Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

You’re a financial adviser, not a retirement lifestyle coach.People seek your expertise to solve their financial challenges. You routinely provide valuable retirement planning advice about topics such as how to pay down debt, reduce taxes, invest money, manage retirement income sources, and demystify estate planning matters.

But there is an overarching retirement planning question that goes unanswered or is never brought up during an adviser-client meeting.

The great, unanswered question

Financial planning technology has advanced our profession significantly over the past couple of decades. Advisors have easy access to professional tools to help their clients answer the most important financial question of their lifetimes: How do I ensure that I don’t run out of money?

But the question that is often ignored or answered superficially deals with your personal identity in retirement: What am I going to be after I no longer do what I used to do for a living?

Those contemplating their retirement years think about this question, but few actually seek a definitive answer beyond doing activities.

I am what I do

Personal character is frequently associated with work identity. When I listen to career-focused people introduce themselves and explain who they are, they invariably offer up their job title or an explanation of what they do. After years of being what they do for a living, they anticipate their inevitable retirement date with no clue what their new purpose will be after they separate from their work environment and related social circles. Consequently, a personal identity crisis begins once work identity is abandoned without a sufficient substitute to replace it.

A retirement lifestyle defined only by what one does (say, replacing work responsibilities with leisure activities), without including a redefined sense of purpose, does not fully answer the “what will I be, now that I’m not” question.

Be, do, have

When I was an active financial planner, I asked clients this question: “What do you want to be, do, and have when you retire?”

Answers varied, but mostly clients responded like this: “I want to be retired before ____ age; I want to do things like play golf, hang with friends, and travel; and I want to have enough money to remain financially independent for my retired lifetime.”

Aside from the financial aspects of making the financial independence goal happen, I always felt like my clients needed additional help in providing more thoughtful answers to my questions about their retirement lifestyle goals. Specifically, they needed to address what would be their new purpose in all areas of their lives after employment ended or was altered.

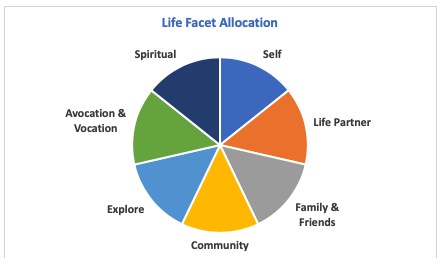

Most people are surprised to learn there are seven life facets in retirement to consider.

Life facet allocation

As a planning tool to help clients provide more thoughtful answers to the “be, do, and have” lifestyle questions, I created an exercise that includes a pie chart similar to an asset allocation diagram. Instead of labeling the slices of the pie with growth, income and cash assets, the model life facet allocation pie has seven areas that make up a retirement lifestyle.

Examining each slice, an advisor can ask the client this: What will you be (new purpose) to the people and situations in each area of your life? Then ask this: What will you do (tasks) to affirm your purpose or identity for each facet? Finally, ask this: What will you have (life experiences) as a result? Worksheets for this simple but effective retirement lifestyle planning exercise are included in my e-book called, You Vision. It can be downloaded for free here.

A conversation begun is better than none

Depending on your client’s identity needs, the life facet allocation exercise can serve as the retirement lifestyle component of a larger financial plan or as a conversation starter that leads to a more comprehensive lifestyle study with the aid of a retirement lifestyle coach or counselor.

Either way, focusing your clients on who they will be in retirement in addition to what they will do can begin a more meaningful conversation about defining new and exciting purposes in a multifaceted retirement lifestyle.

As your client’s lifetime financial advisor, no one is better qualified to introduce a retirement lifestyle planning exercise than you. For financial advisors who don’t want to pursue life planning certification or other degreed programs focusing on the psychology of finding purpose in life, the basic exercise outlined here and found in my e-book, You Vision, will help.

Jim Collier is the author of the recently published book, Retirement Is Recess for Grown-Ups, available at the link here. He is the founder of RetirED LLC, a nonaffiliated retire-ready resource company located in Larkspur, Colorado. Prior to becoming a full-time author, Jim was a Certified Financial Planner and owner of Collier Financial Inc. for 32 years before completing a business succession with his son in 2017. Jim writes and speaks about contemporary retirement lifestyle and business succession planning topics for groups and conferences.

For more information, visit www.retirementrecess.com or email Jim at [email protected].

More Fixed Income Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.