At 1:30pm ET on March 13, the next-to-last paragraph was corrected to read, “Approximately 55% of BBB-rated bonds…” It previously read, “Approximately 55% of high-yield bonds…”

At 1:30pm ET on March 13, the next-to-last paragraph was corrected to read, “Approximately 55% of BBB-rated bonds…” It previously read, “Approximately 55% of high-yield bonds…”

When Donald Trump was campaigning, he said he would eliminate the national debt in eight years. But it has increased by $2 trillion in the first two years of his presidency, leading Jeffrey Gundlach to conclude that we are “on the road to a large debt problem.”

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital. He spoke via a webcast with investors on March 12. His talk was titled, “Highway to Hell,” and the focus was on his firm’s flagship mutual fund, the DoubleLine Total Return Fund (DBLTX). The slides from his presentation are available here.

Highway to Hell is a 1979 song from the rock group AC/DC. Gundlach said it illustrates the perdition that awaits the U.S. economy if policymakers continue to allow an unchecked growth of federal deficits.

Deficit warnings have been a common theme in Gundlach’s webcasts. In 2011 and 2012 he warned that harmful effects – specifically high interest rates – would come by the end of the decade. We are on schedule, he said, and unless the Fed takes drastic action, that fate awaits our markets.

But a spike in interest rates is not certain, he said. The Fed has demonstrated that it can take drastic action and can quickly adapt to evolving market conditions.

The Fed’s attitude changed 180 degrees since December, when it said its quantitative tightening (QT) was on “autopilot,” reducing the balance sheet by $50 billion/month. Now, Gundlach said, a plan is being discussed to stop QT by the end of the year, which will eliminate about a third of the planned balance-sheet reduction.

The markets rebounded as a result of the Fed’s about face, Gundlach said. Now central banks are talking about using quantitative easing (QE) as a regular policy tool against weakening economies.

Indeed, he said, the narrative has turned to a coordinated slowdown, as economic data across the globe has been disappointing, with metrics below their 12-month averages. Some emerging markets are “okay,” Gundlach said, including Brazil, Peru and Uruguay, but globally “it is flashing red. Global data changes are the worst they have been in seven years.”

That slowdown has been driven by the falloff in global trade, according to Gundlach. That contraction is similar to the lead up to the two last recessions, and the next one, he said, could be a year or two away.

Forecasting the next U.S. recession

Gundlach’s primary recessionary signal is the Conference Board leading economic indicators, which he said are falling sharply, “but from a very high level.” They are still positive, which means they are not a precursor to a recession. “There is nothing imminent forecasting a recession,” he said, “but possibly in 2020.”

The job market is tight, he said, and wage growth could approach 4%. “That could change the psyche of investors,” he said, raising inflation expectations. The Fed has said it would not be concerned if inflation goes above 2%, and Gundlach said that 2% could become a “floor,” instead of a trigger for policy adjustments. “The Fed wants investors to be more comfortable with inflation approaching 3%,” Gundlach said.

Consumer confidence rebounded with this year’s uptick in the stock market, Gundlach said. The Conference Board consumer expectation metric is at 131, one of its highest readings ever. One of the most important things to watch are real-time consumer expectations, he said. “If those start to drop, it would be a strong signal of an impending recession.”

The National Federation of Independent Business (NFIB) planned hiring data “rolled over,” Gundlach said, which is troubling, as are retail sales data. Six-month retail sales were down 1.6% in December, the worst one-month decline since the global financial crisis.

Gundlach highlighted one anecdote. There are more $100 bills than $1 bills in circulation. But 20 years ago the number of $1 bills was double the $100 bills. If there is no inflation, he asked rhetorically, why do we need so many 100 bills? His conjecture was that people have a greater need to move large amounts of cash quickly.

The highway to hell

Gundlach cited an array of figures with a common theme: the buildup of public- and private-sector debt.

The federal government has shown an increasing willingness to use “off budget” financing, he said, which includes financing for the military, disaster relief and “phony loans for Social Security.” The economy is growing at a real rate of 3.1%, but we have a budget deficit typical of those in recessions, he said.

He referred to the national debt, which includes deficits that are financed by bond issuance as well as intragovernmental loans, such as those used to finance Social Security. The national debt is $22.13 trillion, he said, and growing at about $1.5 trillion/year. Gundlach calculated that we would need 10% of GDP to pay back the national debt, and at that it would take the next 60 years.

Private-sector mortgage debt has not grown since the financial crisis, he said. But corporate and Treasury debt have had an “incredible increase.” Those three sources of debt now comprise 210% of GDP, according to Gundlach.

“We have insufficient taxation or excessive spending,” Gundlach said.

Taxation as a percent of GDP is at its lowest since 1950, he said, yet spending as a percentage of GDP is growing. If we fund the Green New Deal the way we financed World War II, as some have advocated, it would be accompanied by a big increase in taxes, Gundlach said, “more than could be financed by a wealth tax or a tax on the upper 1%.”

Entitlements and mandatory spending are two thirds of the budget and are rising rapidly, he said, and will continue to do so given our demographics.

But fewer people care about the deficit, Gundlach said, based on a poll of whether Americans should make deficit reduction a priority. This was especially true among Republicans.

“People don’t care about the deficit anymore,” Gundlach said, “but that will change at some point.”

Deficits have increased substantially during recessions and Gundlach predicted that long-term rates will go up in the next recession. But there is one way the Fed could avert a spike in rates. It could follow the policies adopted by the Bank of Japan and, to a lesser degree, the European Central Bank. Those central banks have “monetized” debt, using their own funds to purchase bonds in the open market. Interest rates in Japan and parts of Europe are near 0%.

The federal deficit could rise to 8% of GDP in a recession, based on historical averages, Gundlach said. That would translate to a $2.7 trillion deficit and a $4 trillion increase in the national debt, he said, “in a year when the economy is not growing.”

As an aside, Gundlach said that individuals need a 43% debt-to-income ratio to get a government guaranteed mortgage. The corresponding ratio is 537% for the U.S. government, which Gundlach acknowledged has its own currency that it can print.

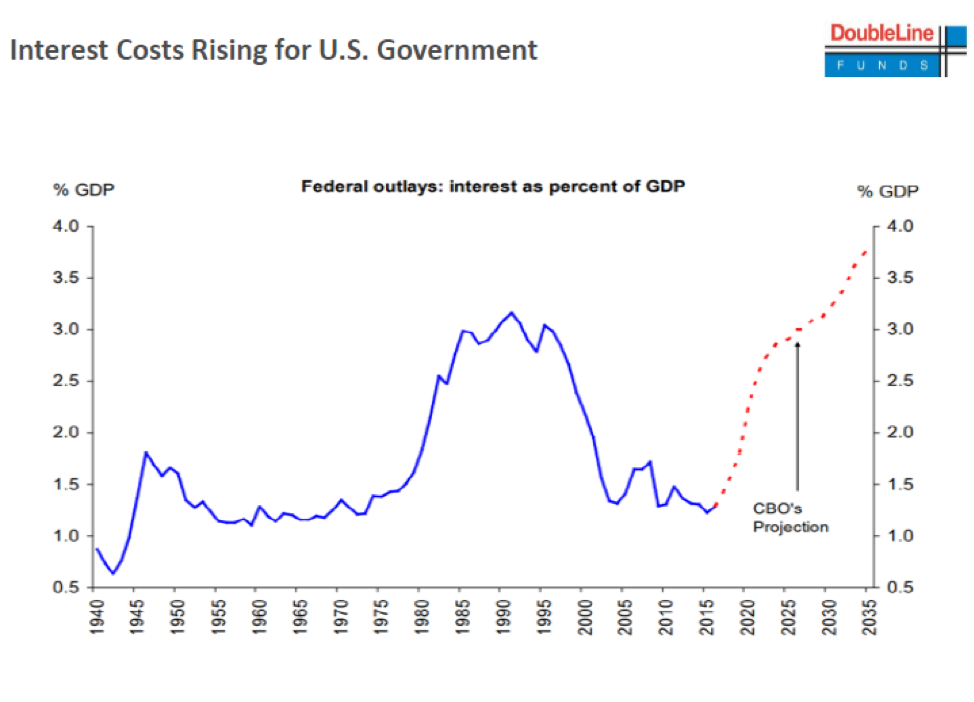

One impending problem is that the interest expense is projected by the congressional budget office (CBO) to “explode higher, starting yesterday,” Gundlach said. The overdue rise in interest expense is shown in the graph below:

But interest expense hasn’t risen in the last 15 years – because, he said, “it takes time.” The CBO projections assume no recessions, which will reduce GDP and lower tax revenues. Because of the increased interest expense, “we will be challenged to have any real GDP growth at all,” Gundlach said, “and that is without a recession.”

“The Fed could be forced into a massive QE program,” he said, “otherwise I am not sure who will buy those bonds.”

A crackpot idea

Gundlach dismissed modern monetary theory (MMT) as a “crackpot idea.” He said it was based on the tenuous assumption that, as long as nominal GDP growth is less than the 10-year yield, it is okay to borrow. The problem, according to Gundlach, is what happens when the economy turns down. What about the existing stock of debt?

He said he was “horrified” by the ex-CEOs and independent trustees of mutual funds that had publicly supported MMT. “That is detrimental to the world of finance,” he said.

MMT is a way of monetizing the debt, he said, that would lead to a “boycott of long-term bonds until there is a response to what will be a frightening scenario.”

Investment recommendations

The trade deficit has expanded and the deficit in traded goods (as opposed to services) is at an all-time record, despite Trump’s campaign promises to reduce the trade deficit. The trade and budget deficits correlate to the dollar, he said, which weakens when they expand. “You should be a dollar bear for the long term,” he said. That would be good for emerging markets, which did well in the fourth quarter of 2018, despite dollar strength during that period.

His number-one recommendation is emerging market equities. He said investors should be at their maximum emerging market exposure within their overall equity exposure (not necessarily their maximum equity exposure).

He said the dollar will weaken because the expectation is for dovish policy from the Fed, particularly over the next one to two years.

“The next big move will be lower on the dollar,” he said, “which will be good for commodities and gold.”

As in his prior couple of webcasts, Gundlach said to avoid corporate debt.

Half of investment-grade bonds are rated BBB, he said, and those bonds face a “wall” of maturities between now and 2021. The BBB market is 2.5-times bigger than the high-yield market. It is “mis-rated,” he said, and “risky if there is a recession.”

Approximately 55% of BBB-rated bonds would be rated junk based on the leverage ratio of the underlying corporations, according to Gundlach. This is because the rating agencies use other criteria, he said, but leverage ratios should be a “fundamental starting point.” The bonds will get there in the next recession, Gundlach predicted.

Downgrades would mean a reduction in bond prices. He said the same happened in 2002 and 2003, and “it will be much worse now because the size of the bond market is much bigger.”

More Fixed Income Topics >

At 1:30pm ET on March 13, the next-to-last paragraph was corrected to read, “Approximately 55% of BBB-rated bonds…” It previously read, “Approximately 55% of high-yield bonds…”

At 1:30pm ET on March 13, the next-to-last paragraph was corrected to read, “Approximately 55% of BBB-rated bonds…” It previously read, “Approximately 55% of high-yield bonds…”