The CFP Board’s Misdeeds Demand Accountability

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

It’s time for the CFP® Board to acknowledge that it has been misleading consumers and causing them financial harm. The penalties for its misdeeds must go beyond mere admonishments and pressure to fix its vetting and enforcement problems. The scale and brazenness of the Board’s transgressions warrants financial accountability and an end to the Board’s efforts to gain control over the financial planning industry.

On July 30, 2019, the Wall Street Journal ran a scathing front-page exposé on the CFP® Board of Standards’ failure to properly vet its members and the hypocrisy of this failure relative to its self-righteous public messaging. Specifically, WSJ investigative reporters, Jason Zweig and Andrea Fuller ran background checks on more than 70,000 CFP® members using FINRA Broker Check compared the output against the CFP® Board’s go-to verification site for consumers.

They found more than 6,300 CFP®s with significant disclosure events on their FINRA profile who were effectively endorsed by the CFP® Board as having clean disclosure histories. The number includes nearly 500 CFP®s with criminal charges (140 for major felonies), hundreds of CFP®s with client complaints that were settled for $10,000 or more, and hundreds more with personal bankruptcy filings.

I worked with authors to help develop the story. In the article, the reporters noted that the CFP® Board took "strong issue" with my suggestion that the organization does not vet its members and that its multi-million dollar "consumer awareness" campaigns are setting people up to be deceived. My rebuttal, which is posted on the CFP® Board’s LinkedIn page reads, as follows:

|

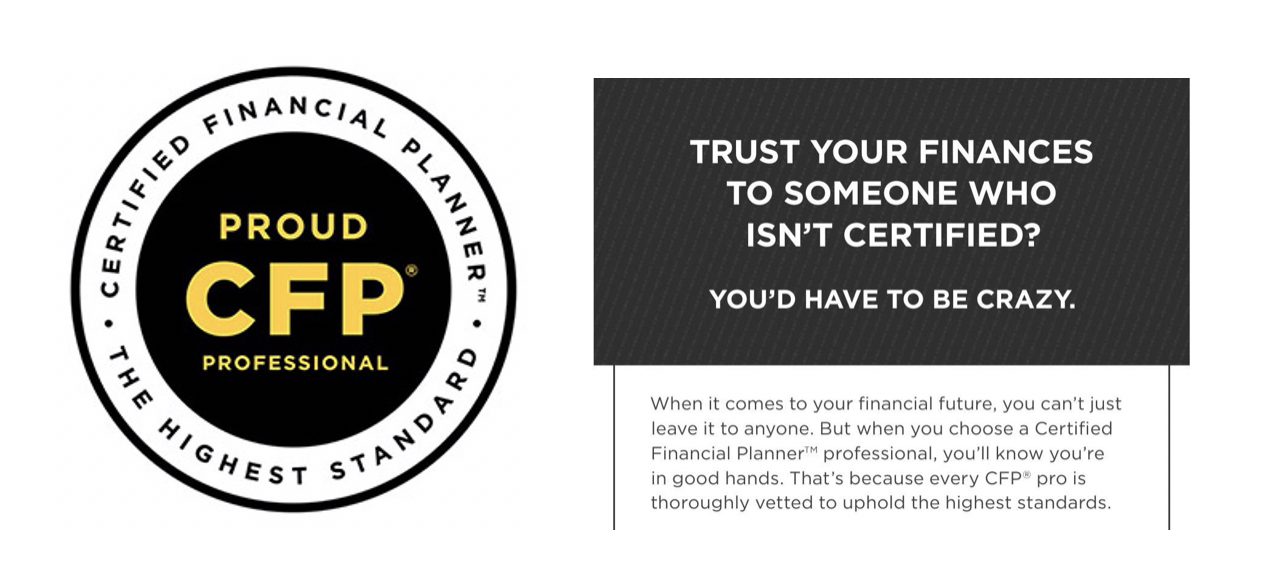

(1) The WSJ article states that more than 6,000 CFP®s who had significant disclosure events on their FINRA records were endorsed on the CFP® Board's verification site as having no disclosure events. Res ipsa loquitur (the fact speaks for itself). (2) This is an example of the CFP® Board's messaging to consumers - "When you choose a CFP®, you'll know you're in good hands. That's because every CFP® pro is thoroughly vetted to uphold the highest standards." I believe most reasonable people would agree that this messaging is misleading/deceptive in the wake of the WSJ article findings. |

In responding to the WSJ article, CFP® Board CEO Kevin Keller essentially played the victim by stating that it is unfair to its members for the Board to publish SEC and FINRA disclosure events prior to doing its own investigations. He also objected to the public disclosure of some bankruptcy filings. In a separate response, the CFP® Board did acknowledge that its self-reporting policy was not as effective as anticipated and that it is taking corrective measures to review the background checks of existing members.

However, the Board defended its past actions by stating that it is not a regulatory agency and, as such, does not have the operating resources or access to information to properly police its members. Barbara Roper, the director of investor protection for the Consumer Federation of America, was quick to jump to the CFP® Board’s defense in stating, “They [the CFP® Board] made a big mistake by relying on self-reporting after the initial vetting process, and they’ve taken steps to address that shortcoming in their process.”

What is conspicuously absent from the CFP® Board’s mea culpa and from Roper’s casual dismissal of the WSJ article’s findings is any suggestion that the Board should be held accountable for the harm its actions may have had on the investing public.

Accountability for harming consumers

To illustrate by example how the CFP® Board’s lax oversight and misleading messaging has likely harmed consumers, the impetus for my reaching out to Jason Zweig with a story idea in late 2018 was an encounter I had with a 401(k) rep. This person was boasting of his CFP® designation and his personal wealth to a friend of mine to whom he was pitching a group annuity contract. My friend asked me to check the fellow out. I first ran his name through the CFP® verification website. The report confirmed his CFP® certification and showed no disclosure events or bankruptcies.

However, when I entered his name into FINRA Broker Check and SEC IAPD, I found five disclosure events, including three complaints settled for $75,000 or more, an unrelated termination for cause, and a bankruptcy filing two years ago. The disclosure of this information was obviously of great value to my friend in deciding whether he should place his trust in this “gentleman.”

For its part, the CFP® Board has spent millions of dollars over the past decade on “consumer awareness” campaigns featuring the previously cited tagline and other similar messages including the following:

If they’re not a CFP® Pro, you just don't know.

Anyone can call themselves a "financial planner." Only professionals who meet the Board's rigorous standards can call themselves a CFP®.

How many consumers were swayed by this messaging to trust CFP®s with similar disclosure histories to those of the salesman who was pitching my friend an expensive insurance product with opaque fees and expenses? The number of consumers who have been harmed by the CFP® board’s irresponsible messaging is likely not small.

Further, any suggestion that the CFP® Board was unaware of dangers of promoting its members as being more trustworthy is preposterous. The CFP® Board has long been aware of its feckless vetting (relying on "self-reporting") and of the fact that some of its members obtain the CFP® mark in order to convey trust so that they may then defraud their clients.

For example, disgraced former CFP® Bradford Bleidt, who was convicted in 2005 of running a massive (by pre-Madoff standards) Ponzi scheme, openly admitted that he used the CFP® mark to gain trust in order to lure new victims. There are other high-profile examples of CFP®s who have used the marks for self-enriching purposes as well.

While the CFP® Board’s response bemoans a lack of resources for enforcement, it spends more than $10 million each year on PR – money that could be easily reallocated to consumer protection. Conversely, it took me less than two minutes to run the afore-referenced shady CFP® through Broker Check. The WSJ reporters managed to run 70,000 names through both verification sites in the just a week or two. Their efforts were considerably more time consuming than mine but did not require millions of dollars. The CFP® Board could easily have crosschecked its members against FINRA Broker Check and SEC IAPD, but chose not to do so.

Willful negligence demands accountability.

Accountability for fostering consumer confusion

In addition to the direct harm it has inflicted on consumers by steering them to and encouraging them to trust CFP®s with significant regulatory disciplinary and financial disclosure events, the CFP® Board should also be held accountable more broadly for misrepresenting to consumers that the financial planning profession is unregulated and that its standard of conduct and authority supersede that of the regulatory authorities. The following image illustrates how the Board’s messaging implies that the financial planning profession is unregulated:

In truth, all financial advisors whose services include providing investment guidance to their clients are restricted from using the term “financial planner” unless they are registered with the SEC as an Investment Adviser Representative (IAR). The applicability of the Investment Advisers Act of 1940 to financial planners is outlined in detail in SEC Release IA-1092: Applicability of the Advisers Act to Financial Planners.

As referenced in the WSJ article, in a PR video produced by the Board, CFP® Board General Counsel Leo Rydzewski proclaimed that federal regulation of financial planners is at a basic level and that the CFP Board’s standards “rise above” all other authorities. When confronted by the WSJ reporters about this comment, Rydzewski doubled down by asserting that the CFP® Board’s standards of conduct go beyond what is required by the SEC and state regulatory authorities. Two examples of advertising material showing how the CFP® Board implies that its standards are higher than those of the regulatory authorities are as follows:

The basis for the CFP® Board’s rhetoric centers around the organization’s newly minted Code of Ethics and Standard of Conducts, which apply the Board’s self-defined “fiduciary standard” to all its members. However, the suggestion that its fiduciary standard is higher than the standard that applies to financial planners under the Advisers Act is beyond misleading.

In my opinion, it is fraudulent.

To prove this point, I reviewed the Board’s new Code of Ethics and Standards of Conduct, which are slated to go into effect on October 1, 2019, and found that the Board does not require CFP®s to disclose either the amount or percentage of compensation they may receive from the sale of products with opaque commissions. For example, a CFP® who is an insurance agent (but who is not registered as an IAR with the SEC) is not obligated under the Board’s new standard to disclose the amount of commission he or she may receive from the sale of life insurance or annuity products. Further, while the new code does require CFP®s to disclose “material conflicts of interest,” this disclosure does not need to be in writing. This reliance on oral disclosure will likely be as effective as self-reporting has been for disclosure events.

For its part, the fiduciary conduct rules the SEC applies to financial planners are far more restrictive and more clearly defined. Specifically, under the SEC’s “material facts” disclosure rules, financial planners are required to, “…disclose fully the nature and extent of any interest the investment adviser has in such recommendation, including any compensation the investment adviser would receive from his employer in connection with the transaction.” Further all SEC-registered financial planners are required to provide advance written disclosure of all potential conflicts of interest. They are also required to provide written information about their educational background and experience and any prior or pending disclosure events.

Equally misleading in the CFP® Board’s rebuttal to the WSJ article is Rydzewski’s defense that his “reference to superior standards refers to higher education and ethics among CFP®s that ‘go beyond what is required by the government at the federal or state level.’” To be clear, while the CFP® Board promotes its correspondence courses as college or graduate-level training, the CFP® training program and designation lack the academic accreditation or standing to support that claim. Prior to 2008, a college degree was not required to sit for the CFP® exam. Even today, no prior academic experience in finance or economics is required.

While the SEC does not have any established educational requirements for financial planners, there are is no data to support Rydzewski’s claim that CFP®s are more educated (or ethical) than non-CFP® financial planners.

Indeed, there is good reason to believe the opposite is true. The SEC requires all IARs to provide advance (and ongoing) written disclosure of their educational and professional experience in SEC Form ADV part 2A & 2B. Non-CFP® financial planners who have an academic background in finance would likely be less insecure in their credentials than those who do not. For example, financial planning industry thought leader Michael Kitces openly discloses in his bio that he entered the financial services industry as an insurance agent with an undergraduate degree in psychology and theatre from Bates College and that he enrolled in the CFP® program to obtain the finance background he did not receive in college. Legions of other advisors who had no prior academic experience also have obtained the CFP® designation in order to enhance not only their knowledge, but also their marketing credibility.

Ironically, the CFP® Board has been sermonizing ad nauseum about how the SEC has fostered consumer confusion in maintaining a bifurcated regulatory structure between the brokerage and investment advisory communities. In truth, the CFP® Board’s misleading, self-promotional statements concerning its false fiduciary standard and its place in the regulatory system have created far more confusion. In the words of fi360 and 3Ethos founder, Don Trone, “If the CFP® Board were a country, it would be North Korea. The Board has done more harm to the fiduciary movement than any other organization.”

A culture of bad behavior

Consistent with its recent actions as described above, the CFP® Board has a long history of ethical transgressions in its dealings with the public, dating back to its very origin. In a recent Nerd’s Eye View podcast entitled, Insights from the History of Financial Planning Since the First CFP® Class, Michael Kitces and his guest, Ben Coombs, informed listeners that the original purpose of the designation was to give credibility to insurance agents to enable them to compete in product sales with securities brokers. The discussion guided listeners through the unseemly late 1970s and early 1980s when CFP®s temporarily set aside their focus on pushing high-commission insurance products to push even higher commission-paying, ill-fated and often fraudulent oil and gas tax shelters.

The discussion also traced the origins of the College for Financial Planning in Denver in the 1980s. In a manner similar to that of many of today’s “diploma mills,” the term “college” was chosen to give the appearance of academic credibility when, in fact, it was merely the organization that owned and conferred the CFP® mark.

The arrival of current Board CEO Kevin Keller, a career lobbyist, in 2007, brought an increased level of sophistication to the CFP® Board’s lobbying, public relations and branding initiatives. But there were few changes the organization’s ethically-challenged culture. Indeed, in the decade since Keller’s arrival, the Board has faced persistent criticism for a lack of transparency, a proclivity for placing its interests above those of the consumers it purports to protect and high executive compensation packages. A sampling of articles supporting this view are as follows:

CFP Board Chief Executive Kevin Keller Joins $1million Compensation Ranks (Investment News 2/27/2019)

CFP Board: Fiduciary Hypocrites (ThinkAdvisor 6/28/2018)

Show me the money: Financial advisory trade groups pay handsomely (Investment News 12/1/2015)

Global Junkets Lavished On Directors Fuel CFP Board High Life (FA Magazine 4/3/2014)

Is the CFP Fiduciary Promise for Real? (Financial Planning 10/29/2013)

CFP Board chairman steps down amid ethics concerns (Reuters 11/2/2012)

The Curious Case of the CFP Board and a Double-Dipping CFP (Think Advisor 9/24/2012)

Restoring Trust in the CFP Mark (FA magazine, 4/6/2009)

Defining and quantifying accountability

Having established that the CFP® Board has been both willful and proactive in harming consumers and in fostering confusion over regulatory standards, it should be clear that the findings in the WSJ article represent more than just a “big mistake.” The Board’s promise to improve its vetting and enforcement processes is not an acceptable solution. Instead, the article should serve as a wake-up call. Federal and state regulators, the financial planning community, and the public at large must take action to hold the organization and its leadership accountable for its actions.

One easy step toward accountability would be for the SEC to issue a cease and desist letter to the CFP® Board that includes ordering it to eliminate any and all suggestions that it represents a higher standard than the regulatory agencies and to prohibit the use of the CFP® mark by insurance agents and brokers who are not registered with the SEC as IARs. The letter should also impose a penalty of a complete ban on the use of the CFP® mark and the designation “Certified Financial Planner” if the Board fails to reform its behavior.

A second measure for the SEC and the individual states’ attorneys general to consider is the degree to which the CFP® Board should be held financially liable for the harm it has brought to consumers by encouraging them to believe that CFP®s are more trustworthy, more ethical, and more educated than SEC-registered, non-CFP® financial planners. In the wake of the WSJ article, individual plaintiffs’ attorneys may step in to assist with obtaining compensation for victims of the Board’s deceptions.

However, both the SEC and FINRA have not been shy about assigning civil penalties to individuals and firms that have violated its rules. While the CFP® Board may claim that it exists outside the SEC’s jurisdiction, in 2018, the SEC took enforcement against certain cryptocurrency firms for operating as unlicensed or unregistered investment advisers. To the extent that the CFP® Board has encouraged non-SEC registered stockbrokers and insurance agents to obtain and use the Certified Financial Planner designation, the legal grounds for SEC intervention may apply here too.

Assigning a monetary value to the harm the CFP® Board has done to consumers through its lack of vetting and irresponsible advertising campaigns is likely without precedent. There are, of course, abundant examples of settlements the SEC has exacted from individual CFP®s. For instance, CFP® Board of Standards’ “Goodwill Ambassador,” Jill Schlesingers’ SEC IAPD report reveals that she agreed to a $10,000 settlement in December 2008 for her role in misrepresenting financial figures in a private placement scheme with her former business partner, convicted Ponzi-schemer Dave Brochu. Consistent with the WSJ article findings, no mention of this disclosure event appears on Schlesinger’s profile on the CFP® Board’s verification website.

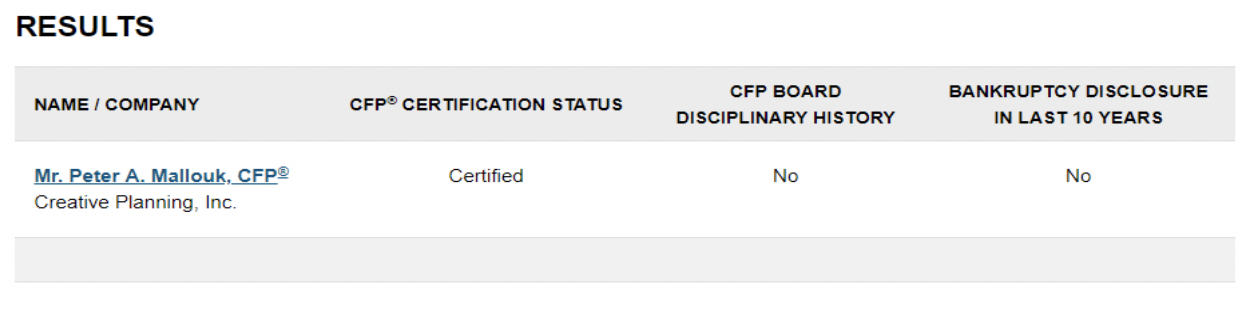

More recently and perhaps more on point, in 2018, Peter Mallouk, CEO of RIA Creative Planning was fined $50,000 and Creative Planning was ordered to pay $200,000 civil penalty for a range of ethical and regulatory violations that are not dissimilar to the CFP® Board’s practices. The details of Mallouk’s settlement are a matter of public record, but also made headlines in the national financial media. Again, no mention of these disclosure events appears on Mallouk’s CFP® Board verification site profile.

The scope of these individual transgressions pales in comparison to both the scope and duration of the CFP® Board’s misrepresentations to consumers. According to the CFP® Board, the CFP® verification site had approximately 765,000 visits in 2018. The number of eyeballs that have seen the Board’s national television and online advertisements is likely in the millions. Civil penalties on the order of millions or tens of millions of dollars would seem commensurate with the scale of the damage the Board has likely caused and would serve as a powerful deterrent against future bad behavior.

Regardless of the degree to which justice is served, I sincerely hope this commentary in the wake of Zweig and Fuller’s outstanding reporting helps put an end to the CFP® Board’s publicly stated quest to make the CFP® mark a required standard for the financial planning profession – a move that would give the CFP® Board monopolistic control. Regardless of how much money it is has spent on building brand awareness, the CFP® Board has demonstrated beyond any reasonable doubt that it is wholly unqualified to serve as a standard-bearer for our profession.

John H. Robinson is the founder of Financial Planning Hawaii and a co-founder of software maker Nest Egg Guru. He has published dozens of papers and articles on a broad range of financial planning topics, including numerous contributions on the fiduciary standard and ethical issues pertaining to the financial planning profession.

Related Reading

Michael Kitces is Wrong About the CFP Board. Here’s Why (Financial Planning, January 2019)

Does the CFP Board Choose Advertising over Enforcement (Financial Planning, 9/24/2018)

Why the CFP Board Should Not Govern the Financial Planning Profession (August 2018)

FPA Lobbies for Stronger Advisor Regulations on Capital Hill (FA magazine, 6/7/2018)

Most CFPs are brokers. Fiduciary Advocates say that's a problem. (Financial Planning, 3/9/2018)

Do the CFP Board's New Standards Go Far Enough? (Financial Planning, 3/29/2018)

The CFP Board Code of Conduct Standards are a "A Mess" (FA magazine,3/9/2018)

A Path Forward for the CFP Board (Advisor Perspectives 3/13/2018)

The CFP Board's Duplicitous Dance (Advisor Perspectives August 2017)

Just Say No to CFP Board’s New Standards (Think Advisor, 7/11/2017)

CFP Board Commission On Standards Expands CFP Fiduciary Duties… But Can It Enforce Them? (Kitces 6/26/2017)

Board to Death: IS the CFP Board’s New Fiduciary Standard Really Better Than No Standard at All? (ThnkAdvisor 6/21/2017)

Secret recording: A CFP at JPMorgan pushed high-priced products (Financial Planning 10/13/2016)

Former Rhode Island StrategicPoint Bos Brochu’s Epic Fall (GoLocalProv.com 2/23/2016)

Show me the money: Financial advisory trade groups pay handsomely (Investment News 12/2015).

How the CFP Board is getting its $40 million's worth from its Advertising Campaign (RIA Biz 7/24/2014)

Is the CFP Board Losing Credibility in the Eyes of Advisors? (Wealth Management 4/11/2014)

Did CFP Board Shorten Exams to Lure Certificants? (Think Advisor 1/17/2014)

The Hypocrtical Assertions of CFP Lobbyists (Advisor Perspectives 2014)

CFP Accused of Ponzi Scheme – Selling Fake Investment (Fox6Now.ocm 5/30/2013)

When Your Financial Planner Doesn’t Tell All (Wall Street Journal, 10/4/2013)

Is the Fiduciary Standard a Joke (Wall Street Journal, 9/12/2012)

Is the CFP Fiduciary Promise for Real? (Financial Planning, 10/29/2013)

Why Aren't CFPs Always Subject to a Fiduciary Standard (ThinkAdvisor, 12/3/2014)

What’s Behind The CFP Board’s Big Fee Increase (RIA Biz 4/11/2011)

CFP Board strips credentials from admitted Ponzi-schemer (Investment News, 2/19/2010)

Many regrets for those lured by Bradford Bleidt (Boston Globe 1/20/2009)

Fee-Only Pioneer Zabalaoui Sentenced To 8 Years (FA Magazine 8/6/2009)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All