The (Un)certain Future for Small Advisory Firms

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Behemoths like Amazon and Uber have transformed industries, putting smaller competitors out of business. Could the same fate await smaller financial planners? Many analysts have predicted massive consolidation in our industry, resulting in a landscape where a few “Goliaths” make it impossible for the small “Davids” to compete. Is this thesis accurate and, if so, what should advisors do to protect themselves?

Behemoths like Amazon and Uber have transformed industries, putting smaller competitors out of business. Could the same fate await smaller financial planners? Many analysts have predicted massive consolidation in our industry, resulting in a landscape where a few “Goliaths” make it impossible for the small “Davids” to compete. Is this thesis accurate and, if so, what should advisors do to protect themselves?

In 1999, Mark Hurley, an industry consultant and manager of a family of mutual funds, published a white paper that forecast not just the death of the solo practitioner, but the extinction of pretty much every financial services firm except for a small number of Goliaths, whose economies of scale would make them insurmountable competitors. They would be more efficient (and possibly offer planning at lower price-points) than the David-sized firms, have better name-recognition (and therefore more effective marketing), and they would offer in-house expertise that the smaller firms could not afford.

You continue to hear resonances of this message today, in part from Hurley (now president, ironically enough, of Fiduciary Network, LLC, a firm that funds mergers and consolidations, making him hardly an impartial observer in this discussion). Strong echoes have recently come from rollup firms like Fiduciary Network, whose recent white paper suggested that only Goliath firms with much more than $1 billion under management will have the scale to succeed in the future. And Ric Edelman, whose firm aggressively buys up smaller practices, has softened the negotiating stances on the other side of the table by repeatedly telling us, in press interviews, that smaller advisory firms simply cannot prepare adequately for the future. (See here and here).

Despite these predictions, we continue to have a thriving ecosystem of smaller advisory firms, including the XY Planning Network of Millennial advisors. Today, almost half of all RIA firms have less than $100 million in assets under management – 17,688 state-registered firms and 18,225 larger firms registered with the SEC.

But at the same time, bolstering the argument that we are still transitioning to gianthood, the number of firms with more than $1 billion under management – the emerging Goliaths – has grown from essentially zero 10 years ago to – according to the latest Cerulli report – 687 today. Those 687 now hold just over 60% of the total client assets in the industry. So there is clearly growth at the top end. And anecdotally, we can all see a clear trend of smaller firms merging in order to achieve scale and develop a more stable succession plan.

So the question before us is: Was the original prediction correct, just too early in the cycle? Will solo and smaller RIA firms have to merge and grow in order to survive? Do solo advisory firms face an existential threat to their existence and, if so, should they contact Ric Edelman with a firesale price?

Or is something else going on that will create an ecosystem where both the Goliaths and also the Davids can thrive?

That’s the first question. The second question is: We all know there are advantages to having size and scale. But are there comparable advantages that the Davids have over the Goliaths? And if there are, how can the smaller firms use those advantages and thrive despite the woeful predictions about their future?

Let’s tackle the first question. If we try to project the spectrum of firm sizes in the (relatively young) financial planning profession as it matures, then it is reasonable to look at the experiences of more established professions. The legal and accounting professions operate much like planning firms; that is, they provide expertise to their clients in a professional setting, and we all know that they have large and small firms in their respective ecosystems. Over the centuries of their professional existence, have their larger firms driven to extinction the smaller competitors?

Far from it. The table shown here lists the number of law firms in the U.S. marketplace, broken down by size of the firm:

The center of gravity is the smaller 1-4 professional firms, and the number of small firms with 5-9 professionals is roughly double the number of firms with 10-19 professionals, and that, in turn, is double the number of firms in the next higher tier. At the very top, there are only eight firms with more than 1,000 attorneys, led by Goliath law firms like Kirkland & Ellis and Baker McKenzie, which have offices pretty much everywhere.

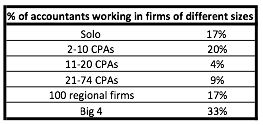

The same information on the accounting profession is a bit harder to find; you have to go back to an AICPA survey 10 years ago to find the spectrum of firm sizes on this table:

This is not exactly the same picture, but it tells a similar story: many more accountants are working in accounting firms with 10 or fewer CPAs than in the Big 4 firms.

In both the legal and accounting professions, over more than a century of professional evolution, the Goliaths have failed to drive the Davids out of business.

If we look closer, we can see that both professions reached an equilibrium with similar-size demographics. There is a handful of large national firms, a larger number of regional firms, a larger number of large local (city) firms, and a large plurality of small firms and practitioners who make up anywhere from 35% to 49% of the total. Underneath these relatively stable statistics, there will be a lot of churn, where smaller firms will merge with each other to gain scale and eventually move up the scale, while individual staff professionals will leave the partner track at larger firms and go solo, replenishing the population of smaller firms.

How does today’s planning profession compare with these rival professional spectra? Envestnet, drawing on SEC, FINRA and Cerulli data, published a report in 2017 which evaluated the size spectra of the RIA population. Recasting the data to a similar table, this is what we look like today:

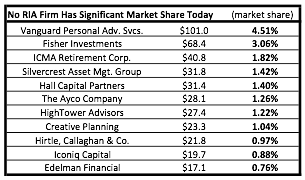

What does this tell us? First of all, we’re still very far from having any real Goliaths in our marketplace similar to Kirkland & Ellis or Baker McKenzie in the law firm space, or Deloitte or Ernst & Young in the accounting profession. The RIA profession is sorting itself out similarly to the other professions; a large plurality of smaller firms, and a relatively small number of larger ones. Looking at the largest firms in the RIA world based on assets under management and percentage of the total RIA assets, nobody has come forward as a dominant Goliath market leader:

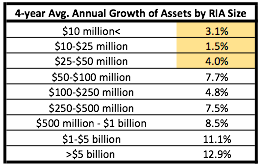

And if you look at the growth rates of the firms of various sizes, you see that once you get above $50 million or so in assets under management, you’re looking at the Davids growing approximately as fast as the Goliaths. I’ve highlighted the low growth rates of the smallest firms because in many cases those solo advisors are committed to a lifestyle practice, and are consciously not trying to be on what they regard as a stressful growth path.

Let’s turn to the next question. On what basis can the Davids compete with the emerging and growing number of Goliaths that will eventually become national firms and name brands? How will they hold their own with the regional firms, or the firms that will create a large footprint in their home city?

Smaller firms actually have several advantages that they can exploit in their fight to remain the solid center of gravity in the planning profession. Let’s count them down from number least to most important .

- Recruiting advantages. Smaller firms can offer their new recruits a more rapid path to face-to-face client interaction than their Goliath competitors – which is an enormous advantage in recruiting. And they can offer more rapid advancement to partnership status for candidates who are ambitious to own equity in their own firms sooner rather than later.

To take advantage: emphasize the entrepreneurial and career development opportunities when you market your firm to young talent out of college. At the same time, pay competitive salaries. Get the word out in your community, and perhaps attract staff advisors who feel their career at a larger firm is dead-ended. Some people just function better in a less bureaucratic or competitive environment.

- Software flexibility. The promoters of the Goliath story always count size and scale to be a big advantage when it comes to buying productivity tools. But if you talk with any of the independent broker-dealer home offices or the larger advisory firms, you will often hear more complaints than boasting about the superiority of their systems. The reality is that the largest firms get trapped in legacy systems, while smaller firms can more easily adjust to new software innovations in a rapidly evolving tech ecosystem.

The scale favors smaller firms. The largest RIA firms may have 300 employees over which to amortize the development costs of its in-house-created systems. The independent software companies that create tools for RIA offices have 50,000-100,000 potential customers over which to amortize their development costs.

To take advantage: Stay on top of new developments in the software ecosystem, and overcome your natural resistance to change. Look for outsourcing opportunities, and constantly ask yourself what services can be automated. In the age of ETFs, model portfolios, online advice platforms and new robo-as-software tools, do you really need an investment officer and trading staff?

- Greater service customization. Financial planning firms, as they get larger, start to face the same issues that the brokerage firms are facing now: they are eventually forced to standardize the services provided by their newly-hired planners, to protect the firm’s reputation against “rogue” advice. And the economics force them to monitor the time that their staff planners spend with a client.

The result: newly-hired staff planners never get the flexibility to use their creativity, spend the time they want with their clients, or provide truly customized solutions to the firm’s clients. The solo practitioner or smaller firm owners are more creative in tailoring recommendations to client circumstances.

To take advantage: Make sure your website tells prospects that, unlike the name-brand RIA firms, you don’t offer canned advice or solutions.

- Leaner and meaner. Smaller firms don’t have the overhead of larger firms. A solo practitioner can work out of his/her home, and can outsource many of the back office chores that represent fixed costs at larger firms. A big part of the overhead is partners who earn significant income for supervising and managing larger scale operations.

These smaller firms can offer planning at lower price-points without compromising their margins.

To take advantage: Smaller advisory firms already tend to be the destination of choice for clients who don’t meet Goliath minimums. Consider venturing into the unlimited blue ocean marketplace of middle class or Millennial clients. Position yourself as a firm that the Goliath firms can refer to when they talk with prospects who don’t meet their minimums.

- Fewer management headaches and managerial friction. Related to Item 7, a smaller firm is much easier to manage than a larger one, and the requirements to orchestrate the activities and interactions of a larger number of people leads to friction and inefficiencies.

Just look at the numbers to see how complexity multiplies with each new hire. With a planner and two staff people, there are three possible interactions. With 10 planners and 20 staff people there are 436, and the next hire adds 20 new interaction vectors, and the one after that adds 21. (See graph below.)

To take advantage: Instead of spending 80% (or more) of your time on management duties, be a planner for clients for 80% of your time, and budget 20% to staff mentoring and tending the vision of the firm.

- Online equalizers. On the web, where most prospects check out advisory firms before making a commitment, the smaller firms can look just as professional and significant as the larger ones – for approximately the same outlay. In fact, because the larger firms have to be more careful in how they portray themselves (they have much more to lose if they foot-fault on compliance or overpromise and get sued), the smaller firm has an advantage in its creative self-portrayal.

To take advantage: Constantly upgrade your website so that it’s at least as professional-looking as the Goliath firm down the street. Create videos (where you tell prospects your personal business mission to help them lead better lives and answer this month’s most often-asked client questions), and be generous about giving away reports, white papers and especially case studies, so prospects can see that you work with people like them, and that you solve challenges like the ones they’re facing.

- Status marketing. Some people prefer to work with the person whose name is on the door. If you were to visit a Merrill Lynch office, you would hardly be invited to speak to Mr. Merrill or Mr. Lynch. Some people feel like working with staff rather than principals is demeaning or means they are getting less than the full portion of available expertise.

To take advantage: David RIAs can use this very line to their advantage in marketing materials. Emphasize that when people walk into your offices, they’ll be working directly with a company principal, not a junior staffer.

- Greater marketing and PR flexibility. Many larger firms feel that they have to be more careful in their interactions with the press, and the brokerage firms have very strict compliance regimes which forbid their brokers from talking to the press at all. Thus, smaller firms enjoy an advantage in their community outreach. Fee-only independent advisors can work freely with the press to educate their communities of potential clients. They can blog without going through nit-picky compliance reviews and take controversial stances that might alienate large portions of the population, but attract the relatively small number of prospects that they need in order to thrive.

To take advantage: Get to know the local press, and tell them that your mission is to help them educate the public about financial issues and raise the level of financial awareness and literacy in the community. Ask clients if they’re willing to share their stories about issues that are important for the community. For some clients, publicity and 15 minutes of fame will be a value-added part of your relationship.

- Less reputational risk. The Goliaths suffer reputational damage across all their offices whenever any single employee crosses an ethical boundary and gets caught – and the odds that someone, somewhere will act unethically goes up exponentially as the firm acquires more client-facing brokers or advisors.

To take advantage: Create printed copies of the large wirehouse BrokerCheck “rap sheets,” which will be, in some cases, dozens or hundreds of pages long, and use them freely to market against the larger firms whose reputation is routinely tainted by scandal. Collect archived headlines from the wirehouse scandals of 2008.

- Greater agility and adaptability. In a hyper-rapid environment, smaller firms can make faster course adjustments in terms of revenue or service models and technology adoption than Goliaths.

And their decisions are made with more accurate and timely information. The owner/decision-makers of the David firms are right on the front line of meeting with clients and managing the day-to-day operations.

Being closer to the consumer means they can see and respond to challenges immediately. As firms grow into Goliaths, they increasingly separate management from the front lines, which means they have a more cumbersome process to becoming aware of challenges, and assessing the immediacy of challenges, and determining whether it would be cost-effective to change legacy processes and systems in response.

To take advantage: Schedule time every year to rethink your revenue and service models, and meet with staff to solicit ideas for improvement. Stay on top of trusted news sources about changes in the profession, and be prepared to overcome your natural, innate resistance to change.

I don’t want to overstate this case. There are many good reasons to seek greater scale – including creating a sustainable firm that will outlive its founders, creating more specialized roles for the staff members, offloading tasks that you, personally, would prefer not to perform and gaining a larger footprint in your market area.

But survivability is not one of them.

Ignore the white paper writers, rollups, would-be buyers and pundits. Advisors can – and will – survive and prosper as Davids, and the solo and small RIA firm will continue to be a significant, thriving part of the financial planning ecosystem well into the future.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com. Or check out his Insider's Forum Conference (for 2018 in San Diego, CA) at www.insidersforum.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All