Do We Face a Retirement Crisis?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe popular view among Americans is that we face a retirement crisis. Traditional pensions have almost disappeared in the private sector and been replaced by 401(k)s with less than 50% participation and inadequate savings. According to one survey, 88% of Americans fear we face a retirement crisis.

But receiving far less publicity are views from a few experienced researchers pointing to evidence that retirees are actually doing okay. I’ll sort out these differing views.

An ominous outlook

Over the past 40 years, there has been a dramatic shift in the private sector from traditional defined-benefit pensions to retirement-savings plans, mostly IRAs and 401(k)s. In the early 1980s over 60% of private sector employers offered defined-benefit (DB) plans, and that has declined to less than 20% today. And benefits have been frozen in many DB plans and not offered to new employees. Retirement savings plans have not made up for the loss of traditional pensions. Only about 50% of workers have employer-sponsored plans, and many who are offered such plans either fail to participate or contribute adequately. This recent Wall Street Journal report cited a statistic from the Center for Retirement Research at Boston College (CRR): For households nearing retirement age and participating in a 401(k), the median balance in tax-advantaged investment accounts is $135,000. Such a balance would only produce about $600 per month if annuitized at age 65.

Those are not the only issues with retirement-savings plans. “Leakages” from such plans are common as families lack other funds when emergencies arise, and workers often cash out when they change jobs. Employees lack the skills to allocate assets and manage money in these plans, and, when they get to retirement, are particularly clueless about how to convert retirement savings into sustainable lifetime income. And there are special difficulties for certain segments of the population such as “gig” workers, single women (many widowed) and minorities.

The Social Security Administration estimates that 21% of married couples and 43% of single seniors rely on Social Security for 90% or more of their income. Professor Teresa Ghilarducci and Tony James point out in their book, Rescuing Retirement, that for the median income worker, Social Security minus Medicare premiums cover only 29% of pre-retirement income compared to 70% that is typically cited as the replacement rate needed to maintain one’s lifestyle. Lower-income workers will typically do better than 29% because of the progressive nature of the Social Security benefit formula, but many will not be able to maintain their lifestyle in retirement.

Since 2006 the CRR has been publishing and regularly updating the National Retirement Risk Index (NRRI) that estimates the percentage of Americans in various age groups who are at risk of not being able to support their current lifestyle in retirement. In their most recent reporting the CRR highlighted a worrisome trend that the outlook for Baby Boomers and Generation Xers is far less promising than for current retirees. It estimates that 50% of households are at risk of not being able to maintain their living standards in retirement, and, when health care costs are explicitly taken into account, the outlook worsens.

To some extent, the lack of voluntary savings for retirement reflects the financial strains that many working families face. Real-wage growth has flattened since the late 1970s. In this blog post, economist Robert Reich discussed the middle-class squeeze brought on by flat wages, and how American have coped – women moving into the work force, longer hours and less savings and more debt. His view is that the middle-class has reached the limits of these coping mechanisms. This state of affairs does not bode well for Americans needing to save more to pay for retirement.

Given the above evidence, it seem that the answer to the question, “Do we face a retirement crisis?” is a definite “yes” and it would be a miracle if we did not.

A different view

But there’s conflicting evidence that needs to be examined. The figure I mentioned earlier of 88% of Americans fearing a retirement crisis was from CNBC reporting that also cited both a Gallup poll finding that 74% of retirees were living comfortably and a Vanguard report that only 16% of retirees were dissatisfied with their financial situation. Data also shows lower poverty rates for those over 65 than for the working-age population.

Not all researchers agree that we face a crisis. One of those with a more optimistic assessment is Andrew Biggs of American Enterprise Institute whose views have appeared often in the popular press. He summarized his research findings in this Forbes article.

He found that retirees were not depleting wealth and were, in fact, typically increasing their wealth over the course of retirement. If we were, indeed, in a crisis retirees would be running out of money. Using data from the Fed’s Survey of Consumer Finances (SCF), he focused on retirees who were 65 to 67 in 1989 with a median net worth of $122,318 in 2013 dollars and followed this cohort over time. By 1998 their net worth had risen to $219,146, and by 2007 it had risen again to $247,532. Even after the financial crisis, the net worth of this cohort had declined only to $202,400 – well above the starting value.

In fairness, Biggs pointed out that these figures were influenced somewhat by wealthier members of the cohort living longer, but he also referenced studies by other researchers using Health and Retirement Study (HRS) data that followed specific households. Some of these studies show declines in wealth, but at a slower pace than remaining life expectancy, meaning that spendable income was increasing.

Many retirees seem to find a way to live off the income that they earn, which often consists mostly of Social Security benefits. There is a general reluctance to spend down savings to meet lifestyle needs but, instead, to hold onto these funds for health care costs or other contingencies. The Society of Actuaries (SOA) has conducted a series of interviews with retirees in different age groups in order to provide insights about retirement spending. This website provides links to a number of different SOA retirement projects including the May 2018 report on interviews of retirees over age 85 and a January 2016 report on those retired 15 years or more.

There are also questions about the often-cited 70% retirement-income replacement ratio. Researcher Frederick Vettese argues that it should be no more than 50% when households enter retirement with no mortgage and children out of the home. Michael Hurd and Susan Rohwedder of the RAND Corporation have studied HRS data in great detail and have argued in this paper that the replacement-ratio analysis doesn’t make sense and a much more nuanced view of the retirement life cycle is needed, including natural declines in discretionary spending as retirees age.

Dallas Salisbury, the retired former head of the Employee Benefits Research Institute (EBRI), contends that it’s a myth that everyone used to have pensions and now they have been taken away. He argues that people always changed jobs frequently, which diminished the value derived from defined-benefit pensions.

Arguments going back and forth about whether there’s a retirement crisis often take the form of data wars between researchers who understand the particulars of the data sources they work with in far greater detail than the general public. Occasionally one will read a convincing data-supported case by one researcher followed shortly by an equally convincing data-supported rebuttal from the other side.

So there is no straightforward way to firmly conclude whether we face a retirement crisis.

Trends

The “no-crisis” views are mostly based on studying existing retirees while researchers expressing concerns are more focused on future retirements. The natural question is whether there is a worsening trend.

It is very challenging to interpret trends given the variety of data sources and their particular quirks. For example, the SCF, which has been heavily relied on, leaves out non-regular IRA and 401(k) withdrawals, so researchers have had to attempt adjustments to get a fuller retirement-income picture. Also, survey questionnaires are updated from time to time, which makes trend interpretation difficult.

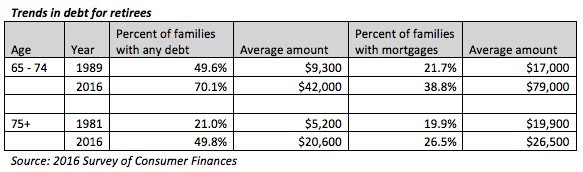

However, one trend that is both clear and concerning is the increase in retiree debt – both mortgage and consumer debt. The chart below shows trends from the SCF for as far back as data is available. The average amounts are for those who hold the particular debt category and the dollar figures are adjusted for inflation to make them comparable.

The percentage of families carrying mortgage and other forms of debt is increasing substantially, and the average amounts of debt are increasing even more dramatically. Regardless of what happens with retiree income and savings, increasing debt burdens will place a greater strain on financial wellbeing in retirement.

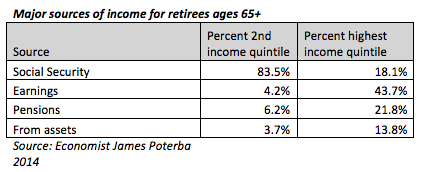

Certainly the most talked about trend affecting retirement is the shift from DB to DC retirement plans. Unfortunately it’s hard to find easy-to-understand evidence on the trends in income derived from DB pensions versus from DC retirement plans, partly due to the SCF reporting issue mentioned above. We need to rely on researchers who work with such data full time to provide interpretations. The chart below from economist James Poterba is a few years old, but illustrates how the impact of trends differs greatly by income category. Those in the bottom half of retirement income derive most of their income from Social Security. Any changes to this program such as the current phase-in of the age-67 full-retirement age (FRA) have a big impact on the bottom half. The continuing shift from DB to DC won’t have as much impact on the bottom half.

However, there may be cause for the concern about the shift from DB to DC if we hope to improve financial prospects for retirees overall. DC plans tend to work out much better for workers at the top of the income scale who are more likely to participate in such plans and can afford to save substantial amounts. Two years ago Monique Morrissey of the Economic Policy Institute produced a chartbook based on the 2013 SCF and supplementary material that highlighted inequality in our retirement systems. She demonstrated that inequality in the programs that retirees rely on in addition to Social Security is more extreme than more publicized income and wealth inequality.

Conclusion

After reviewing arguments from both sides, my personal view is that we do not yet face a retirement crisis. However, certain population cohorts such as single women, are in much worse shape than others. A key factor that has kept us from a general crisis is that retirees have downsized their spending to match their income sources. But this situation is not ideal. If workers had saved more and/or worked longer, they would not have had to cut back so much in retirement.

There is more cause for worry looking ahead – increasing debt loads for retirees are a particular concern, as well as low interest rates, increasing longevity, reduced Social Security benefits and higher health care costs. We need to find ways to do better.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire in the UK.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All