How Paul Volcker Saved our Country

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits When I had the pleasure of introducing Paul Volcker at a conference, I referred to him as “the man who saved the country.” This was not hyperbole. It is hard to remember the deep trouble we were in, more than 40 years ago, when inflation reached 13% in 1979.

When I had the pleasure of introducing Paul Volcker at a conference, I referred to him as “the man who saved the country.” This was not hyperbole. It is hard to remember the deep trouble we were in, more than 40 years ago, when inflation reached 13% in 1979.

Times were terrible. A generation’s life savings, invested mostly in bonds, had disappeared. In real (inflation-adjusted) terms, the Ibbotson total return index of long-term Treasury bonds, initialized at $100 in 1940, had fallen to $47. That’s total return, with all interest reinvested! On a price-only basis, ignoring interest, $100 fell to $8.57 in real terms.1

You expect losses like those in countries like Argentina, where monetary folly tipped into hyperinflation and caused growth to come to a halt or go negative for long periods. But a slow-motion version happened in the United States, and it was not obvious we were going to avoid the Argentinian disease.

But we did avoid it, and Volcker deserves the credit.

The basic human will to overcome obstacles and prosper is so strong that even economies badly broken by monetary madness sometimes struggle forward. France, Italy, and Japan all had very high inflation rates either before or during their postwar economic miracles. Having the right individual at the right time in the right institution makes all the difference.

In 1979, in addition to prices spiraling up, trend productivity growth had fallen to 1% (one-half the postwar rate), labor markets were a mess, product quality was low, and you could buy America’s best companies for eight-times earnings. The part of the economy that could pass price increases along to consumers was doing well; the part that couldn’t was collapsing. Consumers...well, they were waiting in gas lines. President Carter gave his famous “malaise” speech, which didn’t contain the word “malaise” but should have.

Into this nation-sized train wreck rode “Tall Paul,” as he was affectionately known – he’s six feet seven inches tall, his family of origin is similarly sized, and they all used to live on Longfellow Street – and he cleaned up the town, like Clint Eastwood on his horse. OK, not exactly. In Keeping At It: The Quest for Sound Money and Good Government, an autobiography beautifully crafted with the help of the Bloomberg journalist Christine Harper, Volcker recounts the many struggles involved in achieving his aims. And his aims were ambitious: getting inflation down, righting the screwball monetary policy that prevailed when he was appointed, and getting along – or not – with presidents, economists, business leaders, and power brokers of the executive and legislative branches.

A hinge in history that I will never forget

When President Carter appointed Paul Volcker to the chairmanship of the Federal Reserve on August 6, 1979, the move smacked of desperation. Appointing a hard-money man, a strong monetarist, was not Carter’s instinct; the president had previously drawn on the meager talents of G. William Miller, whose tenure as Fed chair was highlighted by his prohibition of smoking during meetings.

Volcker fit the sound-money requirement, although he was not a follower of the leading monetary economist of the time, the University of Chicago’s Milton Friedman. Volcker was a Democrat, Friedman a Republican, and Volcker thought Friedman’s prescriptions rigid and unrealistic. But the two men were on the same side of the bigger questions. Both thought inflation was a more destructive force that the recession that could potentially result from combating it.

The book informs us of the personal anguish behind Volcker’s decision to take the chairmanship position. His wife Barbara was ill and did not move to Washington. Volcker had to take a massive pay cut. Barbara died in 1998. Paul, now remarried, is still alive (but unfortunately ailing) at 91.

Fifteen months into Volcker’s term, Ronald Reagan decisively defeated Jimmy Carter in the 1980 presidential election. Volcker was skeptical of his new boss (the Fed is supposed to be independent but the Fed chair serves at the pleasure of the president), and was concerned that the suave Hollywood actor might be a lightweight. But Volcker recalls that Reagan said, “There’s good news that the gold price is way down. We may be getting inflation under control.”

Volcker adds: “I don’t kiss men, but I was tempted.”

Surprise! Reagan was not an old fool, but a thinking man with a background in economics and at least an elementary understanding of monetary linkages. (Reagan’s economic sophistication was actually much greater than is revealed by this simple comment.) Volcker had a new ally, one who would prove challenging at times but whose overall vision was similar to his own.

Revenge of the monetarists

I was exactly the right age and in the right position to be profoundly affected by this transition: just young enough to be impressionable, just old enough to know something about the topic. I had recently acquired a degree in finance from the University of Chicago’s Booth School of Business. Many of my professors, ignored by Washington for a generation, were suddenly being recruited by the White House. George Shultz, the school’s former dean, became Secretary of State. Edward Levi, the university’s president, was attorney general. The Booth economist Yale Brozen, who persuaded me to attend the school and who gave me my first job, was on the Reagan transition team. It felt like my teachers and friends had taken over the country.

Brozen advised me to buy some Treasury bonds, which were then yielding 15%. I asked him why he was so sure they wouldn’t go to, say, 24%, causing me to lose a bundle. He said, “Paul Volcker is a friend of mine and he won’t allow that to happen.” It’s nice to know people in positions of influence. Unfortunately, I didn’t have any money to buy the bonds.

Running of the bulls

What happened after Volcker was appointed Fed chair? Exhibit 1 shows the Ibbotson total-return index for long-term Treasury bonds, expressed in real terms, from 1940 to the date of the Volcker appointment.2 The stock market (S&P 500 total return, including dividends, and also in real terms) is shown for comparison. Volcker had stepped into a sticky situation, the equivalent of a 40-year Great Depression for bondholders, while equity holders had done spectacularly well for the first two-thirds of the period, only to stumble badly after 1966, 1968, or 1972 (pick your high point; they’re all about the same).

Exhibit 1

Real total returns on U.S. stocks and bonds, January 1940-August 1979

Source: Morningstar Ibbotson SBBI. Used by permission.

The Fed’s responsibility is, of course, to keep inflation from getting out of hand and thereby maintain the real value of savers’ government bond holdings. It is not supposed to bolster the stock market. So Volcker was essentially taking charge of a failed institution. Since the passage of the U.S. Employment Act of 1946, the government had taken responsibility for a substantial degree of economic management over the previous half-century; it had not been doing its job.

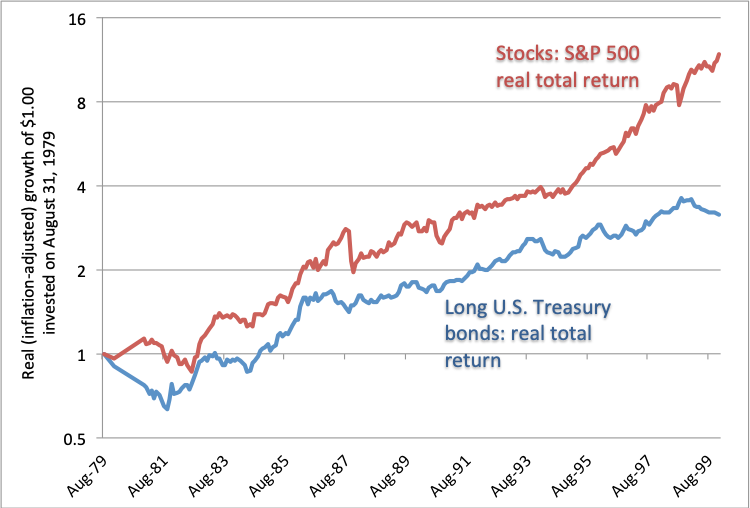

Volcker’s radical monetarism got off to a rough start: after he targeted the money supply instead of interest rates, the Federal funds rate soared to 21.5%, unheard of in American history. These sky-high rates drove many credit-dependent enterprises, some of which had survived the real Great Depression, out of business. There were two recessions in the first three years of Volcker’s tenure, the second one being particularly severe (and comparable in depth to the Global Financial Crisis of 2007-2009). But was that too high a price to pay for the outcome shown in Exhibit 2?

Exhibit 2

Real total returns on U.S. stocks and bonds, September 1979-December 1999

Source: Morningstar Ibbotson SBBI. Used by permission.

The stock market rose almost as much in the 20 years shown in Exhibit 2 as it did over 1940-1966. But the really dramatic difference between the two periods is in the performance of the bond market. Volcker had restored health to the market for which the Fed is most directly responsible, and those good conditions continue today (the bond market rose further in the new century, not shown).3

Some critics carp that the twin recessions of 1979 and 1981-1982 were too heavy a burden. However, sustained and accelerating inflation is a much greater threat to the long-term well-being of a society than a sharp recession (especially when the latter is followed by an extended recovery, which occurred).

Volcker really did save the country.

An overreaching president

Volcker recalls an awkward moment in 1984 when he was called into a meeting with President Reagan and James Baker, his chief of staff (later Secretary of the Treasury and Secretary of State). Reagan “didn’t say a word,” Mr. Volcker writes. “Instead Baker delivered a message: ‘The president is ordering you not to raise interest rates before the election.’”

Ordering him? The Fed chairman was stunned and disappointed. Presidents aren’t supposed to tell Fed chairmen what to do. President Nixon had set a negative precedent by pressuring (not ordering) then-chairman Arthur Burns to hold rates steady before the 1972 election. The misstep helped ruin Nixon’s reputation. Ronald Reagan was not known for overreaching: Iran-Contra aside, he had a conservative’s caution about exercising executive authority. Volcker hadn’t intended to raise rates anyway, but he lost some of his respect for the president over this incident.

Today, we see Donald Trump pressuring Fed chairman Jerome Powell not to raise rates, and it isn’t even an election year; don’t they ever learn? The Fed only has the credibility in the markets that it needs to do its job if it’s independent of political influence. It has a Congressional mandate to achieve price stability and maximum employment, not to re-elect presidents.

The back story

The Fed chairmanship is, of course, the capstone of any economist’s or banker’s career, and reflects decades of prior experience. But everyone’s basic values come from their childhood.

“They have a mortgage and we don’t”

Volcker learned the value of a dollar from his mother. As a child, he went to a summer resort where many people had boats. He asked his mother why so-and-so had a Chris-Craft and they didn’t. She said, “They have a mortgage and we don’t.” Never poor, Volcker had it drummed into him early that you can get poor in a hurry by living beyond one’s means.

Imagine his view of trillions of dollars in government debt three-quarters of a century later! He’s against it, and was quoted in a New York Times article as seeing “a hell of a mess in every direction.”4 He’s exercised not just about the overextended finances of our various levels of government but about the influence of money on politics. And he believes that our main civic institutions have thereby been corrupted to the point that people have lost respect for them: “Respect for government, respect for the Supreme Court, respect for the president, it’s all gone...even respect for the Federal Reserve,” Volcker said. Only the military, Volcker believes, still commands widespread admiration.

“The best job in the world”

Before he was Fed chair, Volcker accumulated a resume that reflected his lifelong attraction to public service. Although he was chairman of the Kennedy for president committee in his home town in 1960, he managed to become one of the two appointed Democrats in the Nixon administration. (The other was Daniel Patrick Moynihan.) Volcker describes his post, undersecretary of the Treasury for monetary affairs, as “for me, the best job in the world.” It’s nice to love your work.

The tumultuous Nixon years were full of monetary challenges. The dollar was devalued against most leading foreign currencies, the “gold window” (where dollars could be redeemed for gold at a bargain $35 per ounce) was closed, and inflation accelerated from a meow to a roar. President Nixon imposed wage and price controls, which had only previously been attempted in wartime; economists howled; and, in early 1974, Volcker decided he had had enough.

Facing a choice between academia and lucrative private enterprise, he went back to Princeton, where he had been on the faculty. The job did not last long. He was called back to public service as president of the New York Fed, a job he held from May 1975 until President Carter appointed him Fed chair four years later. Of the New York Fed, Volcker writes, “I asked my assistant to dispose of a large plant sitting just outside my office that appeared to be dying. A week or so later, I asked why it was still there. Her dispiriting answer: policy dictated that if I didn’t have the plant, none of the officers could have one.” No wonder it is hard for governments to get things done!

After the Fed

A private sector interlude

Upon leaving the government, Volcker became chairman of Wolfensohn & Company, an investment firm founded by former World Bank chairman Paul Wolfensohn. (Even heroes have to make a living.) He also rejoined Princeton as a professor of economic policy and served as a visiting professor at NYU. That’s a pretty good gig for a fellow without a Ph.D., but running the Fed probably provides a better doctoral-level education than researching an obscure topic so as to please a dissertation committee.

During this period in his life, Volcker remained deeply involved with policy issues. He led the Group of Thirty, a consultative club that includes many central bankers and Nobel or near-Nobel-level economists. He was concerned with the risks accumulating in the financial system and suggested substantial reforms, including stricter regulation. Thus, when financial conditions started to deteriorate in 2007, fulfilling a forecast by Volcker, earlier in the decade, of a crisis within five years, he played the role of elder statesman, meeting with figures such as Treasury Secretary Tim Geithner and Fed chair Ben Bernanke periodically as the crisis unfolded.

But Volcker did not always back the consensus. The 2008 rescue of Bear Stearns, accomplished through a government-backed merger with JPMorgan Chase, strained Volcker’s patience: “The Fed...had acted at the ‘very edge of its lawful and implied powers’,” invoking a half-forgotten section of the Federal Reserve Act that allowed it to lend to nonbanks in emergencies. “The point was that the Fed should not be looked to as lender of last resort beyond the banking system,” concludes Volcker.

But Volcker did not think that acting at the very edge of its authority was wrong, only of questionable legality. He knew that unfreezing the commercial paper and repo markets, which were collapsing as some of the biggest players in the market, such as Coca-Cola and General Motors, were unable to roll over their short-term obligations, was necessary to prevent a broader economic collapse. Unfortunately, Congress has since taken away the Fed’s previously ambiguous power to act as lender of last resort to nonbanks, removing another arrow in the Fed’s quiver that could be badly needed in the next emergency.

An unexpected role in the Obama administration

Following the election of Barack Obama, the president called Volcker into public service once more, this time taking the reins of the newly created President’s Economic Recovery Advisory Board (PERAB) at the age of 81. Volcker’s advocacy of more conservative banking practices led to tussles within the White House, but Obama resolved them by “announcing his administrative support for a ban on speculative activities within commercial banks, ‘which we’re calling the Volcker Rule, after this tall guy behind me’ [Obama said].”

The point of the Volcker rule was to apply “the simple idea that ‘thou shall not gamble with the public’s money’,” he writes. The moral hazard of banks being able to take risk and have potentially huge losses paid by the taxpayer, but keeping gains for themselves, had finally been addressed. Despite rising asset prices and the accumulation of both public and private debt, studies such as a recent effort by the Nobel Prize-winning economist Robert Engle show that financial crisis risk is low. The Volcker Rule seems to be working.

The Paul Volcker and William Sharpe encounter

Investors will enjoy an anecdote Volcker tells about an encounter he had with William F. Sharpe, who (with some co-discoverers) formulated the Capital Asset Pricing Model, one of the foundations of modern finance. Volcker writes that when both were attending a conference on new techniques in financial engineering,

I nudged him and asked how much this new financial engineering contributed to economic growth, measured by GNP. “Nothing,” he whispered back to me. It was not the answer I anticipated. “So what does it do?” was my response.

“It just moves around the [economic] rents in the financial system. Besides it’s a lot of fun.” (Later, at dinner, he suggested the possibility of small ways in which economic welfare could be advanced. But I felt I had already gotten the gist of his thinking.)

The blunt skeptic

Volcker spoke as mysteriously as any Fed chair when he was in office – “we did what we did, we didn’t do what we didn’t do, and the result was what happened” – but afterward he became known for his blunt pronouncements. He said he couldn’t think of a financial innovation since the ATM that did any social good.

I’d offer the index fund as one candidate, and using futures and options to hedge tail risk is another. Moreover, some clever financial engineering will be required to create liquid and transparent markets in life annuities, which will be very useful if they arise. The long fellow doth protest too much. Sharpe should have stood up for his profession a little more robustly. But a skeptical attitude is healthy in a policymaker.

Volcker believes the financial system is still vulnerable and that the response to the 2008 crash didn’t do much to prevent repeat episodes. The Volcker Rule is not enough; he favors even more regulation, and worries that the Fed and other institutions tasked with overseeing the banking system aren’t doing enough to prevent a “too big to fail” situation from recurring.

Evaluating the book

Readers interested in Volcker’s tenure as Fed chairman, as dramatic a period in our economic history as the (fairly) recent crisis, should start at chapter 8. But Volcker’s deep experience, his skeptical attitude, and his devotion to the public good are evident on every page. Unfortunately, we’ll never known if the luminous writing is his or Christine Harper’s; the book is written in the first person, in Volcker’s voice. Whoever took the lead oar in the writing is a master of the craft.

Economists, investment managers, and sophisticated advisors would have benefited from more technical detail. Volcker is much more than a political operative; he’s an accomplished monetary economist and policy analyst who could have shed more light on our current challenges. His chapter 15, “The New Financial World,” addresses these issues, but only in words – no graphics, no math, no data. This is not really a criticism since the book is an autobiography, not an economic treatise, but it’s a fact worth noting.

An inspiring book

Volcker appeared on the scene as Fed chairman at one of history’s critical moments. The United States could have become a monetary basket case on the verge of hyperinflation. Instead, under his leadership, we enjoyed 40 years of disinflation and a bond bull market that impacted the fortunes of equity and bond investors even today. While the twenty-first century has been tumultuous, it is not for monetary policy reasons. In the long tail of Volcker’s accomplishments, the dollar is sound and the inflation rate mild.

Investors and advisors who believe understanding history is the key to succeeding in the future – and that should be all of them – should read Volcker’s inspiring book.

Larry Siegel is the Gary P. Brinson Director of Research for the CFA Research Foundation and an independent consultant. Prior to that, he was director of research in the investment division of the Ford Foundation. His book, Fewer, Richer, Greener will be published by Wiley in 2019. He may be reached at [email protected] and his web site. Larry thanks Stephen Sexauer, CIO of the San Diego County Retirement Employees Association, for his valuable comments and suggestions.

1 These are end-of-1979 data. The bond market would go even lower before it recovered in the 1980s. While most bond investors don’t hold only the longest bonds, some liability hedgers, such as pension funds, do.

2 To the nearest month-end.

3 Exhibit 2 goes only through December 1999, not because more recent data are unimportant, but because the needed data are expensive and I don’t have a subscription. Also, Volcker’s influence does not extend forever into the future; 20 years is a reasonable cutoff.

4 Sorkin, Andrew Ross. 2018. “Paul Volcker, at 91, Sees ‘a Hell of a Mess in Every Direction’.” New York Times (October 23),

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All