Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In this article I critique the logic and math used by the finance industry to support their asset location advice. It is not so much their conclusions I care about, as how they get there. I present a list of arguments commonly used, why they are wrong, and some issues that are never discussed.

Tax shelters, such as Roth IRAs and 401(k)s, exist to reduce the taxes you pay. Their benefit can be measured as the difference in outcomes compared to a taxable account. The objective of asset location is to maximise that benefit by choosing which asset to hold in which account. To that end it is necessary first to agree with the net benefits of traditional 401(k) and IRA (which I will refer to as “TRAD”) accounts, as I argued in How to Properly Frame 401(k) Benefits. Contrary to the industry’s belief, their universal benefit comes from permanently sheltering profits from tax. There is also a possible bonus (or penalty) from withdrawals at tax rates lower (or higher) than at contribution. No one disputes that the net benefit of Roth accounts comes from permanently sheltering profits from tax.

1. There is a near universal conceptual model of TRAD accounts, which has profits taxed on withdrawal at full (ordinary income) rates (e.g., see here). This mistaken understanding results in location advice to keep stocks (paying dividends and capital gains that would otherwise be preferentially taxed) out of TRAD accounts, even if that means using a taxable account.

But the tax on withdrawals from TRAD accounts is an allocation of capital between the account’s ‘owners,’ not a tax on profits. Assuming no bonus or penalty from a change in tax rates, the outcomes of TRAD and Roth accounts are equal. The benefits from profit sheltering are equal, regardless if the profits are interest, dividends or capital gains.

2. Another decision rule says volatile stocks should be kept in taxable accounts because the tax benefit from capital losses is lost in tax-shelters (e.g., see here). But in taxable accounts, only net capital gains over time are taxed – gains less losses. In tax-shelters as well, only net profits over time are tax-free. Losses are treated equally in all accounts. And no one invests with the presumption that they will lose money over time.

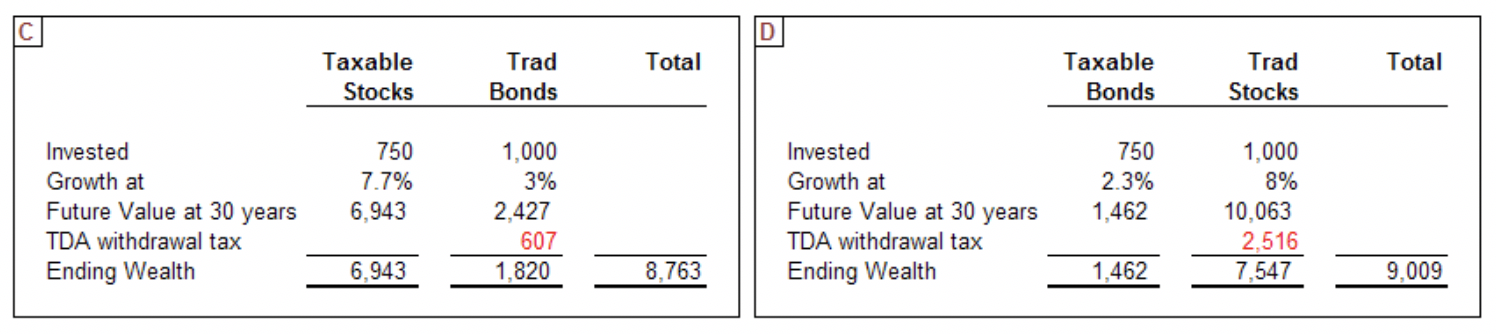

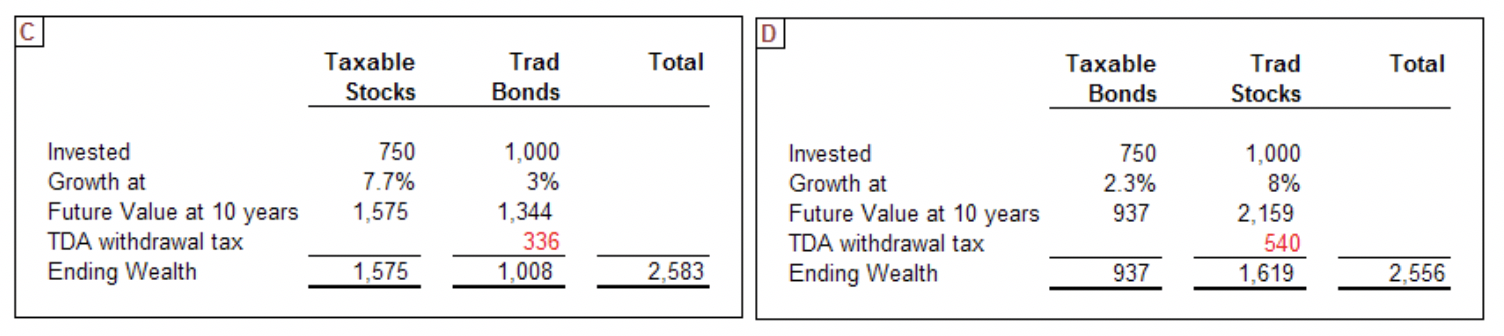

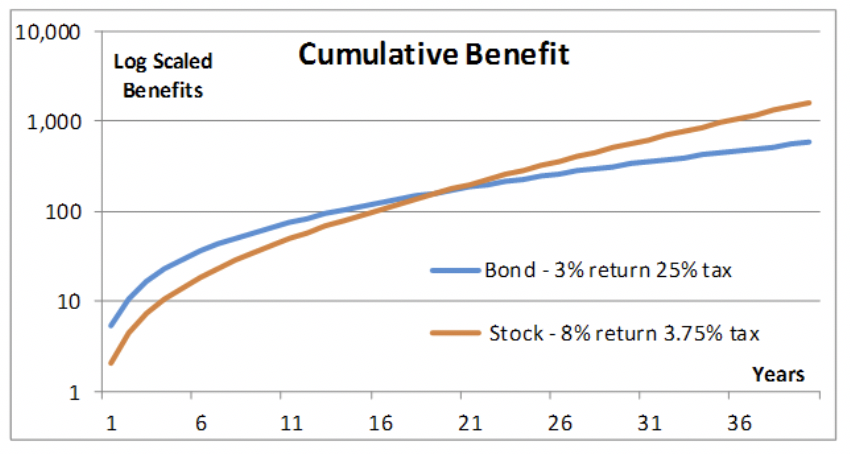

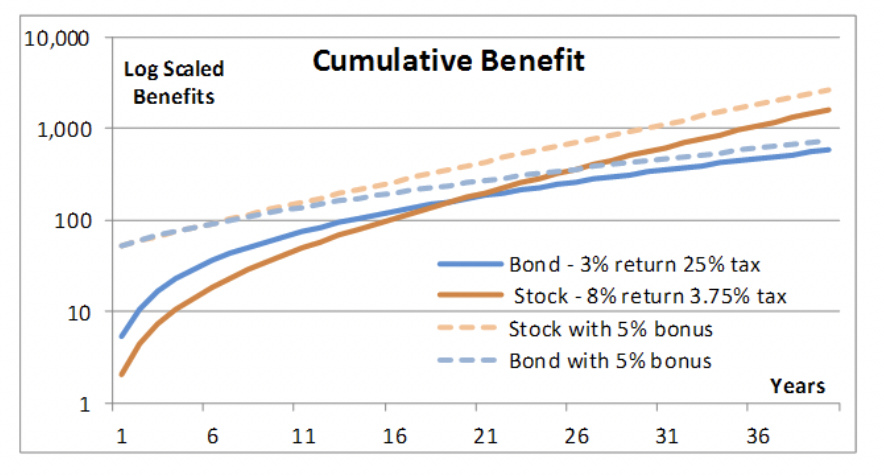

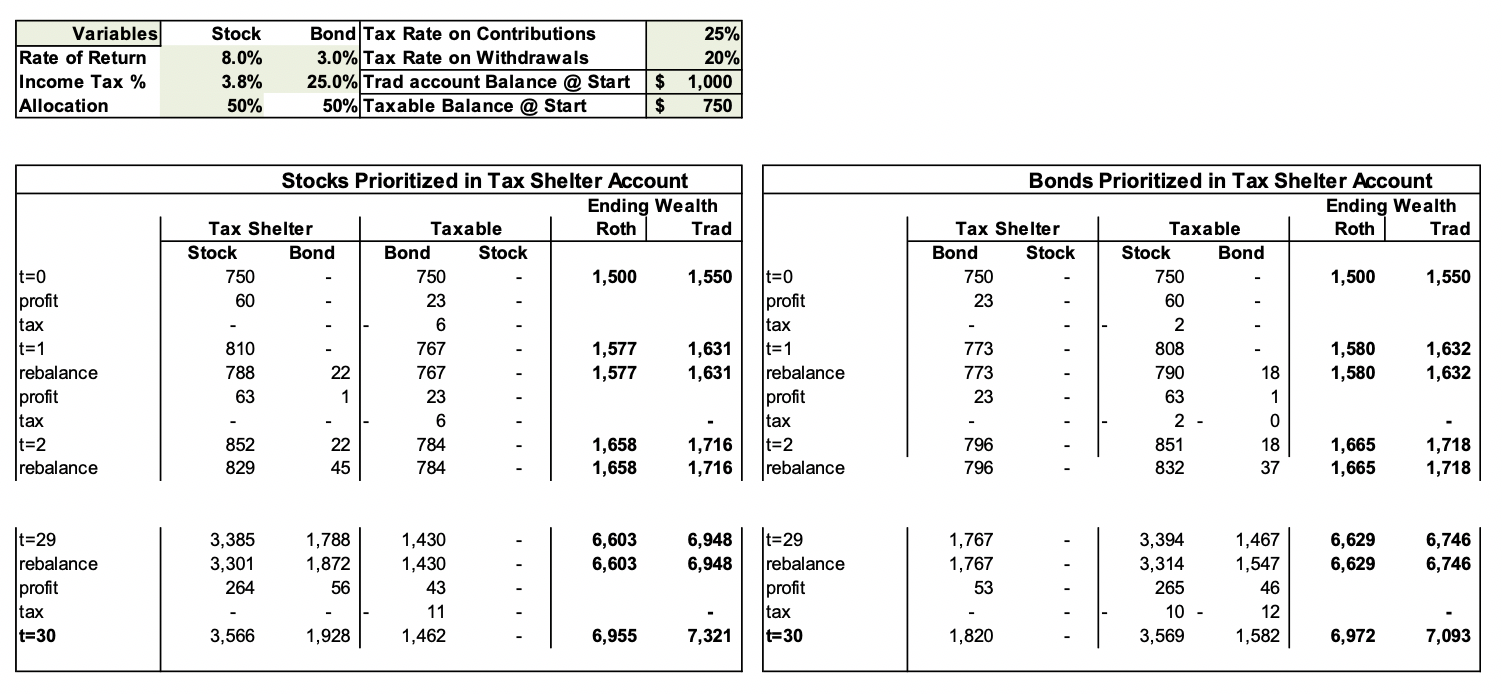

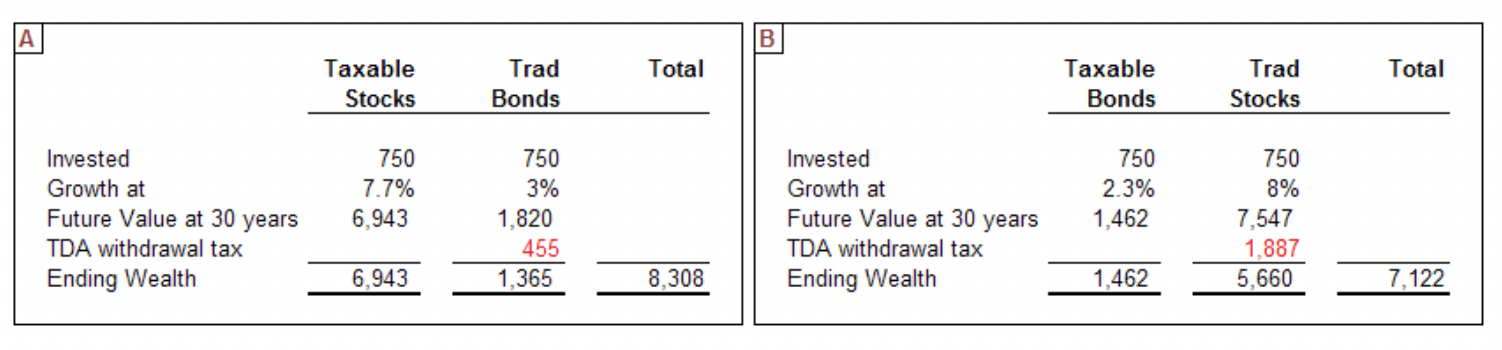

3. Many (e.g., see here) asset locate the dollars sitting in any account as if they were of equal value. They ignore the reality that before-tax dollars are worth less than after-tax dollars. Their analysis of asset location looks like examples A and B below. Bonds earn 3% and are taxed at 25%. Stocks earn 8%, taxed at 3.75% (15% tax on 2% dividends; 0% taxed capital gain). If you believe $750 = $750 regardless, then their conclusion that bonds are better than stocks in TRAD accounts is justified by example A’s better outcome (versus the opposite asset location in example B).

But when the tax rate is 25%, a TRAD account must have $1,000 to equal $750 in a taxed account. The asset location conclusion reverses when you model equal values for each asset allocation. Below, stocks in the TRAD account show a better outcome (D versus C). How you equate the value of dollars matters.