Why Advisors Should Distinguish Base and Discretionary Expenses

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Modern retirement theory assumes that all assets on an individual’s retirement sheet1 (financial capital, social contract, human capital) should be used for their definitional highest and best purpose. To determine the highest and best purpose of retirement sheet assets, goals are prioritized and assets and liabilities are matched.

The difference between base (mandatory or essential) and discretionary (voluntary or non- essential) expenses in retirement is fundamental and consequential. Properly making this distinction may be the most important decision in order to use assets efficiently and effectively in retirement income planning. Some advisors fail to highlight the difference between expense categories and claim that clients do not see food, shelter or insurance differently than country club dues or vacation cruises. Hence the expense categories are combined and called lifestyle expenses.

This is a distortion of affluence. Lifestyle expense is an unfortunate term and promotes the idyllic sense that to live the lifestyle one wishes these expenses should take on the same priority funding importance as basic expenses. Expense distinction is the most critical issue to optimize the use of retirement assets and to cover base (essential) expenses. Our “3S” model2 posits that net cash flow (base income) should cover Base expenses with sources of income that are simultaneously secure, stable and sustainable.

Advisors should always look for ways to add value to clients, especially if operating under a fiduciary standard. An overlooked area for value-add in retirement planning is in expense categorization. Many advisors question whether we should distinguish between types of expenses for planning purposes. The typical salvo is that clients don’t want to distinguish between food and country club dues, so why should we force them into expense categorization?

But if we fail to advise on this distinction, we miss a significant opportunity to properly frame client decision-making. If the distinction adds value and improves outcomes, should not advisors, as a best practice, parse these expenses in planning? We make distinctions between different kinds of stocks (small, large, value, growth) or bonds (corporate, sovereign, or high yield), so why the pushback on acknowledging expense types? The short answer is that if we push this conversation into a logical framework, we can improve client outcomes and add value.

The most important input to a retirement plan is monthly base expenses. All other retirement calculations measure or test the sustainability of this single number. Retiree outcomes can be enhanced by focusing on what the retiree can control, beginning with their base expenses. Intentional retirement budgeting improves sustainability through generating the highest net-cash flow from available assets while preserving other assets for funding unknowable future needs.

Retirement-income planning should start with the cash flow required to cover budgeted essential expenses. Rather than beginning with income replacement, start with necessary expenses, then build stable, secure, sustainable income (3S income) through liability matching. Income replacement ratios (i.e., the percentage of pre-retirement income that is needed in retirement) are too simplistic and no substitute for detailed budgeting. The goal of generating retirement income is to attain the highest net cash flow, i.e., the after-tax cash after basic expenses have been funded.

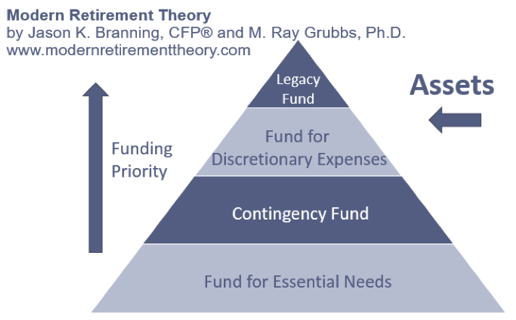

The retirement-decision framework offered by modern retirement theory places base or essential expenses as the first priority, followed by contingencies, discretionary and finally legacy. The rationale for establishing this hierarchy of funds is derived from the two unknowable questions. The first is longevity: How long an individual client will live, thereby requiring income to fund base expenses in an unknowable context. The second is contingencies – expenses that are unknowable during the remaining lifespan. For the individual retiree, the answers to these two questions form the planning context for retirement income.

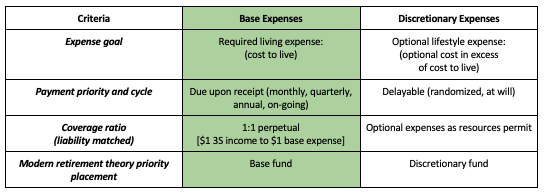

The following table contrasts the two choices to encourage clients to thoughtfully categorize base (essential) versus discretionary expenses.

Let’s review each of the four levels of distinction.

Expense goal

First, there is a definitional distinction between base and discretionary expenses. This helps decide which assets to convert to income and each asset’s income-producing value (IPV) and conversion costs. Base expenses as those that are required to live in a modern society. They are aligned with the consumer expenditure survey and include food, clothing, housing, utilities, taxes, healthcare, insurance, transportation and other expenses to unique individual clients. While many advisors will disagree with how expenses should be funded in retirement, they agree that it is fundamentally different to provide income for food versus for vacations. Withdrawals from portfolios should reflect this. This is a valid distinction recognized by many retirees – they just need a better framework to view this issue. Vacations are an important part of life, yet they do not rise to the priority funding requirement level of a balanced diet.

The client impact of the distinction between essential and discretionary is profound. Retirement income must be put in place that is simultaneously stable, secure, and sustainable (3S model) to pay for base expenses for as long at the retiree lives. Discretionary expenses are not held to the same rigorous standard – they can be funded with income from other sources, even one-time sources, and can, by definition, be deferred until a later time. The impact on a client’s assets may be significant as well by deferring assignment of certain assets for income until a later time (e.g., using a bond ladder to delay Social Security until age 70).

Payment cycle

Base expenses are ongoing for as long as the retiree lives. Their form may change but the essential nature will not. For example, a house payment or rent may change form to a payment to a long-term care facility, but the ongoing nature of the expense will not change. Everyone will pay for a place to live for as long at they live. These types of expenses will occur monthly, quarterly, semi-annually or annually. The frequency may change, but they will continue as essential expenses of living.

In contrast, discretionary expenses will occur on a non-regular, client-determined basis. For example, traveling could be planned by the client, but the exact timing of a trip may vary or not occur at all depending on how market-based portfolios perform.

Payment priority

Base expenses are due on a regular, systematic basis. They are due upon receipt and cannot wait until funds are available. To depend on unreliable or volatile sources or sources of income does not constitute fiduciary advice nor a sound planning recommendation.

Discretionary expenses are the polar opposite. By definition, they are optional and can be funded when and if funds are available. Advisors should acknowledge expense priority as directly affecting retirement sustainability. By paying attention to types of expenses, advisors add value to clients by increasing sustainability. These expenses can be controlled, whereas market returns cannot. By focusing on what can be controlled, advisors are proactively empowering clients to take ownership of their financial decisions.

Framing an ongoing expense in terms of a net present value through life expectancy can be eye opening. The magnitude of a monthly expense can be expressed as the net present value on the retirement balance sheet. For example, a couple who is 65 and has a $237 monthly expense is the equivalent of having or needing $50,000 in assets. If on-going, monthly base expenses are cut by $237, the effect is that $50,000 less of lifetime assets are required.

Coverage ratio (liability matched)

The coverage ratio is the sum of all coverage contributions compared to base fund expenses. The theoretical goal is to have base expense liabilities covered by 3S base income sources at a 1:1 ratio. Practically, we suggest a ratio of 1.05 or 1.1. Creating slightly higher than required income versus expected expenses avoids generating too high an income that is eroded by taxes, but also leaves a gap in the event of an intra-year increase in essential expenses, e.g., a short-term spike in inflation. A coverage contribution is the measure of total base expenses covered by net income produced by an asset. Discretionary expenses can be covered as resources allow. For example, a retiree’s Social Security income covers their base expense needs by 45%, so the coverage contribution of one asset, Social Security, would be .45.

Conclusion

When developing a retirement income plan, advisors should begin with a focus on actual client expenses. Expenses should be categorized and a priority of expenses established. Base expenses are, by definition, different than other expense types. Matching up the required retirement income with base expenses leads to greater tax efficiency and asset sustainability over time.

Jason K. Branning, CFP® and M. Ray Grubbs, Ph.D. are principals with MRT, LLC a retirement education firm based in Ridgeland, MS. Additionally, Jason is an investment advisory representative of Asset Dedication, LLC, an SEC registered investment advisor and Ray is a tenured professor at Millsaps College in Jackson, MS.

1 Retirement Sheet is a snapshot of assets, liabilities, income and expenses. It frames an individual’s balance sheet and cash flow statement. A Retirement Sheet includes Social Security benefits, pensions, not simply housing wealth and portfolio assets. The Retirement Sheet is a comprehensive income snapshot: Human Capital, Financial Capital, Social Contract.

2 Crafting Retirement Income that is Stable, Secure, and Sustainable. Branning and Grubbs. Journal of Financial Planning. December 2017.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All