As the chief research officer for the Buckingham Family of Financial Services, one of the issues I’m asked about more and more is the underperformance of U.S. value stocks over the last decade. The main concern I hear is that the underperformance is a result of the trade becoming overcrowded post-publication of the academic findings demonstrating a significant value premium around the globe as well as across asset classes.

We can address the issue of overcrowding by examining the spreads in valuations of growth and value stocks. If overcrowding has occurred, we should see a dramatic narrowing in valuations.

Have spreads narrowed?

We can measure the spread in valuations by using data from Ken French’s data library. The data is based on a 2-by-3 matrix, splitting the market into large (top 50%) and small (bottom 50%); and value (cheapest 30%), core (middle 40%) and growth (most expensive 30%). The portfolios include utilities and financials and use a weighted average market cap.

At the end of 1993, right after the publication of the original famous Fama-French research on the size and value premiums, the price-to-book (P/B) of U.S. large growth stocks was 4.4 times that of U.S. large value stocks, and the ratio of their price-to-earnings (P/E) was 3.1 times. If there was overcrowding, we should see narrowing of the spreads, as cash flowing into value stocks and out of growth stocks impacts relative prices.

Contrary to the conventional wisdom that would theorize the spread had narrowed, we find that at the end of 2018, the P/B ratio had widened from 4.4 to 5.4 (a relative increase of 23%), and the P/E ratio had widened from 3.1 to 5.0 (a relative increase of 61%). Turning to small stocks we see similar evidence.

At the end of 1993, the P/B of U.S. small growth stocks was 5.4 times that of U.S. small value stocks, and the ratio of their P/Es was 4.2. At the end of 2018, the P/B ratio had widened from 5.4 to 5.9 (a relative increase of 9%), and the P/E ratio had widened from 4.2 to 6.1 (a relative increase of 45%).

The year-to-date underperformance of U.S. value stocks, both large and small, in 2019 would indicate that, if anything, the spreads may have widened a bit further since December. The bottom line is that we see no evidence that cash flows have caused the ex-ante value premium to narrow, either in small stocks or large stocks.

Let’s turn now to the issue of whether valuation spreads matter. We’ll look at three studies that address the issue.

Valuations matter

Adam Zaremba and Mehmet Umutlu, authors of the March 2019 study “Strategies Can Be Expensive Too! The Value Spread and Asset Allocation in Global Equity Markets,” examined whether the value spread (the difference in valuation ratios between the long and the short sides of the trade) was useful for forecasting returns on quantitative equity strategies for country selection. To test this, they examined a sample of 120 country-level equity strategies replicated within 72 stock markets for the years 1996 through 2017. They found: “The breadth of the value spread can predict the future returns in the cross-section. We show that equity strategies with a wide value spread markedly outperform strategies with a narrow value spread. In other words, if you wonder which strategy might produce decent payoffs in the future, pay attention to the value spread.”

Their findings are consistent with prior research. For example, the February 2018 study “Value Timing: Risk and Return Across Asset Classes,” by Fahiz Baba Yara, Martijn Boons and Andrea Tamoni, also found that valuation spreads provide information. The authors demonstrated that “Returns to value strategies in individual equities, commodities, currencies, global government bonds and stock indexes are predictable by the value spread. … In all asset classes, a standard deviation increase in the value spread predicts an increase in expected value return in the same order of magnitude (or more) as the unconditional value premium.”

Jim Davis’ 2007 study, “Does Predicting the Value Premium Earn Abnormal Returns?” also found that book-to-market ratio spreads contain information regarding future returns. However, he also found that style-timing rules did not generate high average returns because the signals are “too noisy” – they don’t provide enough information to offer a profitable timing signal. Confirming Davis’ findings, AQR’s research into style-timing rules led them to conclude that they increase turnover and trading costs, making them even less effective for implementation.

Valuations matter. With that in mind, let’s take a look at how current relative valuations compare to where they were when the growth bubble burst in early 2000.

Revisiting the bursting of the bubble

At the end of 1993, the ratio of the P/B of U.S. large growth stocks to the P/B of U.S. large value stocks was 4.4. By the end of 1999, the ratio had widened to 6.9 – versus 5.4 at the end of 2018. For large value stocks, the spread, while wider than it was at the end of 1993, is well below that of the level reached at the end of 1999. The ratio of the P/B of U.S. small growth stocks to U.S. small value stocks had widened from 5.4 in 1993 to 5.9 at the end of 1999 – the same figure it was at the end of 2018.

When we look at the ratio of P/Es, we see that for large stocks they widened from 3.1 at the end of 1993 to 5.2 at the end of 1999. It was almost as high at 5.0 at the end of 2018. For small stocks, the ratio of P/Es widened from 4.2 at the end of 1993 to 5.1 at the end of 1999. At the end of 2018, it was much wider at 6.1.

Summarizing, comparing relative valuations at the end of 2018 to those at the end of 1999, we find that, with the exception of the still-wide gap in the P/B of large growth stocks, the rest of the ratios look similar, with (in terms of P/E) small growth being relatively far more expensive (with a ratio of 6.1versus 5.1) than it was just before the growth bubble burst in 2000.

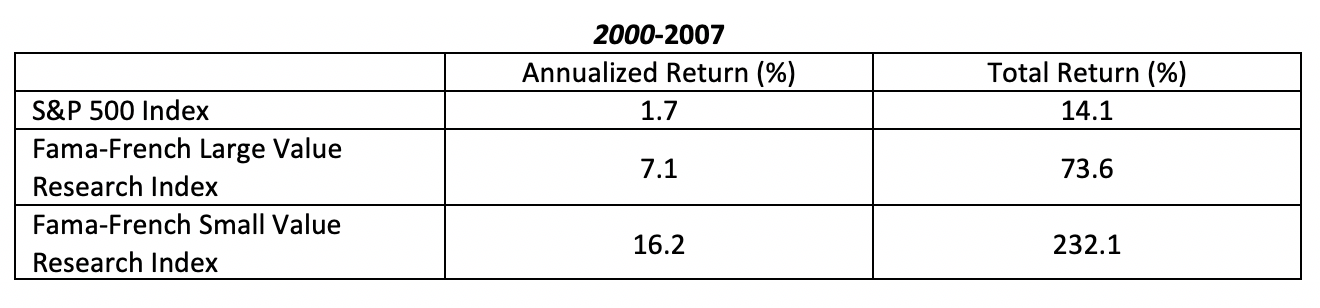

With that in mind, let’s review how value performed in the eight years following the bursting of the bubble. Using data from Ken French’s data library, as the table below demonstrates, large value and small value outperformed by a cumulative 60% and 218%, respectively.

Summary

For value investors, the above findings are good news, as the relatively poor performance of value stocks in the U.S. over the past decade has led to a widening of the P/B and P/E spreads between value and growth stocks. Unfortunately, while it does inform us that the ex-ante value premium is now larger than it was in 1993, and perhaps similar to what it was at the end of 1999, sadly, as Jim Davis noted, there’s little evidence that the information can be used to time entry and exit into value stocks. In other words, the underperformance of value stocks can continue, perhaps even for a long time.

The same thing is true about using valuations to time entry and exit into the overall equity market. While the CAPE 10 does provide us with information on future returns (higher valuations forecast lower expected returns), that information cannot be used to time markets.

Because markets can remain “irrational” longer than the ability of most investors to stay disciplined, adhering to your asset allocation plan and ignoring recent performance – understanding that all risk assets undergo very long periods of underperformance – is one key to successful investing. It is why Warren Buffett warned that, when it comes to investing, temperament is far more important than intelligence. Investors need to accept that the historical evidence demonstrates that even 10 or 20 years of underperformance are likely for all risk assets. If you doubt that, consider the following.

- Over the 40-year period 1969-2008, U.S. large and small growth stocks (Fama-French research indexes) returned 8.5% and 4.7%, respectively, underperforming the 8.9% return of long-term (20-year) Treasuries. Over this same period, U.S. large and small value stocks returned 11.6% and 14.5%, respectively, far outperforming the return of long-term Treasuries, and demonstrating the benefits of diversification.

- Over the 49-year period 1970-2018, Japanese large stocks returned 8.6%. However, over the 29-year period from 1990 through 2018, their total return was -0.03%! That’s almost 30 years with no return for the risks of equity investing. It’s another example of why diversification of risk is so important.

If you cannot tolerate volatility, use a different strategy. However, doing so means you sacrifice the benefits of diversification (the only free lunch in investing, which is why you should eat as much of it as you can get) and ex-ante risk premiums.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 130 independent registered investment advisors throughout the country.

More ETF Topics >