Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisors tout the obvious advantages of liquid portfolios and investments. But they are slower to mention that this liquidity comes at a cost. A vast literature in finance supports the idea that less liquid assets offer higher expected returns. This is the so called “liquidity premium.”

Given these premiums, advisors should look more closely at their clients’ investments as well as portfolio design from a liquidity perspective. Investors, particularly those with long-term goals, may be paying for daily liquidity they don’t need. By ignoring liquidity premiums, advisors are not maximizing the funds of their clients.

What is liquidity – and what is the liquidity premium?

Liquidity is a slippery topic. There is no universal definition, except for maybe that of economist Maureen O’Hara, who said, “liquidity is hard to define but you know it when you see it.” Part of the problem is that liquidity is phase dependent. It varies through time and by market condition.

In general, liquidity refers to how easy it is to buy or sell assets. This turns out to be a multi-dimensional concept. It involves speed (how long it takes to sell something), cost (the bid-ask spread), and the price impact of a trade. Volume, used by some analysts as a measure of liquidity, is a very poor proxy for liquidity. More telling is the price impact induced by volume, that is, how much can you trade without moving the price?

More interesting for investors is what this means for returns. Investors need to be compensated for the cost of trading less liquid securities, as well as the risk that assets could turn illiquid in a crisis. The result is that these securities should offer investors higher expected returns, the “liquidity premium.”

Liquidity premiums have been found in many different asset classes, such as stocks or corporate bonds. They can be seen in even the most seemingly liquid asset class of all: US Treasury securities. There are liquidity differences in the Treasury market, with the older “off the run” securities less liquid than their newly issued on the run counterparts. Both of course have the same risk of default, yet there are differences in yield. One research study found that the less liquid off-the-run Treasury notes had an average yield of 43 basis points higher than their on-the-run counterpoint.

Liquidity premiums are difficult to quantify and vary by market condition. However, the CEO of the Harvard Management Company, Jane Mendillo, in 2014 put a number on them, in an expected returns framework. She said, “We should be getting an incremental return for that illiquidity – and we call that our illiquidity premium – of at least 300 basis points annually on average over what we are expecting in publicly traded stocks.”

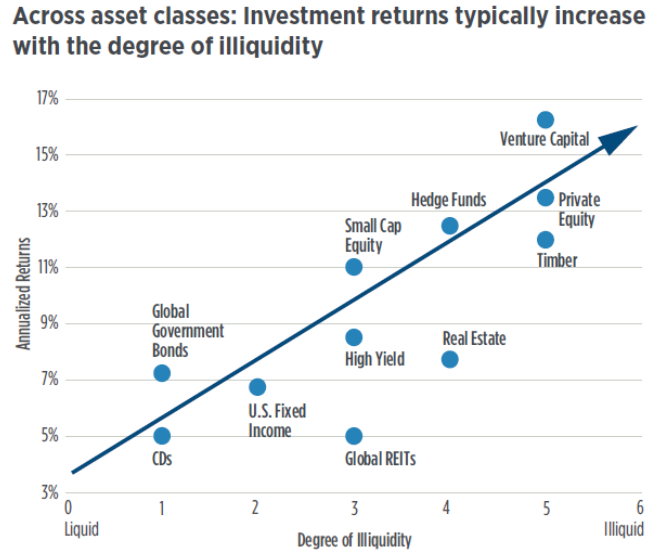

The idea that there are liquidity premiums within an asset class is well-established. More controversial and hotly debated is the idea that liquidity can explain the return differences between asset classes, given their different risks, characteristics, and role for management skill. Nonetheless, researcher Antti Ilmanen, found a relationship between an asset classes’ degree of illiquidity and expected returns.

Liquidity premiums (along with better information) therefore go a long way in explaining the seeming “magic” of the high returns of alternative asset managers.

Accessing liquidity premiums

This research about liquidity premiums has until recently been merely academic. Individual investors’ portfolios have tended to be 100% liquid.

This extreme liquidity characteristic of individual investors’ portfolios is not merely the result of conventional thinking; it’s that individuals had few other investment options, outside of private vehicles. For instance, mutual funds are required to be highly liquid. They have a 15% illiquid investment limit.

However there is another ’40 act vehicle that doesn’t have the same prohibition on housing illiquid assets: closed-end funds. The SEC notes “closed-end funds are permitted to invest in a greater amount of ’illiquid’ securities than are mutual funds.”

There have been rapid advancements in closed-end fund product design to take advantage of this illiquidity feature. Though in the past closed-end funds primarily offered traditional assets classes, today some offer alternative illiquid assets, with attendant, liquidity premiums.

Some investors are not aware of these developments. WSJ columnist Jason Zweig termed interval funds, “the trendiest investment on Wall Street...that nobody knows about.” (Interval funds are a variant of closed-end funds. They aren’t traded; they only offer limited redemptions and intermittent liquidity compared to traditional closed-end funds. In contrast to interval funds, listed closed-end funds still provide liquidity at the fund level because they can be bought and sold on an exchange).

Implementation ideas – and some risks

Putting these ideas about illiquidity into practice requires some new approaches by advisors. It also means learning from the excesses of institutional investors.

Illiquid investments carry unique risks. They provide higher expected, not guaranteed returns. These are investments for the long-term so “in depth due-diligence of the investment is vital,” argues advisor Michael Kitces in his “Nerd’s eye view” column. He offers some suggestions of how to do this, including the forceful recommendation that, “only invest in illiquidity if it is transparent enough to properly vet in the first place!” Advisors may find that many illiquid investments don’t have the requisite transparency.

A less visible, but no less important, problem is that the theoretical framework underpinning financial planning doesn’t really grapple with illiquidity, either as a risk or a source of return. In traditional asset pricing models liquidity plays no role at all because it is assumed away: markets are “frictionless” and participants are price takers. This is true of Markowitz’s original modern portfolio theory. Much of financial-planning software was derived from this theory.

Therefore, financial planners need to take a different approach when thinking about illiquidity, focusing on the client’s needed cash flows, both expected and unexpected. They need to look at the illiquidity of the total portfolio including residential housing and risk of a job loss in times of a liquidity crisis This modeling exercise can underscore the value of a planner and the limitations of robo-advisors.

The experience of some institutional investors shows how not to do this. In their rush to capture the illiquidity premium, supposedly cutting-edge college endowments moved to nearly completely illiquid portfolios that were also leveraged; they forgot about their short-term liabilities. The financial crisis revealed the problems of this approach. But a 100% liquid portfolio is not the right-answer either, given that endowments still have very long, even infinite time horizons. And hence, even after the crisis, many endowments still retain large exposures to highly illiquid assets.

Conclusion

Liquidity is very valuable and therefore very expensive. Illiquid assets tend to be comparatively cheaper. For example, one study found that restricted stocks (stocks that can’t be traded on public markets, for two years at the time of the study) sold at a 30% discount compared to their liquid counterpart.

Introducing illiquid assets into a portfolio introduces new and potentially diversifying sources of return beyond the equity risk premium that dominates returns today. This higher expected return from illiquid assets can in turn influence portfolio choice, with investors with longer time horizons in a position to exploit these premiums.

For many clients, the cost of completely liquid portfolios is a price well worth paying. They may be facing uncertain life situations and need to have portfolios they can convert to cash overnight. But this isn’t true of all clients. Particularly in the context of goals-based planning or bucketing, more nuance is needed. Portfolios might be directed towards specific long-term, even intergenerational goals. And here it is absurd to ignore liquidity premiums and create 100% liquid portfolios that could just as well serve the immediate goals of day traders. Yet that is conventional practice today.

Individuals don’t need to recreate institutional, virtually illiquid portfolios. Instead, for individual investors – particularly in the portion of their portfolio dedicated to retirement or next-generation wealth – the truth lies somewhere in between.

David Adler is author of the monograph, “the New Economics of Liquidity and Financial Frictions,” published by the CFA Institute Research Foundation. He is a senior advisor to XA Investments, a Chicago investment manager that provides access to illiquid alternative investments using closed-end funds. The views expressed here are his own and don’t necessarily reflect those of XA. He can be reached at [email protected]

Read more articles by David Adler