Dimensional versus Vanguard: A Test of Simple Factor Investing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

This article originally appeared on ETF.COM here.

There is overwhelming evidence that simple indexing strategies outperform the vast majority of investors, be they individuals or institutions.

Perhaps the simplest strategy, as advocated in the new book by Taylor Larimore, is to hold just three funds.

For equities, you can own the Vanguard Total Market Index Fund (VTSMX) and the Vanguard Total International Stock Index Fund (VGTSX). On the bond side, you can own the Vanguard Total Bond Market Index Fund (VBMFX). Had you owned such a portfolio over the past 20 years, you would have outperformed most investors. This approach is not only a very good one, but will continue to outperform a large majority of investors going forward.

That said, such an approach ignores the academic evidence demonstrating there are certain factors that have provided above-market returns to investors willing and able to accept their additional risks.

These factors have performed with persistence across long periods; pervasiveness across sectors, countries, regions and even asset classes; and robustness to various definitions. What’s more, they have intuitive risk-based or behavioral-based explanations for why they should persist and are implementable, meaning they survive transaction costs. The two factors with the longest history are size and value.

Dimensional’s approach

Firms such as Dimensional Fund Advisors have been building portfolios based on academic findings regarding factors for decades. Therefore, investors have been able to build portfolios that accessed these factors.

Typically, investors constructed equity portfolios using the building blocks provided by Dimensional, which include U.S. large-cap, large-cap value, small-cap and small-cap value asset class funds, funds reflecting the same four asset classes for non-U.S. developed markets, and three emerging market asset class funds (large-cap, small-cap and value). (Full disclosure: My firm, Buckingham Strategic Wealth, recommends Dimensional funds in constructing client portfolios.)

To many investors, owning 11 funds was too complex. In 2005, Dimensional addressed that issue by creating what they call core funds, which provide exposure to all these asset classes. Core funds have the benefit of diversifying across factors/asset classes. In addition, they improve tax efficiency over an individual fund structure because they greatly reduce the turnover impact of stocks’ migration across asset classes. They also eliminate the need for investors to rebalance across asset classes, as the fund does it for them via cash flows and dividends.

Thus, today, investors can implement a factor-based equity strategy with just three Dimensional core funds: a core U.S. fund (DFQTX), a core international fund (DFIEX) and a core emerging markets fund (DFCEX). Alternatively, you could own Dimensional’s World ex-U.S. Targeted Value Fund (DWUSX), which combines international and emerging markets into a highly tilted (to the size and value factors) portfolio, or its world ex-U.S. Core Equity Fund (DFWIX). Either would allow you to own just two equity funds.

Dimensional versus Vanguard

With that knowledge, we can go back in time and see how an investor who was willing to accept these different risks, and the tracking error that can occur (factor-based funds will perform differently than total market funds), would have done.

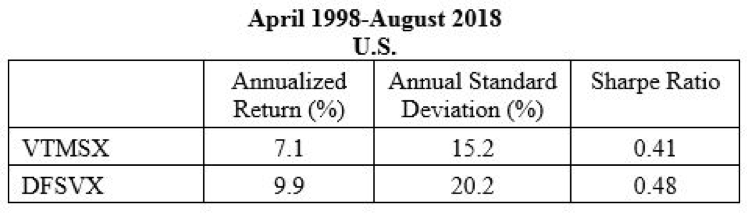

While there are many possible combinations, the following analysis uses the Dimensional fund with the most exposure to the size and/or value factors for the U.S. (DFSVX), developed international (DISVX) and emerging (DFEVX) markets.

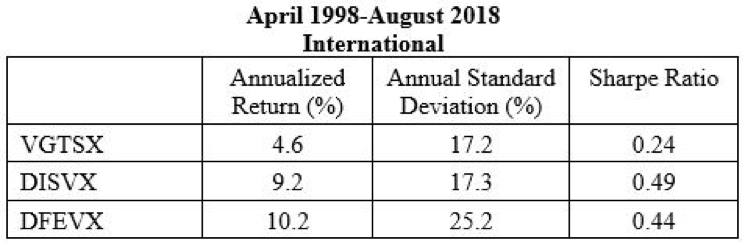

For comparison purposes, I’ll also show the returns of the Vanguard Emerging Markets Index Fund (VEIEX) and the Vanguard Developed Markets Index Fund (VTMNX), permitting you to look at a three-equity-fund portfolio versus the simpler, two-equity-fund portfolio. This allows for a more apples-to-apples comparison.

I’ll use the longest period for which we have data available (based on when all the funds were live). Thus, my start date is April 1998. Fund returns data comes from Portfolio Visualizer. Factor premiums are from Ken French’s website and run through July 2018 (one month less than our returns data, giving us a slightly different period than for the returns data).

During this period, and based on Ken French’s data series, the monthly U.S. size and value premiums were 0.25% and 0.12%, respectively. Those premiums help to explain the higher returns of DFSVX.

Global ex-U.S. perspective

I’ll next look at the data using Vanguard Total International Stock Index Fund Investor Shares (VGTSX) to represent the total international stock market in a two-equity-fund portfolio.

During this period, the monthly global ex-U.S. size and value premiums were 0.13% and 0.41%, respectively. Those premiums explain most of the difference in returns. But because the global ex-U.S. premiums do not include emerging markets, we need to consider the premiums there as well. During this period, the Dimensional Emerging Markets Value Index provided an annualized return 2.9 percentage point higher than its Emerging Markets Index. This premium helps explain the differences in returns.

Of interest (partly because it comes after a period when many pundits had declared the size premium dead) is that, during this period, the size premium was much larger in U.S. stocks (virtually twice as big as it was in international stocks) while the value premium was much larger internationally (about 3½ times as great as it was domestically). That provides a demonstration of why diversification is important not only across regions, but across factors.

Separating developed and emerging markets

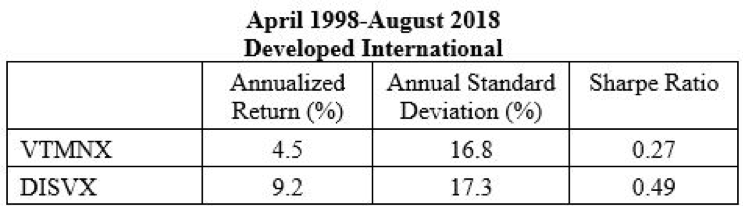

So that we can isolate the performance of developed and emerging markets, I’ll next look at them separately.

As I previously mentioned, during this period, the monthly global ex-U.S. size and value premiums were 0.13% and 0.41%, respectively. Those premiums explain most of the difference in returns.

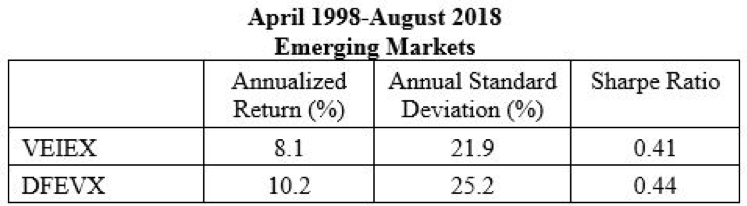

While we don’t have Fama-French factor premium data available for emerging markets, we can examine the returns of the Dimensional Emerging Markets Index and the Dimensional Emerging Markets Value Index to see if there was a value premium over the period. During this period, the Dimensional Emerging Markets Index returned 8.5% versus the 11.4% return of its Emerging Markets Value Index. The difference explains why DFEVX provided higher returns.

For those interested in seeing how a globally diversified, multifund portfolio would have performed, you can use the portfolio tool available at Portfolio Visualizer. It allows you to test various allocations.

Summarizing, over this period, there were significant size and value premiums around the globe, and investors were well-rewarded for taking those risks. Of course, there will be periods, even very long ones, where this will not be the case. Investors who can’t take the heat that underperformance may bring should stay out of the proverbial kitchen.

Core funds

I’ll now turn to looking at the performance of the aforementioned core funds. Again, for those interested in exploring how funds might mix in a portfolio, you can test various portfolios at Portfolio Visualizer.

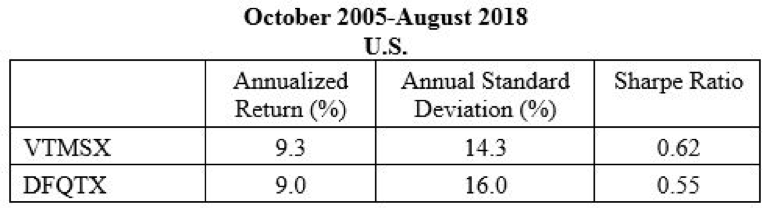

The first full month of inception for Dimensional’s first core equity (multi-asset class/multifactor) fund, DFCEX, was May 2005. The first full month for the other two core equity funds (DFQTX and DFIEX) was October of that year. With the introduction of those funds, we can also look at how core funds have performed since inception compared to the three Vanguard funds.

While Dimensional’s core funds have more exposure to the size and value factors than total market funds do, they are more “marketlike” than DFSVX, DISVX and DFEVX. Thus, they have lower expected returns as well as less tracking error risk.

During this period, the monthly U.S. size and value premiums were 0.16% and -0.08%, respectively. While a negative value premium over such a period was not to be “expected” (over 10-year periods, the size premium in U.S. stocks was negative 23% of the time and the value premium was negative 14% of the time; at 20 years, the figures were 15% and 6%, respectively), it demonstrates long periods of underperformance can occur. This goes to show that discipline is key to being a successful investor.

It’s also worth noting that, while over this more-than-12-year period, there was no benefit to increased exposure to the value premium, DFQTX’s underperformance was relatively small. On the other hand, as you saw with the data that went back to April 1998, there was a large benefit over that much longer period.

Non-U.S. core comparison

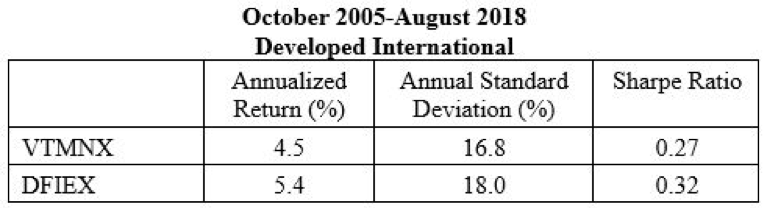

I’ll now look at developed international markets.

During this period, the monthly global ex-U.S. size and value premiums were 0.04% and 0.11%, respectively. This helps explain DFIEX’s higher returns. The outperformance in international markets (0.9 percentage points) was greater than the underperformance in the U.S. market (0.3%age points).

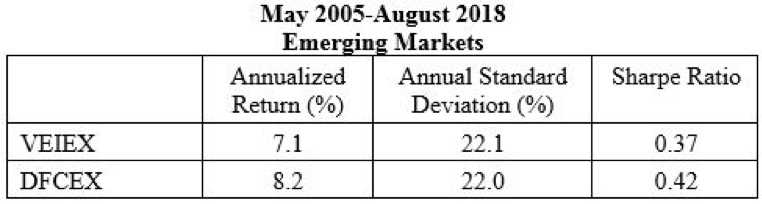

Next, I’ll look at emerging markets.

During this period, the Dimensional Emerging Markets Value Index provided a return 0.7 percentage points higher than its Emerging Markets Index, and the Dimensional Emerging Markets Small Index provided a return 1 percentage point higher – helping to explain the higher return of DFCEX.

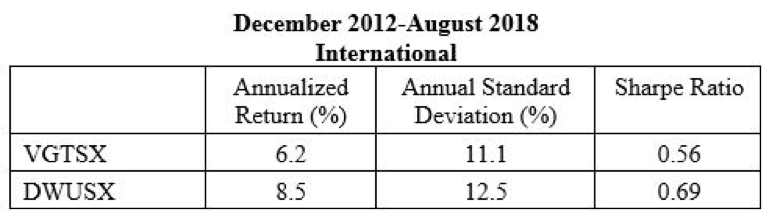

In November 2012, Dimensional introduced its World ex-U.S. targeted value fund, DWUSX, which has more exposure to the size and value factors than DFIEX. It also combines developed international and emerging markets into one fund. The first full month we have data for it is December 2012.

During this period, the monthly global ex-U.S. size and value premiums were 0.22% and 0.05%, respectively. In emerging markets, Dimensional’s Emerging Markets Value Index produced a return 1 percentage point lower than its Emerging Markets Index, but the Dimensional Emerging Markets Small Index produced a return 1 percentage point higher.

The premiums in developed international markets help explain the higher return to DWUSX (about 80% of its holdings are in the developed markets).

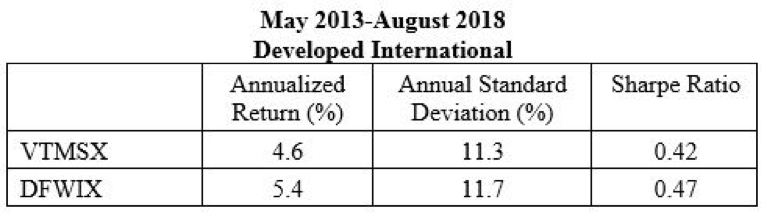

I have one more core fund to examine. In April 2013, Dimensional introduced its World ex-U.S. Core Equity Fund (DFWIX). The first full month of data we have for it is May 2013. Like DWUSX, about 80% of its holdings are in developed markets.

During this period, the monthly global ex-U.S. size and value premiums were 0.21% and 0.00%, respectively. In emerging markets, the Dimensional Emerging Markets Value Index underperformed the Dimensional Emerging Markets Index by 1.2 percentage points, while its Emerging Markets Small Index outperformed by 0.2 percentage points. The size premium in developed markets helps explain the outperformance of DFWIX.

Summary

Factor-based portfolios do not have to be complex. They can be just as simple in terms of number of funds as total market portfolios are – or at least almost as simple. There is no need to own a dozen or more funds, as some advisors might recommend. That not only overly complicates the portfolio, it’s also less efficient than using core (multi-asset/multifactor) funds, especially for taxable investors.

For investors interested in learning why you should expect the size and value factors (as well as the momentum and profitability/quality factors) to provide premiums in the future, I refer you to my book, “Your Complete Guide to Factor-Based Investing.”

Disclosure: The funds discussed in this article have been selected for informational purposes to illustrate the data and are not provided as a specific recommendation to purchase a particular security. Past performance is historical and does not guarantee future results.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All