Don’t Be Fooled by the Yield Curve

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFor the first time in at least 40 years, there’s a fundamental economic reason that a yield curve near-inversion might not herald a recession. The U.S. Treasury yield curve is currently flatter than usual, not quite inverted but close enough to make some people nervous – since, in the past, recessions have almost always followed. I will make the case that it’s likely to be different this time.

“This time is different” are the four words that make economic forecasters into monkeys, but see if you agree with my logic.

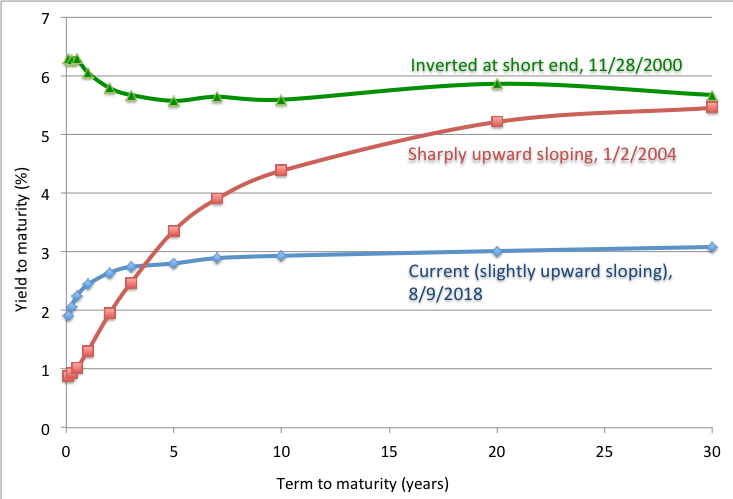

Yield curves – current, normal, and inverted

The U.S. Treasury bond yield curve is usually considered inverted when the yield on the two-year bond is higher than the yield on the 10-year bond. Other definitions are sometimes used, and I favor looking at even shorter maturities than the two-year because they’re more indicative of Federal Reserve policy, but the standard definition is good enough for this discussion. And it’s what most people focus on.

The two- to 10-year yield spread has narrowed to 25 basis points, which is not an inversion, but it’s close. Exhibit 1 compares the current situation to a more typical upwardly sloping yield curve shape and an inverted yield curve:

Exhibit 1

Current, upward sloping, and inverted yield curves

Source: Constructed by the author using data from treasury.gov. The 30-year yield for 2004 is extrapolated.

In the past, inverted yield curves and subsequent recessions have been closely associated, at least in the United States. The not-quite-inverted yield curve is prompting many commentators to ask whether a recession is imminent. Among them is an old master of the investment business, Charles Gave, who writes,

Should this [yield] spread move into negative territory, I would expect a financial accident to occur outside of the U.S., a U.S. recession, or possibly both. In the latter two scenarios, U.S. firms will no longer want to borrow and financial engineering will start to unravel. Zombie companies will fail and capital spending will be cut, as firms move to service debt and repay principal. Workers will get laid off and the economy will move into recession.1

This is especially problematic given how long-lasting the recovery from the 2007-2009 Great Recession has been. But it has also been an extraordinarily slow one, making it more likely – although not in any way guaranteeing – that it will last longer than past recoveries. So far, in terms of time it is the second longest economic expansion on record, but the economy has not been vigorous.

Roadmap through this article

I’m going to start by showing the empirical relationship between yield curve inversions and recessions over the last 40 or so years. Then, I’ll show how the “special” (godawful) nature of the recovery from the Global Financial Crisis distinguishes the current situation from the historical ones. I’ll then review conventional explanations for the yield curve inversion/recession relationship; explain how the new monetary environment weakens the influence of the Federal Reserve and makes old empirical relationships suspect for forecasting; and present reasons why the yield curve may steepen instead of flattening further or inverting. I conclude with some observations from industry and academic thinkers whom I respect.

First, some history

Exhibit 2 shows the historical relationship between yield curve inversions and recessions in the modern (post-1977) period. The blue line is the 10-year minus two-year yield spread. The green circles show a breach of the 50 basis point threshold for a near-inversion, considered a danger point. When the spread is below zero, the yield curve is actually inverted; and the red circles show the trough of each inversion. Recessions are the shaded gray areas.

Exhibit 2

History of 10-year minus two-year yield spreads, 1977-2018

Source: Charles Schwab; underlying sources are Charles Schwab, FactSet, as of April 20, 2018. Bps=basis points.

Each recession was preceded by a yield curve inversion, and each yield curve inversion was followed by a recession within one to two years. It’s been a powerful relationship. There were false alarms, in the sense that a breach of the 50 basis point threshold, in the mid-1980s and then again in the mid-1990s, was not quickly followed by a recession – but there was no false alarm from an actual inversion, only real ones.

This time is different?

It’s reasonable to be worried. The current recovery or expansion is quite old, having begun in June 2009, nine years ago. The all-time record is 10 years (1991-2001). But something is different this time. The recovery began slowly and didn’t build up momentum until 2014; then it slowed again, and only recently accelerated. The whole last decade has been something of a disappointment in the real economy (“secular stagnation,” according to Larry Summers), although it’s been great for the S&P 500.

This means that, as I said at the outset, for the first time in at least 40 years there’s a fundamental economic reason why the current yield curve near-inversion might not forecast a recession. At least according to some, the excesses that need to be corrected by a recession – high inflation, high levels of debt, rich stock market valuations, and tightness in the labor market – aren’t there in any convincing quantity. (The stock market is a little rich by historical standards, but not enough to get excited about.)

The sluggish recovery after 2009, then, was more like a continued recession than like the boom conditions that typically follow a bust. The expansion could have a ways to run.

A conceptual framework for understanding the issue

There are basically four possibilities. One is that yield curve inversions and recessions have nothing to do with each other, except by coincidence – they’re like sunspots and commodity prices. I don’t believe that. A very wise man, Ian Fleming (author of the James Bond books), said that “Once is happenstance. Twice is coincidence. The third time it's enemy action.”

We’re in enemy action territory.

The second possibility is that yield curve inversions cause recessions. There are some reasons why this might have been the case in the past, but I will argue that it’s less likely to be true now.

The third possibility is that recessions cause yield curve inversions. Given that the yield curve inversions usually occur first, that idea can be dismissed.

The fourth and most intriguing possibility is that yield curve inversions reflect, and are the consequence of, conditions in monetary and fiscal policy, and in the supply and demand for capital, that may cause, but are not guaranteed to cause, a recession. In other words, the two are related, but indirectly. Any forecast that we make based on such a relationship is going to be quite uncertain, but still worth paying attention to. That is the hypothesis on which I’m going to focus in the rest of this essay.

Conventional explanations for the yield curve inversion/recession relationship

The traditional explanation for the relation between yield curve inversion and recessions is that, when inflation begins to get out of control, the Fed causes recessions in an attempt to reduce the inflation rate. Paul Volcker, a hard-money man appointed Fed chair by a desperate President Carter in 1979 when inflation was running at around 12%, was successful using this strategy. He raised short-term interest rates to 20%, sending the economy into a very sharp recession in 1981-1982. Inflation quieted down to 4% by 1984 and high inflation rates never came back, although it has proceeded at a 2% to 3% rate ever since and those price increases add up over long periods of time.

Volcker was a hero because very high and accelerating inflation rates are much more destructive than all but the worst recessions. In the Great Inflation of 1940-1981, fixed-income investors (savers) lost almost their entire fortunes in real terms. You can recover from a recession but two generations of savers can’t get their savings back. The inflation had to stop.

But how did the Fed’s rate increases cause a recession? (The Fed’s strategy of using high interest rates to force a recession and thus a decline in inflation also worked in 1991 and 2001, so there was something real going on here.) Again, let’s recap the conventional wisdom. By raising short-term interest rates (at that time it had no influence over long-term rates), the Fed prevented banks from making a profit by “borrowing short and lending long,” their usual modus operandi. Borrowing short means taking deposits on which short-term interest rates have to be paid, and lending long means investing in long-term securities, such as mortgages. This only works well when long rates are significantly higher than short rates.

When banks can’t make a profit by lending, they don’t lend. The capital shortage or credit crunch drives the economy into an intentional recession, taking the pressure off of wages and prices and causing inflation to recede.

But the yield-curve effect on recessions is a second-order effect. The first-order effect is the high cost of borrowing. Most business borrowing is short term. If interest rates are high – punishingly high, in the case of the 1981-1982 recession – that’s enough to discourage borrowing and put the kibosh on business expansion or even survival. A lot of small companies that survived many earlier financial dislocations did not survive 20% interest rates.

At any rate, it was certainly possible that, until not all that long ago, yield curve inversions caused or were one of the causes of recessions. That story comports with the old-fashioned monetarist view that prevailed during Milton Friedman’s tenure at the University of Chicago.

That view, however, is not up to date.

The new monetary environment

First of all, banks now have all kinds of hedging instruments at their disposal. They should not care whether the yield curve is inverted. Like any other business, they should invest in any positive net-present-value project, and finance the project using the best borrowing strategy they can identify. If short rates are low, they can borrow short, and hedge future rate increases. If short rates are high, they can borrow long, locking in low interest costs.

Second, and much more important, the Fed has lost much of its power. The Fed used to determine the money supply; it now is one of many players in that game, the others being hedge funds, money market funds, cryptocurrency issuers (a small factor now but it could grow) and, most importantly, credit grantors. We all know about mortgage and home equity lending, but even the S&P 500 is a component of the money supply if you can seamlessly borrow against your holdings of it to make a purchase or pay your debts.

All these trends have made mincemeat of the idea that the Fed can do what it thinks is best for the economy and then just wait for the desired result. The Fed helps the process along by making it a little more difficult for businesses to borrow if they want to slow the economy, and a little easier to borrow if they want to stimulate it. In the last decade, however, we’ve seen how ineffective stimulus can be when the winds in the larger economy are blowing in the other direction.

As a result, the Fed is more reactive than proactive, more likely to be behind the curve than in front of it. Exhibit 2 makes it look like it’s ahead of the curve because the yield curve inversions precede the recessions, but – so the argument goes – the recession was already preordained by fundamental economic forces and would have happened almost no matter what the Fed did.

A natural business cycle?

Recessions are preordained if the business cycle is a natural phenomenon, independent of monetary policy; according to this view, booms create the conditions (high input costs) that cause a recession, and recessions cause the conditions (cheap resources) that cause a subsequent boom. While economic historians continue to argue about it, this explanation feels right: we had a vigorous business cycle long before there was a Fed.

To sum up, yield curve inversions may have caused recessions in the past when Fed activity was more powerful, but this time really could be different. The short-term rate hikes are way behind the curve, with the Fed struggling to justify getting rates up to levels that would be considered wildly dovish at this point in the business cycle in any previous expansion.

If there was a causal relationship between yield curve inversions and recessions in the pre-financial crisis days, then, there may not be such a relationship any more.

The yield curve may steepen, not invert: A fiscal quandary

Why long-term interest rates are so low continues to be a mystery. Jamie Dimon, no fool, recently said, “I think rates should be 4 percent today. You better be prepared to deal with rates 5 percent or higher — it’s a higher probability than most people think.”2

Yes, you’d better be prepared. Three major factors determine long-term bond yields3:

- The supply and demand for long-term capital, based on savings rates (supply) and opportunities that borrowers perceive in the real economy (demand). When corporations and other real-economy players are optimistic, interest rates are higher because the players think they can earn a spread over the borrowing rate by making risky investments;

- The risk premium that investors require for bearing the price fluctuation risk of long bonds, and

- The financial condition of the borrower.

The U.S. economy has not been as dynamic as it is now in over a decade, and the rest of the world is a patchwork of good and bad, so the supply-demand situation suggests long-term interest rates should be somewhat high. I have no special information on the risk premium.

But the borrower – the U.S. government – is deeply in debt (over $20 trillion, or about a year’s GDP), of which $15.4 trillion is held by the public and thus subject to market discipline. It’s not a shockingly huge amount relative to GDP, and the U.S. will be able to pay its bills in nominal terms. Lenders, however, look to the future, and the financial position of the U.S. is getting worse, not better. The government will have to borrow trillions more to finance Social Security, Medicare, Medicaid, and the interest on the debt it already owes – to say nothing of the other important functions of government that are being crowded out by entitlement spending. Infrastructure is just one painfully obvious example.

Eventually the baby boomers, to whom much of this entitlement budget is owed, will die, and the problem will go away. But, by then, the bonds that are in the market today will have matured, so the eventual resolution of the problem doesn’t help the bondholders much. Since the government owns a printing press, it won’t default in nominal terms, but it will have to devalue the real worth of the principal through inflation, which means higher interest rates.

That’s a long-term forecast that may not take effect in the next year or even several years. But it points to yield curve steepening, not flattening or inversion.

Another view from Gavekal

Charles Gave, whom we met earlier, is the patriarch of his consulting firm, Gavekal, but he and his associates do not always agree. In a July 16, 2018 Gavekal publication, Tan Kai Xian and Will Denyer argue that “the interest rate environment is not yet signaling an imminent recession.” They cite three favorable indicators:

- The yield curve is not yet inverted, and it was relatively flat, as it is now, during “one of the greatest growth and bull market periods of recent history” – 1995-1999, when the stock market tripled. “It was only when it significantly inverted in 2000,” they note, “that it prefigured a bear market and recession.” Also, that recession was mild, although the stock market decline was nearly 50%, not surprising considering the lofty level from which it fell.

- “The forward spread is not pricing in a recession either.” The forward spread is the difference between the market’s expectation of future short-term rates, as revealed in the forward market, and the actual short-term rate now. This is a more precise measure of the market’s expectation of changes in the short-term interest rate, because long-term yields are averages of interest rate expectations over a series of short runs and thus contain smoothed or muddied information. I agree with this analysis; today’s forward spread implies higher short-term interest rates in the future, inconsistent with a recession.

- “Real long-term corporate bond yields have risen only slightly and remain well below our best estimate of the real rate of return on capital,” the authors write. If corporations think they can invest in the real economy at a rate of return higher than the borrowing rate, business conditions are good and do not foreshadow a recession.

This last point is the most important one, since it captures the idea that there is more to the business cycle than interest rates. The expected or consensus real rate of return on capital is a fundamental, not monetary, factor and must be figured into any sensible forecast. The Gavekal authors conclude, “We are not yet ready to join Charles in calling for recession.” Neither am I.

Is the yield curve inversion/recession relationship just a U.S. phenomenon?

An interesting sidelight is provided by a report from AQR Capital Management, which consistently churns out some of the industry’s best research. AQR points out that the tight yield curve inversion/recession relationship only holds in the United States. “In Australia, for example,” they write, “since 1990…the yield curve has been inverted four times, but there has only been one recession.” (AQR, enamored of wry humor, blames it on crocodiles.) They continue, “Japan’s yield curve has not been inverted since 1991, yet Japan has had multiple recessions.”

The German yield curve has behaved oddly: Two inversions were followed by recessions. “Since 2009,” however, “the German yield curve has been fairly steep, but that did not prevent Germany from falling into recession during the European sovereign crisis in 2012.” One possible explanation is that Germany does not have its own currency; the euro reflects events outside Germany so it shouldn’t logically be closely related to German domestic economic performance.4

It’s interesting that the relationship between yield curve inversion and recessions mainly apply to the United States, or used to. If the relationship has changed, it’s probably for the reasons mentioned earlier, about the Fed having less power and the current expansion having been so weak for so long. But we should also remember that the U.S. still issues the world’s reserve currency, a status that the French President Valéry Giscard D’Estaing called an “exorbitant privilege.”5

It is a privilege indeed, one that gives our economy an extra level of resilience. While a naïve interpretation of the AQR findings could be that the U.S. is uniquely vulnerable to Fed actions that flatten the yield curve, I draw the opposite conclusion – the U.S. economy is distinctively strong among the mature nations, and a minor shift in interest rates is not going to drive it into recession.

Conclusion: The old rules may not apply

John Cochrane, a professor at Stanford’s Hoover Institution and an intellectual heir to Milton Friedman although disagreeing with him on many specifics, believes the expansion has substantial room to run. His work on the relationship between macroeconomics, monetary policy, and fiscal policy is startling in its originality. Everything he writes is worth reading. Cochrane advises:

The economy has finally recovered from the 2008 recession. Demand is over [that is, there is no more inadequacy of demand]. Further growth depends on [growth in] supply – larger productivity or [a larger] labor force, and supply depends on incentives. It is the end of the beginning, not the beginning of the end.

We will grow until something happens. Recessions don’t happen on their own, and a longer expansion does not make a recession more probable. A recession needs a spark, something to go wrong.

[Martin] Feldstein is right, a panic monetary tightening from the Fed could be that spark, as it has so many times before… A war or a trade war could be that spark. “Don’t screw up” is policy advice often overlooked in the quest for dramatic action.

One thing we know for sure – recessions are unpredictable. If we knew for sure a recession would happen in the near future, then it would already have happened today [because]…if companies knew business would be bad next year, they would stop investing, and business would be bad today.

So take all predictions with that grain of salt – but examine hard the logic behind them.6

I couldn’t have said it better – or nearly as well. Don’t panic. The relation between yield curve inversions and recessions is likely to break down, as did the Phillips curve in the 1960s and the relation between stimulus and inflation in the 2010s. Analyze the fundamentals, be cognizant of valuations, and invest accordingly.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation and an independent consultant. He may be reached at [email protected]. His web site is http://www.larrysiegel.org.

1 Gave, Charles. 2018. “Why A Curve Inversion Matters.” The Daily, Gavekal Research (May 1). In this particular passage he is talking about a different yield spread, but the same general principles apply. Full disclosure: Gave managed a substantial asset portfolio for my former employer, The Ford Foundation, during much of the time I was employed there.

2 At the Aspen Institute’s 25th Annual Summer Celebration Gala, August 4, 2018. As reported by Bloomberg Markets.

3 This analysis applies to real, not nominal, yields. The nominal interest rate or yield also reflects inflation expectations and equals the real yield plus expected inflation over the life of the bond.

4 AQR Capital Management. 2018. “The Yield Curve Is a Very Interesting Topic.” Macro Wrap-Up (May 4),.

5 He was Minister of Finance when he made the comment and only later became President.

6 Cochrane, John. 2018. “It's the end of the beginning for the economy, not the other way around.” The Hill (online, May 23), My italics.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All