Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Only humans have the capacity to think ahead and plan for the future. My favorite plans are the ones that the lunkheads on It's Always Sunny in Philadelphia come up with each week. I love these plans for one reason – they are creative. They never work, of course, but at least they are willing to try something original. And crazy. And entertaining. For them, hope springs eternal even if their plans involve great bodily harm and widespread ridicule.

What the research says about planning

A groundbreaking study in 2006 by Annamaria Lusardi and Olivia S. Mitchell found that investors who have taken the time to do some planning, even a little bit, ended up with two- to three-times more money at retirement than investors who didn't do any planning.

Most working Americans will end up with about $200,000 in their IRA or 401(k) accounts at retirement. But those who take the time to develop a plan will end up with $400,000 or $600,000.

Lusardi & Mitchell asked respondents to discuss what they do to calculate their retirement-saving needs. They asked whether people ever assessed those needs, but also what followed from such assessment. The data they collected about retirement planning calculations were as follows:

|

Question |

|||||

|

Have you ever tried to figure out how much your household would need to save for retirement? |

Yes 31.3% |

No 67.8% |

Don’t know 0.9% |

||

|

Did you develop a plan for retirement saving? |

Yes 58.4% |

More or less 9.0% |

No 32.0% |

Don’t know 0.6% |

|

|

How often were you able to stick to this plan? : Would you say always, mostly, rarely, or never? |

Always 37.7% |

Mostly 50.0% |

Rarely 8.0% |

Never 2.6% |

Don't Know 1.0% |

|

Finally, what planning tools do you rely on to devise and carry out your plan? |

Online retirement calculator 33.8% |

Retirement expenses worksheet 23.6% |

Rely on advisor tools 19.4% |

None 18.8% |

Don’t Know 4.4% |

Where do investors get their planning advice?

The researchers also tried to assess what planning tools people rely on to devise and carry out their retirement-saving plans. Specifically, they inquired whether respondents contacted friends, relatives or experts, and whether they used retirement calculators. In addition, they asked whether respondents tracked their spending and set spending budgets. The specific question phrasing were as follows:

- Tell me about the ways you tried to figure out how much your household would need at retirement.

- Did you talk to family and relatives?

- Did you talk to co-workers or friends?

- Did you consult a financial planner or advisor or an accountant or lawyer?

- Did you read articles about retirement planning in magazines or newspapers or online media?

- Did you mostly rely on information sent to you in the mail, unsolicited?

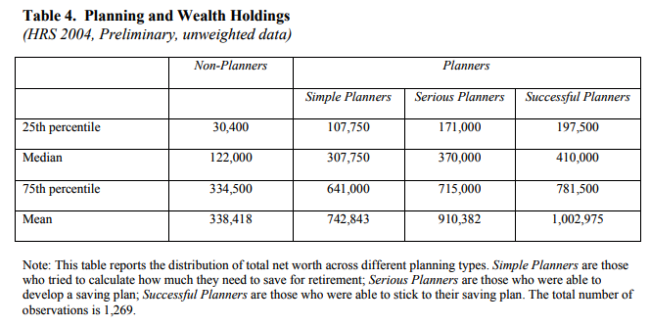

The table below summarizes the amount of wealth accumulated by planners and non-planners: