In my view, a trade war between the US and China is the key risk to the global economy. In a world of integrated supply chains and connected financial markets, its impact is bound to spill beyond their borders and affect the global economy. All eyes are now turned to the June 28 G-20 summit, where the two countries’ presidents are expected to meet. What could this all mean for emerging market (EM) growth and central bank policy? I explore this question below.

Will the G-20 summit bring a truce?

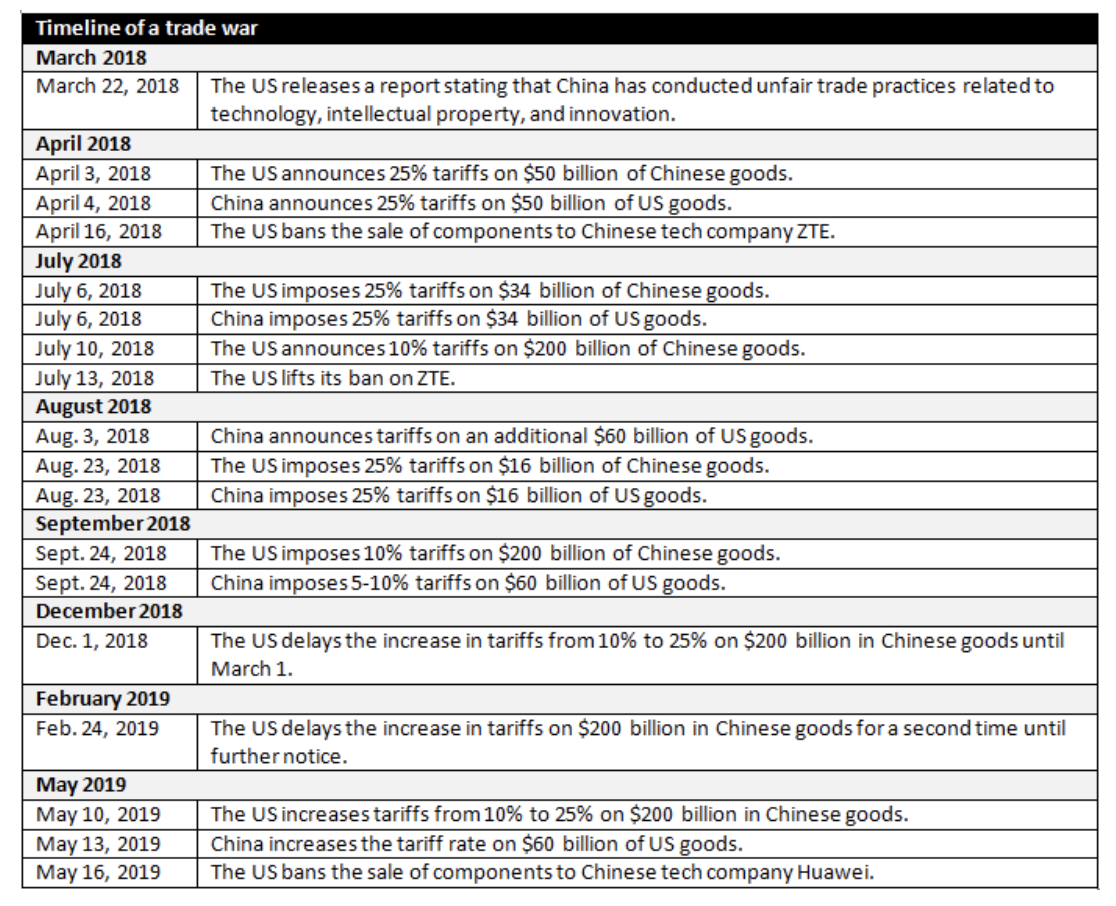

US-China trade tensions have intensified since May, although they have been a concern for investors since early 2018 when the US announced the first tariffs on Chinese imports. In the interim period, we have gone from a tit-for-tat escalation of tariffs to intense engagement and expectations of an imminent deal, and most recently, to a breakdown in talks and further escalation (see table below). We will soon find out if there is light at the end of this tunnel or we are at the brink of an outright trade war.

Recent rhetoric suggests a hardening of positions on both sides. Hence, I do not expect trade tensions to be completely resolved at the G-20 meeting between US President Donald Trump and Chinese President Xi Jinping. Nonetheless, another truce may materialize, avoiding further escalation of tariffs and various other non-tariff barriers, and resumption of talks that could lead to an eventual deal later in 2019 or early 2020.

Then there is the question of the form that such a deal may take. The trade dispute between the US and China is now broader than tariffs and has been extended to security and technology issues.1 Even if a trade deal could be reached to save the day, we think the strategic competition between the two countries will be one of the defining themes for the next few decades at least, with repercussions for the global economy and emerging markets. In the medium-to-long term, this could generate losers and winners in certain situations as countries change trading partners and supply chains adjust to the new geopolitics.2 Nonetheless, I believe everyone would eventually lose overall as global growth prospects decline in an environment of protracted geopolitical tensions and de-globalization of production chains.

What’s been the impact on emerging markets?

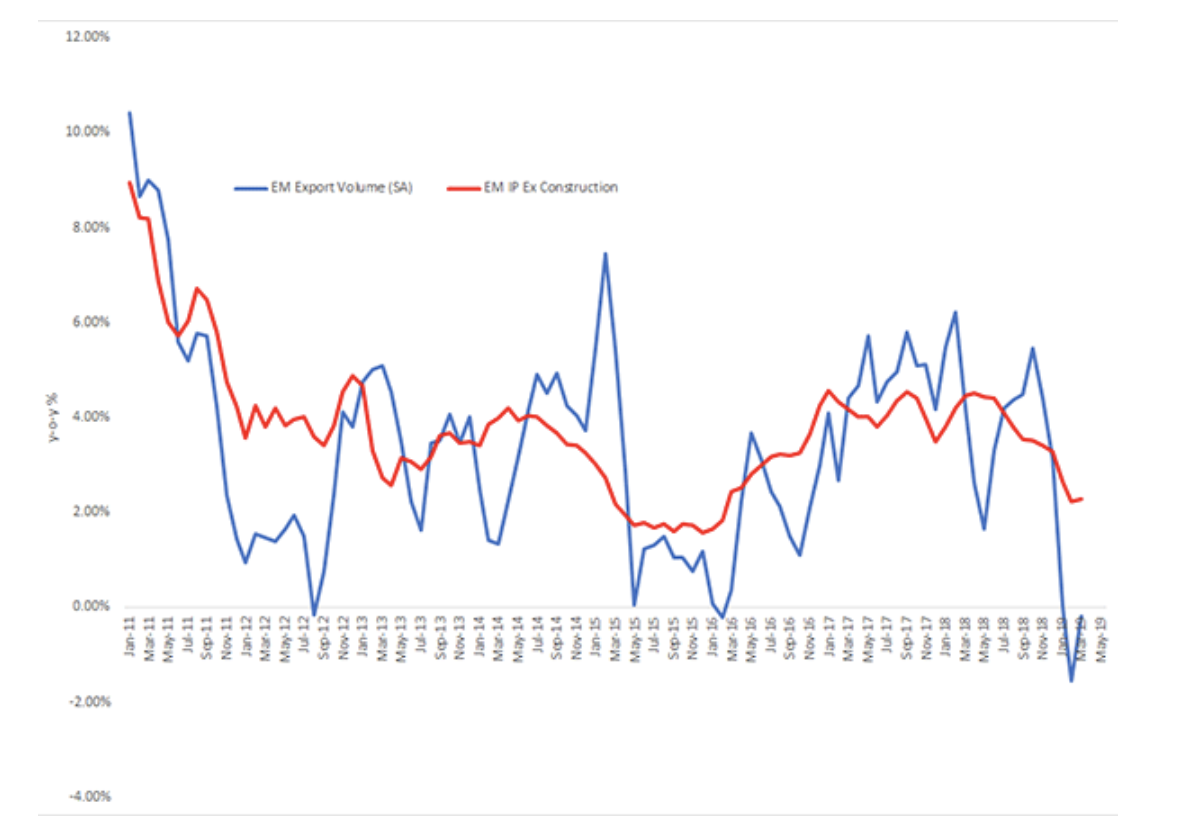

Thus far, the visible impact on EMs has been mostly through the trade channel, with export volumes and industrial production declining significantly (Figure 1). This is despite the sizable front-loading of exports from China to the US to avoid impending tariffs, and trade diversion beginning to manifest in the data, especially in electronics exports to the US from Asia ex-China and agricultural exports from Latin America to China. First quarter growth data also confirmed the weakening trend within EMs (excluding China and the two crises economies of Turkey and Argentina) accounting for one third of the 0.6 percentage point year-over-year decline in global growth.3

Figure 1: EM exports and industrial production

Source: CPB Netherlands Bureau for Economic Policy Analysis and Haver Analytics Inc. as of June 17, 2019

Open economies in Europe and Japan have also seen significant weakness in trade and manufacturing. An important driver of this trend has been the decline in import demand from China. However, the slowdown in China was evident even prior to the trade dispute and is part of a secular trend which we expect to continue as China transitions from the excesses of the post-crisis era to a more sustainable and lower growth rate.

Various estimates had put the direct impact of current tariffs on China in the range of 0.2 to 0.4 percentage points of gross domestic product (GDP) for 2019-2020.4 We forecast that an escalation of tariffs to all Chinese exports could increase this number to 1.2-1.5 percentage points of GDP. However, we expect China’s ongoing fiscal stimulus to mitigate some of this impact, limiting the negative spillover to the rest of EM. Should tensions escalate further, we would expect additional easing from China to support growth at about 6% through 2020.

What’s been the impact on developed markets?

The impact of the tariffs on the US economy thus far has been limited, but this is because the size and composition of the initial tariffs were calibrated to minimize their impact. However, if the coverage of goods affected by tariffs were to expand to consumer goods, we estimate that the impact on growth could be in the range of 0.4-1 percentage point of GDP and 50 basis points on inflation. The indirect effects on financial markets would likely be stronger and require a strong policy response from the Federal Reserve and global central banks.

One saving grace thus far has been resilient labor markets in developed markets and improved balance sheets since the global financial crisis. This resilience shows up in the consumption and services sectors, key drivers of global demand. However, if trade tensions escalate further, manufacturing weakness could spill over to labor markets and the services sector, potentially undermining global demand.

Our outlook

Going forward, the Global Debt Team sees the bigger risk to global EM growth coming from uncertainty. In a globalized production system, policy uncertainty is bound to weigh on business and consumer sentiment and investment plans. Although it is impossible to model these linkages, soft data already point to a weaker capital expenditure outlook globally, and survey data indicate corporate plans to relocate production.5 In the first quarter, investment weakness was evident across most EMs, especially in Asia.

Until a trade deal can be reached, these concerns tilt the risks to global economy firmly to the downside for 2019-2020, in our team’s view. Weak global demand, led by lower exports and investment and weaker commodity prices, does not bode well for the EM growth outlook.

On the positive side, we see room for more policy action from EM central banks. The pivot in Fed policy since September 2018 has already ensured benign global financial conditions and allowed several EM central banks to deliver some monetary easing. Widening output gaps and the absence of demand-led inflation pressures allow further room for EM central banks to ease,6especially, considering the continued dovish tone from major global central banks. We think this should help mitigate some of the risks to EM growth.

1 The US has used various trade status, such as Section 232 on national security or Section 301 on discriminatory measures and national emergencies to justify various recent policy actions. Investment reviews and export control frameworks for critical high-technology sectors are also part of the tool kit. Huawei and ZTE are two recent examples of export bans. China on the other hand created an “Unreliable Entities List” of foreign entities that threaten Chinese companies’ interests.

2 Relocation of supply chains is not likely to be seamless, vary across product groups and would take time. Nonetheless, ASEAN, Korea and Taiwan stand out as potential winners from a reallocation of supply chains as well as Mexico. Brazil could also potentially benefit from higher agricultural exports to the US.

3 Our global GDP series covers about 89% of the global economy using the International Monetary Fund’s purchasing power parity weights.

4 Source: Bloomberg Economics, 2018.

5 Source: Source: USB CFO survey, 2019.

6 Source: Except for some Central and Eastern European countries where output gaps have been closed for some time and inflation pressures are evident.

Important information

Blog header image: Dominik Vanyi/unsplash.com

The opinions referenced above are those of the author as of June 25, 2019. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

An investment in emerging market countries carries greater risks compared to more developed economies.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Meral Karasulu, PhD

Meral Karasulu is Director of Fixed Income Research for the Global Debt team, covering emerging economies in the Asia-Pacific and Central and Eastern Europe regions.

Ms. Karasulu joined Invesco when the firm combined with OppenheimerFunds in 2019. Prior to joining the OppenheimerFunds in 2015, she worked at the International Monetary Fund (IMF), where she served in a number of capacities over her 17-year tenure. In her last role at the IMF, she served as a deputy division chief in the Asia Pacific department. Over the course of her tenure, Ms. Karasulu has covered a range of advanced, emerging and frontier markets including Korea, Australia, Chile, Germany, Netherlands, Mongolia, Myanmar, and Cambodia, focusing on macroeconomic and financial sector issues.

Ms. Karasulu earned a BA degree in economics from Bosphorus University, Turkey, and a PhD in economics, with a specialty in international macroeconomics and econometric theory, from Boston College.

Read more articles by Meral Karasulu