Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“In the financial world, good ideas become bad ideas through a competitive process of ‘Can you top this?’”

Jim Grant

We live in interesting times, at least when it comes to the financial world. Since the global financial crisis (GFC) shook the financial world more than 10 years ago, central bank balance sheets have continued to expand. As Figure 1 shows, combined total assets of the Fed, ECB, and BoJ have increased by nearly four times.

In a policy world dictated by once-bitten, twice-shy response mechanisms, central banks have been conducting policy with a promise to not let an event like the GFC recur. However, they are confusing the symptoms with the cause. The result is that central banks are too focused on financial market prices. They are conducting policy based on such prices and their tolerance levels for price declines is getting narrower.

The impact of these misplaced policy actions has been to suppress interest rates and fan mispricing of risk. Consider that nearly $13 trillion worth of bonds are priced for negative yields globally. As per a story on ZeroHedge, there are 14 euro-denominated junk bonds that carry a negative yield1. Clearly, market participants are pricing these securities for greater fools.

Figure 1. Central bank balance sheets and the S&P 500 index

Source: Central Banks: Balance Sheets, Yardeni Research, May 20, 2019

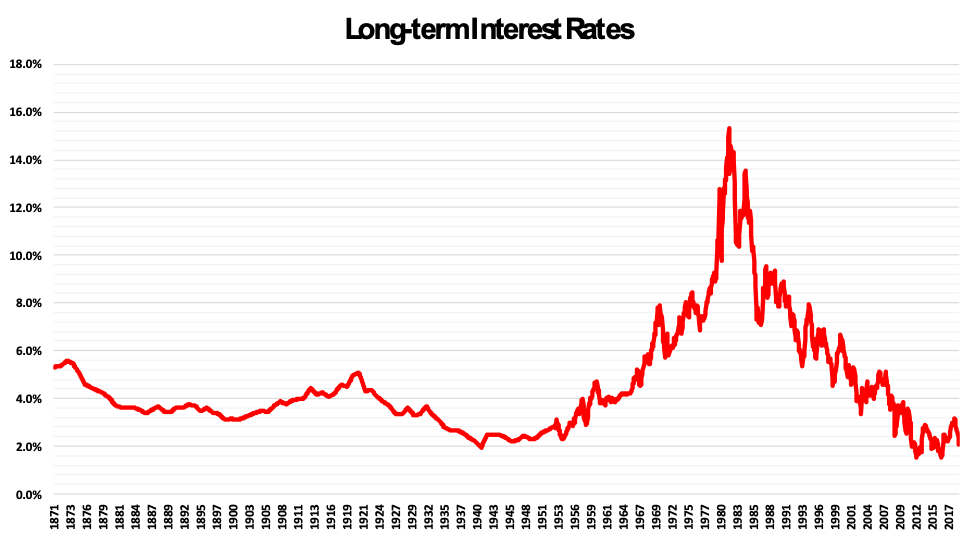

Figure 2 shows the long-term interest rates for the U.S. Interest rates are in the all-time low zone.

Figure 2. Long-term interest rates, U.S.

Source: Data from Robert Shiller

The impact of interest rate changes on equity pricing

Interest rates are a central piece of the security pricing exercise. Market participants base the discount rates on the sovereign bond rate, which is the proxy for risk-free rate.

Interest rates, directly and indirectly, affect the valuation exercise in four primary ways. They affect the discount rates. They have an impact on corporate cash flows available to equity shareholders via interest expenses. To the extent that interest rate changes have been driven by changes to economic growth outlook, they affect the growth rate of corporate cash flows. And, lastly, they affect the terminal valuation multiple applied to cash flows at the end of the forecast period.

Interest rate changes: Value versus growth

Of those four effects, the discount rate impact is the most potent and the one of greatest concern to market participants. However, what is not as well understood is the differential impact interest rate changes have on value and growth stocks.

Value stocks, as traditionally defined, have lower growth rates than their growth counterparts. A larger portion of their business value is derived from cash flows in the near future. On the other hand, much of the value associated with growth stocks is derived from cash flow in the distant future. If one were to think of this in fixed income securities terms, value stocks have a significantly shorter duration than growth stocks.

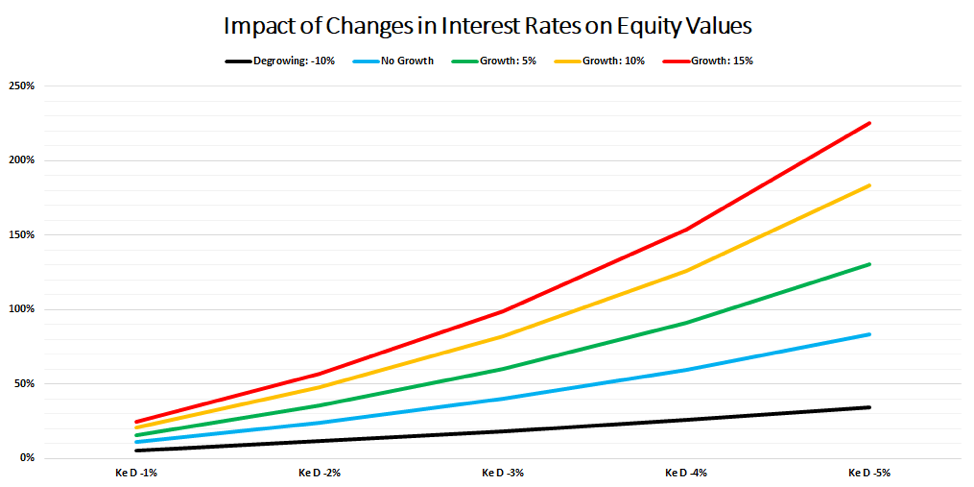

Figure 3 shows the percentage change in equity values as interest rates decline with interest rate delta of -1% to -5%. The black line represents a declining free cash flow stream while the red line represents a free cash flow stream expected to grow at 15% over an extended future. A reduction in interest rates affects these free cash flow streams disproportionately. The higher the expected growth, the larger the impact.

Figure 3. Impact of changes in interest rates on equity valuations

Figure 3 shows that interest rate declines have a larger positive impact on the value of growth stocks than they have on value stocks. Of course, the converse is true as well. This is similar to what happens in the fixed income world: the higher the duration, the larger the impact of interest rate fluctuations.

This analysis assumes that changes in interest rates are not associated with changes to the growth outlook – an assumption that is unlikely to hold. Frequently, changes to interest rates are associated with changes in the growth outlook, which acts to counterbalance the discount rate effect of changes in interest rates.

Value versus growth: Taking the idea too far

As Jim Grant’s quote suggests, the financial world has a tendency to take a good idea and push it too far. We are of the view that we are living in the midst of such times. Market participants, across the board, are embracing high expected growth and are shunning areas of perceived low growth.

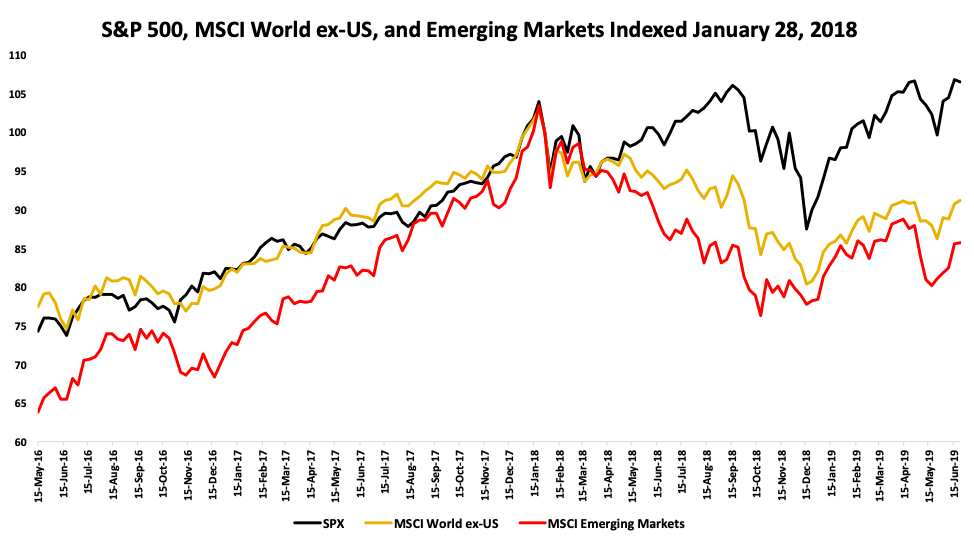

Figure 4 shows the performance of U.S., non-U.S. developed and emerging market equities with each indexed to January 2018. Since then, U.S. equity markets have significantly outperformed the rest of the world.

Figure 4. Performance of equity markets – U.S. equities pulling away

Source: Data from investing.com

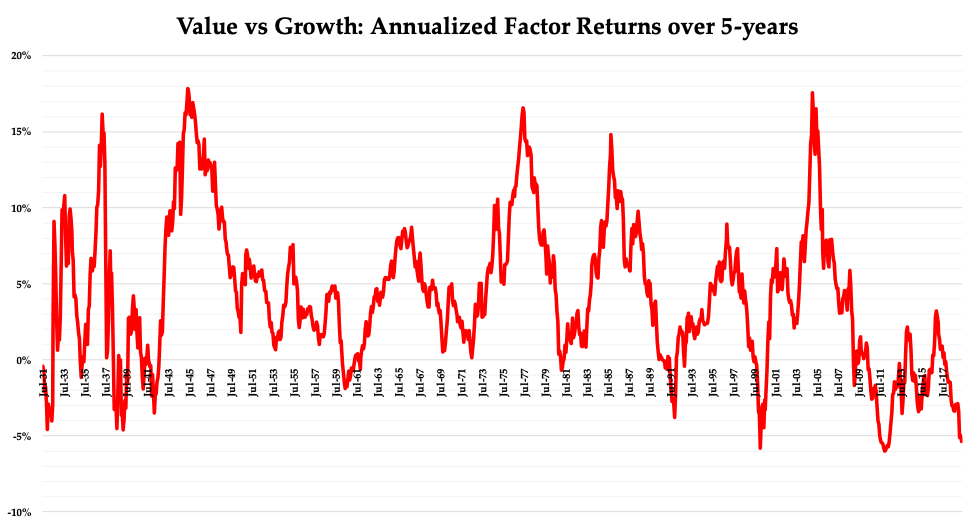

Figure 5 shows the performance of value versus growth over the past nearly 90 years. The chart plots the five-year annualized spread of value versus growth. Value has experienced its worst decade of the past 90 years and the past five-year factor returns are now nearly the worst.

Figure 5. Value versus growth factor returns

Source: Data from Kenneth R. French’s data library

The differential pricing of non-U.S. equities and value versus growth is largely driven by market participants’ preference for growth.

A valuation-driven view: Global moats index

As valuation-driven investors, we do not subscribe to the traditional definitions of value and growth. Clearly, a business that earns returns on the invested capital well above its cost of capital and is able to deploy additional capital at such high returns, should see its earnings or book value valued significantly more than that of an average business. The extent of this premium is a matter of the width of excess returns earned, the duration over which such excess returns can be sustained and the growth that such a business can generate.

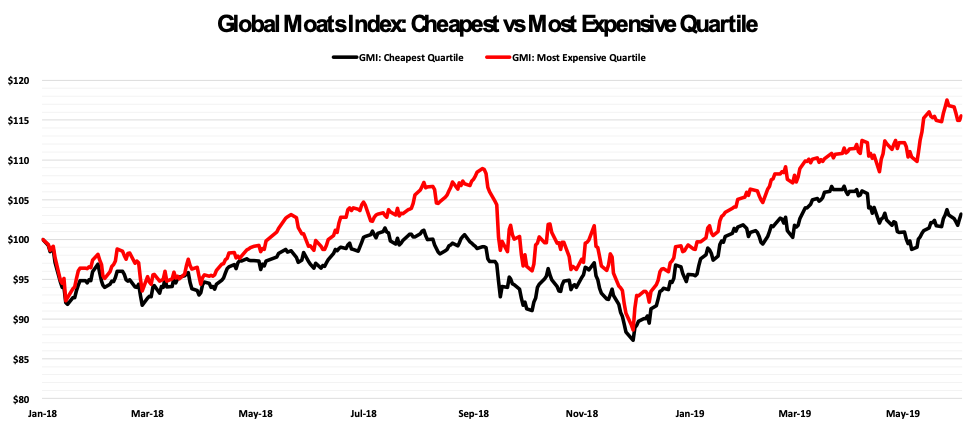

In our Global Moats Fund, we are focused on a basket of high-quality companies, a proprietary basket referred to as the global moats index (GMI). Our research team maintains a valuation band on each one of our companies with our valuation bands accounting for each one of the factors discussed above. Interestingly, our own bottoms-up valuation findings are starting to confirm the market valuation behavior discussed earlier. Much as is seen in the case of U.S. versus other markets, over the past 18 months, we have seen market participants embracing high growth situations and do so without regard for the price being paid.

Figure 6 shows the investment performance of stocks in the cheapest quartile (Q1) versus the most expensive quartile (Q4) within the GMI. As opposed to being based on traditional valuation multiples like P/BV or P/E, the chart below is based on bottoms-up valuation of each one of the businesses in the index.

As market participants are embracing growth, it is not a surprise that Q1 stocks within our index are associated with lower expected growth than those in Q4. However, our valuations already take into account these differential growth rates. Clearly, market participants are paying too high a premium for the privilege of owning growth.

Figure 6. Global moats index – Cheapest versus most expensive stocks

Source: Multi-Act EquiGlobe

Summary

John Galbraith wrote that, “for practical purposes, the financial memory should be assumed to last, at a maximum, no more than 20 years. This is normally the time it takes for the recollection of the one disaster to be erased and for some variant on previous dementia to come forward to capture the financial mind.”

It has been nearly 20 years since the tech bubble reached its peak. We are starting to see an investment pricing behavior that is similar to the tech boom. Then it was tech versus non-tech. Now, it is high growth versus everything else. As a new dementia takes over, we position differently.

Baijnath Ramraika, CFA, is a cofounder and the CEO & CIO of Multi-Act Equiglobe (MAEG) Limited and is the Executive Director at Sapphire Capital. As a portfolio manager, he manages the Global Moats Fund and the India Moats Fund. Contact him at [email protected]. Baijnath’s thoughts and ideas can be read at his blog at www.symantaka.com

Prashant K. Trivedi, CFA, is a cofounder of MAEG and the founder and chairman of Multi-Act Trade and Investments Pvt. Ltd.

MAEG is an investment manager and manages the Global Moats Fund, an investment fund that invests in a global portfolio of high-quality businesses with sustainable competitive advantages. Sapphire manages the India Moats Fund, an investment fund that invests in a portfolio of high-quality Indian businesses with sustainable competitive advantages.

Multi-Act is a financial services provider operating an investment advisory business and an independent equity research services business based in Mumbai, India.

1 https://www.zerohedge.com/news/2019-07-10/redefining-high-yield-there-are-now-14-junk-bonds-negative-yields

More Fixed Income Topics >