Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Over the past 10 years, the financial press has been overflowing with news of robo-advisory services – the early launches, the astonishing asset growth and the threat (or lack thereof) to financial advisors.

Enter robo palooza

When robo-advisors first rolled on to the scene, I was tickled to see someone automate the interrelationship between a client’s ability and willingness to tolerate risk – and then marry the two with a seamlessly allocated (and rebalanced!) investment portfolio.

And then the fees – oh, the fees you save! How could the investing public possibly resist paying 50-80% less than those greedy financial advisors charge? Not to mention the fact that some of those financial advisors were probably allocating to high-cost mutual funds instead of the low-cost ETF nirvana offered by the robos.

I am a huge fan of investment automation. One of my most cherished career roles was spent developing trading algorithms that managed client order flow at a busy broker-dealer. But I also know what it is like to work with individual investors on a one-on-one basis as their portfolio manager. In this role, solutions are highly customized and a great deal of time is spent tailoring the offering to their specific needs.

In looking at robo-advisors fairly, the investing public, who embraces it as a solution, are getting short-changed.

I’m not saying this because I think that, as an industry colleague put it several years ago, robos are just a bunch of “glorified target-dated funds.” I just think the “advisory” moniker is inaccurate.

Where robo-advisors fall short

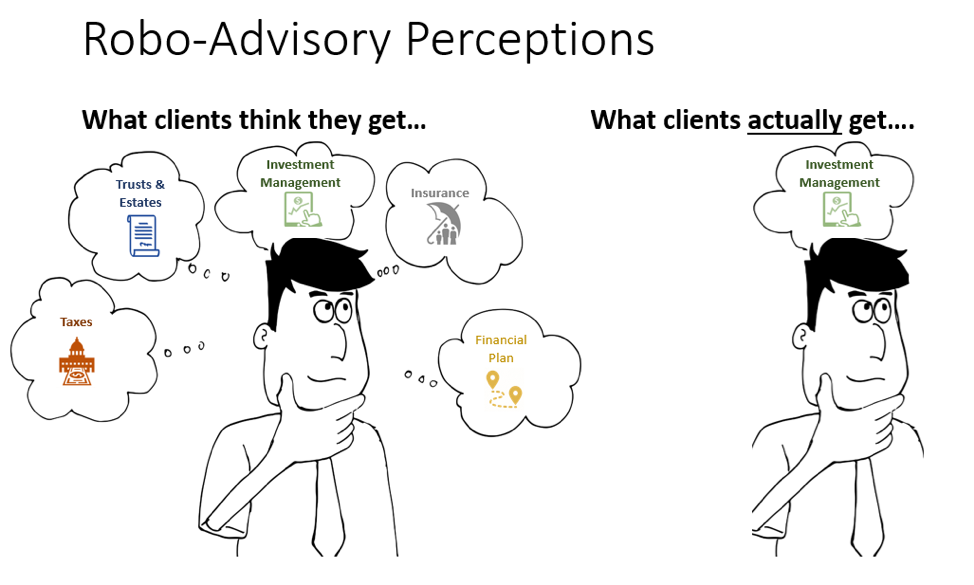

Clients are best served when provided unbiased, unconflicted and complete advice delivered by a well-qualified fiduciary (a professional required to place the client’s interests ahead of his/her own). Robos (notwithstanding high mandatory cash holdings at some) do deliver on some – but not all – of that value proposition. They are investment advisors only.

Here is the bigger issue: Investment management is not financial planning.

A family cannot button up their entire financial well-being via a 15-minute online survey and a couple online signatures. Proper and complete financial planning must take into account a myriad of other questions such as:

- What do we keep? (Taxes)

- When do we protect it? (Insurance)

- Where does it all end up? (Estate)

- How do we get there? (Integrated Plan)

Robo-advisors fail to answer the four critical questions above – mainly because it is first and foremost an investment management solution.

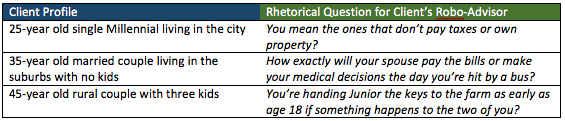

I challenge you to find someone served completely by a robo-advisor. I’ll even provide you a few examples:

Filling In the gaps with robo-planning technologies

So, if I have convinced you that robo-advisors are, at best, a complete solution for very few, and at worst, a mirage of comprehensive planning, I would like to close on a promising note.

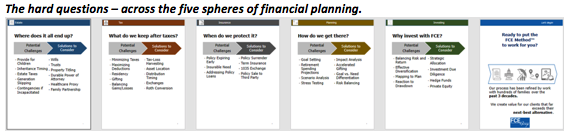

There are elements of the unanswered questions that are ripe for both automation and integration.

Yes, I believe that financial planning can be viably automated and integrated in such a way that brings true comprehensive financial planning to the masses, in a format that is cost-effective and meets the fiduciary standard.

I am not proclaiming the death of the financial advisor value proposition. I see complicated financial situations daily that could not conceivably be addressed by even the most advanced programs and algorithms.

Here’s what I am saying: There are large swaths of the financial planning landscape that can – and should – be both automated and integrated in such a way to which robo advisors aspire, but do not yet currently deliver. I say this from the perspective of someone who has worked exhaustively over the past decade to deliver best-in-class integrated solutions to clients across the spectrum of planning needs.

I, for one, am excited to begin building such technology, and welcome like-minded advisors and technologists to join me in drafting a solution that is truly capable of improving the complete advisory value proposition.

Carl A. Friedrich joined FCE Group in 2014, and serves as senior managing director. Carl is a CFA® charterholder, Financial Risk Manager (FRM), Enrolled Agent (EA), and Certified Financial PlannerTM Professional (CFP®). FCE Group is a Long Island, New York-based independent, fee-based, client-focused wealth management, investment advisory and financial planning firm.

For appropriate disclaimers, please go to: https://www.fcequities.com/legal-notice