Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Value investing is poised to dominate growth investing based on a historical comparison of valuation metrics. The gulf between the P/E ratios of value growth and growth stocks has never been this wide.

At the turn of the century, value investing was all the rage. From the peak of the dot.com bubble through 2006, its popularity was supported by academic research and such luminaries as Warren Buffett. Value investing indeed reigned supreme. Since then, however, its historic performance advantages vanished. After 13 years of lackluster performance, value investing seems like a relic of the past.

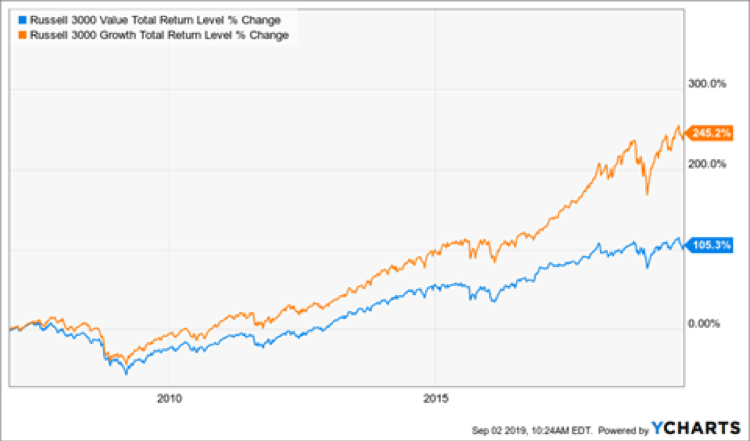

Since 2006, the relative outperformance of growth stocks over value stocks has been strong. In fact, growth has outperformed value by a whopping 140% on a cumulative basis when looking at the two broadest style benchmarks – as shown below. This is more than a 10% yearly advantage for growth stocks (or +7% compounded annually).

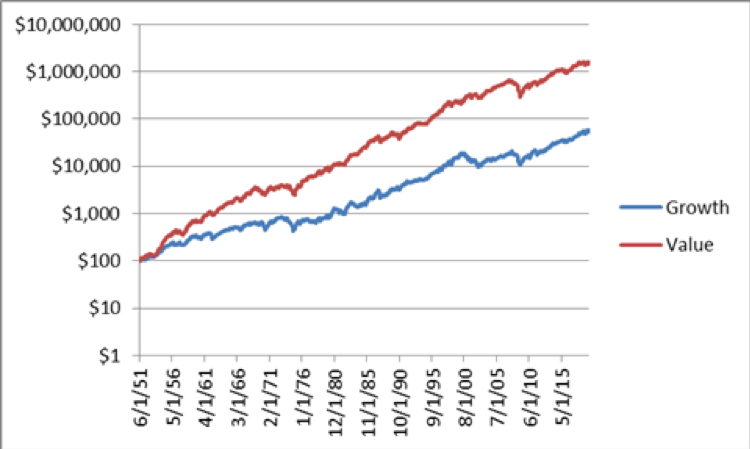

Taking a step back, value investing has historically dominated the broader universe – especially its pricier growth counterpart. The chart below shows the growth of $100 using Fama-French data where portfolios are based on companies that fall within earnings yield (earnings-to-price) ranges.

The value portfolio represents all stocks with the highest 30% of earnings yields (lowest P/E ratios). The growth portfolio represents all stocks with the lowest 30% of earnings yields (highest P/E ratios).

Value and growth performance (Growth of $100)

Another metric that is more closely associated with Fama-French research is the book-to-price ratio. In looking at book-to-price data, the results are quite similar. Book-to-price data also goes back to 1926 and therefore provides for an even more robust analysis on that basis.

The chart below is the ratio of value-to-growth (based on the two lines in the above chart).

Ratio of value to growth

Source: Fama French (Dartmouth website, “Portfolios_Formed_on_E-P”). Aviance Capital Partners.

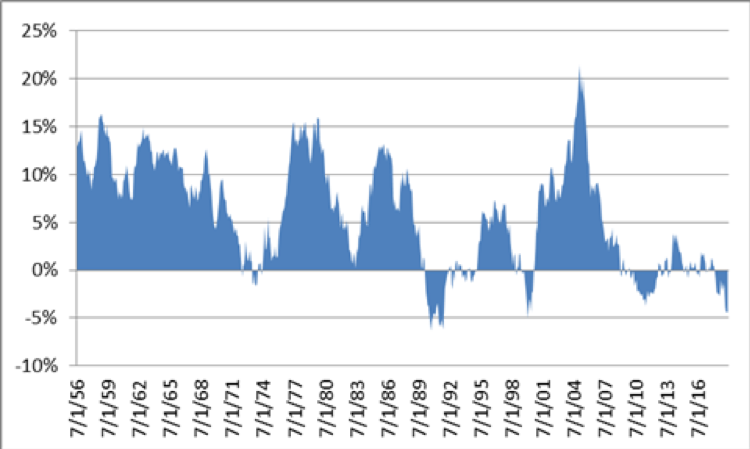

Value generally outperforms growth on a rolling five-year basis

(Value minus growth using five-year annual compounded rolling return)

Source: Fama French (Dartmouth website, “Portfolios_Formed_on_E-P”). Aviance Capital Partners.

Since 2006, value has clearly lagged. This is an unusually long period of underperformance for an approach that has historically been sound.

Is it time to give up on value investing? Has a new paradigm been reached that says fast growing businesses trading at high multiples are relatively better investments? Or, simply, has a shift in the markets made value stocks poor investments?

A look at the fundamentals

The relative valuation (on metrics such as the price-to-earnings ratio or the price-to-book ratio) between growth stocks and value stocks has changed quite a bit over the recent years. Specifically:

- Growth stocks now look expensive relative to history;

- Value stocks look reasonably priced relative to history; and

- Combined, the gap between growth stocks and value stocks is now historically wide on some metrics, such as the price-to-earnings ratio.

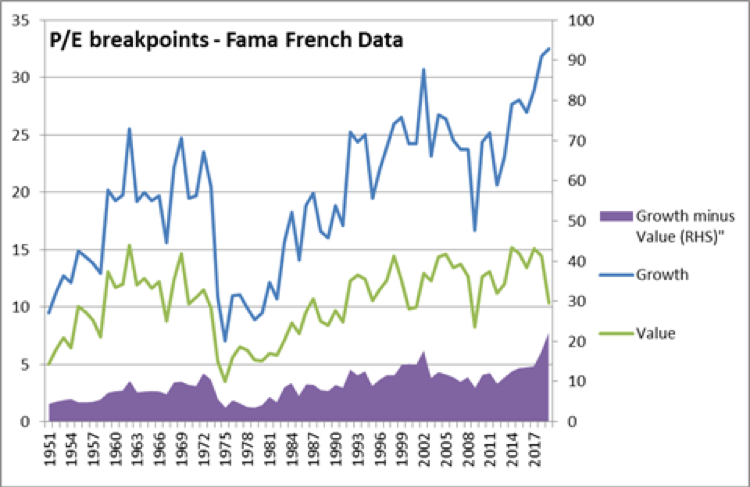

Price-to-earnings (P/E) ratios of growth and value stocks

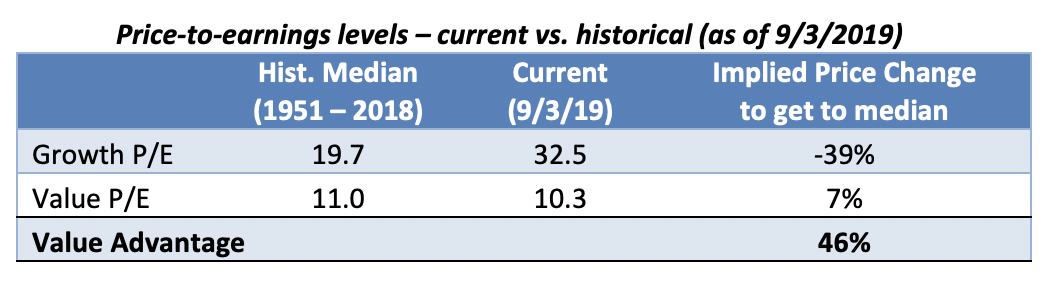

Using data from Fama-French, price-to-earnings ratios can be tracked back to 1951. This data is divvied into breakpoints at various P/E percentiles. For this article, the proxy for value stocks looks at P/E ratios in the 25th percentile of historical data – an arguably middle-of-the-road value position. Likewise, the proxy for growth is the 75th percentile. Since Fama-French use end-of-the-prior-year valuation breakpoints, there is a one-plus year gap between the latest Fama-French data and today’s valuation levels. As a result, current (as of 9/3/2019) P/E ratios for these percentiles are estimated based on bottom-up data collected from YCharts. Specifically the current P/E ratios considered both the 1) current actual levels for corresponding earnings yield (and P/E) percentiles found in YCharts data and 2) applying the rate of change in those levels (from the time of the latest Fama-French data to today) to the latest Fama-French data points. Anecdotally, the results (P/E levels) of the companies identified in the screen run later in this report are consistent with these levels.

As the chart below demonstrates, the gap between P/E ratios for growth versus value has never been as extreme as it is currently. Growth stocks have significantly high P/E ratios relative to those for value stocks. We are in outlier territory.

Source: Fama French (Dartmouth website, “E-P_Breakpoints”), YCharts, Inc., Aviance Capital Partners.

Normalized valuations

What would the price impact be if each of these two groups tended towards a long-term median level of the respective group? Growth stocks, currently at a P/E of 30, trade at a level significantly higher than the median of 20 of its group since 1951. Value stocks, on the other hand, are reasonably priced as shown below.

Source: Fama French (Dartmouth website, “E-P_Breakpoints”), YCharts, Inc., Aviance Capital Partners.

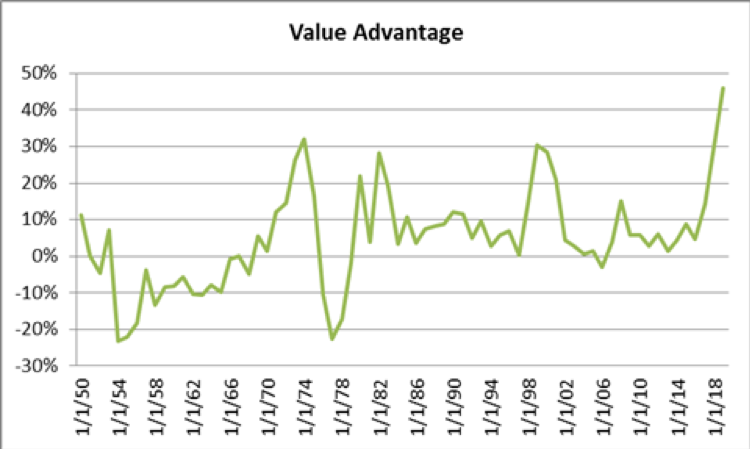

Simply looking at each price adjustment necessary to return to normal levels shows a large 46% advantage for value stocks.

The advantage has never been this large, as the chart below indicates. The last time value stocks were at a price disadvantage was in 2006, following a run-up in value stocks and when the dominance of growth stocks began.

Source: Fama French (Dartmouth website, “E-P_Breakpoints”), YCharts, Inc., Aviance Capital Partners

What to do?

A few observations that may yield some insight as investors decide whether or not to buy-in to the argument that value stocks are poised to outperform growth:

- Accepting a roughly 46% relative price advantage of value stocks does not make up for even half of the great run growth investors have enjoyed since 2006, relatively speaking.

- Since growth stocks are more expensive than value stocks, and value stocks are cheap, investors may experience more downside in growth stocks and relatively less upside from value stocks.

- A clear catalyst for when dominance switches from growth to value is unknowable.

- However, value advantages this extreme, as demonstrated in the previous chart, do not last very long.

Two simple data screens

Finally, accepting the above premise leads to the questions:

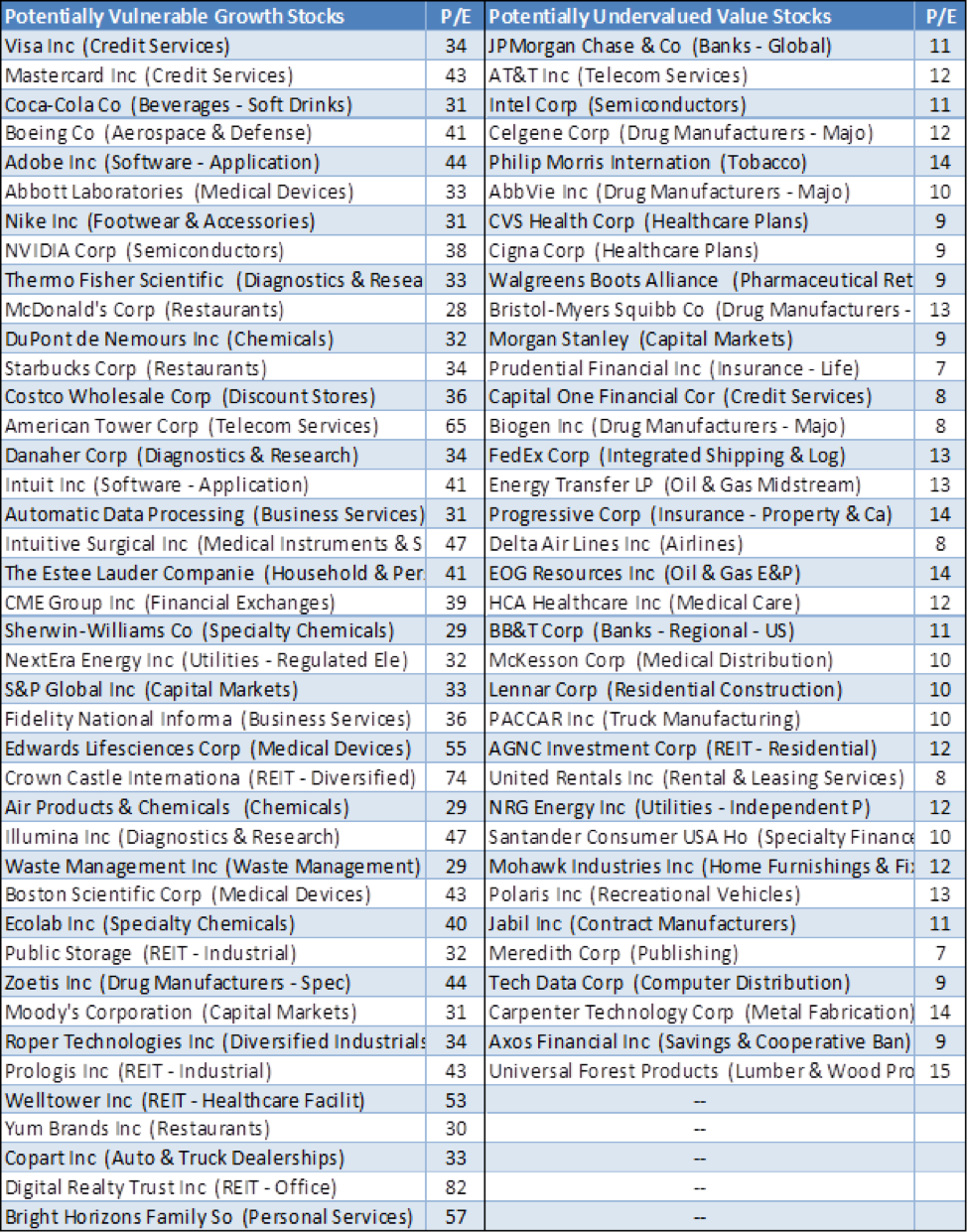

- Which growth stocks are at risk?

- Which value stocks are poised to perform well?

Stock screens are fraught with fallibility. However, the table below broadly attempts to capture the essence of recognizable companies that fall into one or the other category.

Screen for Vulnerable growth stocks

- Price-to-earnings ratios in the top 33%;

- U.S. companies;

- Either $35 billion or more in market capitalization or largest in industry; and

- Estimated growth less than 15% (I exclude rapid growers as these are likely less vulnerable).

Screen for undervalued value stocks

Source: YCharts, Inc.

The information provided in the chart above should not be considered a recommendation to purchase or sell any particular security. It should not be presumed that Aviance Capital Partners has purchased, sold, or recommendation any of the above securities for clients. To the extent Aviance Capital Partners has transacted in, or recommended that a client transact in, any of the securities listed above, it should not be presumed that above chart represents all of the securities purchased, sold, or recommended for advisory clients. Further, it should not be assumed that investment in any of the securities reflected above were or will prove profitable, or that any investment recommendations or decisions that Aviance Capital Partners makes in the future will be profitable or will equal the historical investment performance of the securities discussed herein. The securities represented are not intended to reflect any client account or portfolio holdings.

Conclusion

I question whether value investing still makes sense. Over the past several decades, the nature of the markets and its participants has changed dramatically. Consider for example:

- While “value” investing was a lesser known methodical investing approach several decades ago, it is now simply one of many potential well-known factors.

- While only a minority of households held stocks (directly or indirectly) up through the 1980s, a majority of households now own stocks in one way or another.

- The number of stocks has declined considerably over the past two decades.

- Passive investing through exchange-traded and mutual funds has become a dominant method of investing.

As these changes have become more front-and-center in the investment world, value investing has underperformed growth investing by 140% since 2006. It is only reasonable to question the benefit of adhering to a potentially antiquated approach to building wealth.

On the other hand, logic and the broader body of evidence for value investing tempers this concern. After all, a good bargain will always be common sense. Further data going to back nearly 100 years demonstrates a clear advantage to value investing.

Today, valuation metrics show that value stocks are more attractively priced relative to growth stocks than usual. Specifically, the difference in price-to-earnings ratios between value and growth stocks has never been this extreme. Consequently, for those investors who intuitively appreciate the hallmarks of a good bargain, today is a great time to consider value investing.

Jack Brown is a partner and chief investment officer of Aviance Capital Partners, a Florida-based registered investment advisor.

More Active Management Topics >