Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Recently, much has been written about the corporate debt market and how it has grown since the financial crisis. While consumer debt has declined markedly since that time, the same has not been true of corporate America. In a recent speech, former Fed Chair Janet Yellen spoke about the “high levels of corporate leverage” and the potential for “lots of bankruptcies” in the $9.1 trillion-dollar corporate market if the economy turns down.

Nearly every broad fixed income strategy, whether executed in mutual funds, ETFs, or separately managed accounts, has a significant exposure to corporate bonds. In fact, corporate bonds now compose a larger part of the overall fixed income market than a few years ago, as issuance has exploded. Another byproduct of issuance patterns is the portion of BBB-rated companies that have come to market in the last several years, which has increased the exposure of these types of credits in passive strategies/indices. In addition, many companies issuing debt felt comfortable being in the space, as they engineered their balance sheets to ‘BBB’ metrics and often used their financings to buy back their stock in an effort to boost equity returns. The market of the last decade penalized companies very little for this behavior to be in this ratings space.

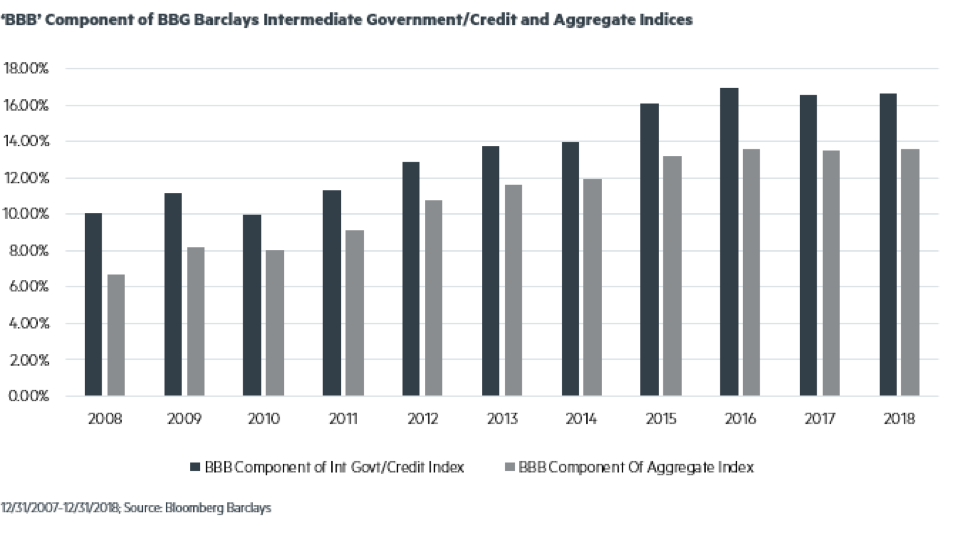

As seen below, the Bloomberg Barclays Intermediate Government/Credit Index contained nearly 17% in BBB-rated exposure in 2018 compared to approximately 10% a decade ago. Similarly, the BBB-rated portion of the Bloomberg Barclays US Aggregate Bond Index nearly doubled between 2008 and 2018. The Bloomberg Barclays broad corporate bond index contains approximately 50% BBB-rated bonds.

While the evidence of quality creep is clear in the indices, many active strategies have also drifted lower in quality as the reach for yield was in full swing during the period of ultra-low rates. We believe that many active strategies, and certainly passive ones in the investment-grade space, have raised their BBB exposures, which has also increased their correlation to equities. This is not a positive development, since many investors expect their bond portfolios to have low correlations to their equity exposures. In other words, there is a stealth decline in the credit quality of the overall investment-grade corporate bond market.