in 2008). Thus, a black swan-type of investment provides stability to the portfolio and access to funds at the exact time when you don’t want to tap parts of your portfolio that have been decimated because of market declines.

A Black Swan portfolio’s ability to withstand severe market declines comes with mitigated sacrifice of the upside relative to traditional portfolio insurance methods.

While a black swan strategy’s natural appeal as a partial answer to mitigate large losses is obvious, it is no less attractive to counter investor behaviors in the face of overwhelming evidence supporting prospect theory, (Kahneman & Tversky’s 1979, Dichtl & Drobetz, 2011a,b, Chou, Chou, & Ko). The black swan-portion of the portfolio can be viewed, even in the accumulation phase, as a sidecar to investor’s equity holding and a way of providing some downside protection while still participating in the upside. Risk tolerance questionnaires notwithstanding, we know how bear markets will evaporate the high risk tolerances that may have been seen during bull markets. The black swan strategy makes it more likely an investor will stick to his/her investment strategy through the inevitable troughs of a market roller-coaster.

The black swan strategy as outlined here (and in The Journal of Investing) is not a market timing strategy that needs to be turned on or off based on one’s expectation of where the market may be headed. Instead, for many investors, this should be a permanent allocation in their portfolios, based on investor risk preferences. As investment professionals, we recognize the value of diversification as one of the major building blocks of any portfolio. However, we don’t have to limit diversification to multiple asset classes. We should also implement diversification of strategies, especially when the other strategy is an index-based, simple-to-understand (and execute) passive, low-expense, strategy that research has shown will likely provide significant downside protection with more than a palatable sacrifice of the upside. Black swan is that strategy.

Indudeep S. Chhachhi is a professor of finance and chair of the finance department at Western Kentucky University. William J. Trainor is a professor of finance at East Tennessee State University. Christopher L. Brown is a professor of finance at Western Kentucky University.

Bibliography

Campbell, Rachel, Kees Koedijk and Paul Kofman, Increased correlation in bear markets, Financial Analysts Journal, Vol. 58, No. 1 (Jan. - Feb., 2002), pp. 87-94

Chou, Pin-Huang, Robin Chou, Kuan-Cheng Ko, Prospect theory and the risk-return paradox, Review of Quantitative Finance and Accounting, Vol. 33, No. 3, pp 193-208.

Dichtl, H., Drobetz, W., 2011a. Portfolio insurance and prospect theory investors: Popularity

and optimal design of capital protected products. Journal of Banking and Finance 35, 1683-1697.

Dichtl, H., Drobetz, W., 2011b. Dollar-cost averaging and prospect theory investors: An explanation for a popular investment strategy. Journal of Behavioral Finance 12(1), 41-52.

Sandoval Jr., Leonida, Correlation of financial markets in times of crisis, Physica A: Statistical Mechanics and its Applications, Vol, 391, No1-2, pp 187-208.

Kahneman, D., Tversky, A., 1979. Prospect theory of decisions under risk, Econometrica 47, 263-291.

More Factor-Based Investing Topics >