Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Dr. Jeremy Siegel, professor of finance at The Wharton School of the University of Pennsylvania, has done a remarkable study of the returns of different types of assets over the past 200 years. He published his findings in the book Stocks for the Long Run in 1994. He has updated the book several times, most recently in 2014. It is surely one of the best books on investing of all time.

This article focuses on chapter 15 in Siegel’s book, “Stocks and the Business Cycle.” This chapter was a revelation to me when I first read it in 1994. It makes so much sense, and yet it’s rarely discussed in the financial literature. It’s as if Siegel discovered a gold mine and nobody else was interested. I’ll give you the short version of this landmark chapter.

Cliff notes for chapter 15 of Stocks for the Long Run

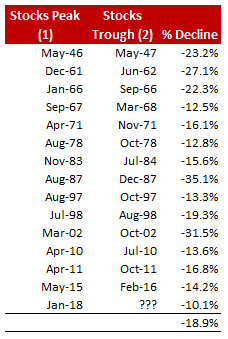

Invariably the stock market turns down before a recession hits and rises before it is over. Of the 47 U.S. recessions since 1802, 43 (9 out of 10) have been preceded by stock market declines of 8% or more. The table below is from the book.

Stock Prices and Business Cycle Peaks, 1948-2017

If an investor went to cash or Treasury bonds four months before each recession, the gains would be significant. The problem, of course, is knowing when to get back into stocks.

Here’s where the real money is made

I have a voracious appetite for anything related to the stock market, the economy and behavioral science. When I come across information like what is shown in these tables, I pay attention. Is it just coincidence, or is there something else going on? Do stock market investors “sense” when a recession is coming, precipitating a market decline? To answer this question, we also must talk about false signals.

Recession False Alarms by Stock Market, 1945-2017

The stock market telegraphs the onset of a recession, but it also gives false signals. What are we to make of this?

Market declines that are not followed by a recession (false signals) are notably shorter in duration and less severe than declines that presage recessions. This is an easy hurdle to clear. When the market is in decline, but the economic indicators are healthy, investors should stay invested and take the short-term pain that the market is dishing out.

If, on the other hand, the economic indicators are in decline, an aggressive and proactive defensive strategy is warranted. That might involve cutting back on equity exposure, buying a put on the market or switching from stocks to bonds. Each investor must decide for him/herself how to play defense.

Why go to all the trouble?

According to Siegel, an investor who correctly plays defense stands to gain as much as 5% per year in returns, versus an investor who simply stays put throughout recessionary periods. This is more than enough reward for going to all the trouble. Here is what Siegel had to say in his book:

My studies show that if investors could predict in advance when recessions will begin and end, they could enjoy superior returns to the returns earned by a buy and hold investor. Specifically, if an investor switched from stocks to cash or short-term Treasuries 4 months before the start of a recession and back to stocks 4 months before the end of the recession, he or she would gain almost 5 percentage points over the buy and hold investor.

Gains through timing the business cycle – Part 2

We now move from the theoretical aspects of Siegel’s research to the practical realm. We do this by looking at actual returns, using real clients with real money invested, by applying various investment strategies over the past 20 years.

The numbers in the table below come from actual client accounts, beginning in 2002. Prior to 2002, the numbers come from back testing, using the identical strategy parameters.

I would like to draw your attention to the 6th strategy in the table – “Recession Defense.” This is the strategy I designed to capture the 4-5% bonus returns from timing the business cycle, as described in Siegel’s book.

The returns for the Recession Defense strategy are the same as they are for a traditional buy-and-hold strategy for the time period that began after the last recession. This is because the strategy is only invoked at the early stages of a new recession forecast. Most of the time this strategy will remain operating quietly in the background until it’s needed.

Once the model raises the alarm for a new recession, the returns for buy-and-hold and Recession Defense start to diverge. At the end of the full 20-year period, the Recession Defense strategy has outperformed the buy-and-hold strategy by 13% per year. If that seems hard to believe, consider this. The last 20 years included two severe recessions and two severe bear markets. All an investor had to do was get out of the way when the warning signs were there and get back into stocks when the model sounded the all-clear. Yes, it can be and has been done.

As I said earlier, my model isn’t perfect (87% accuracy score), and it’s not the only one. But it has worked well enough to add substantial value to my clients’ portfolios over time.

If you decide to stand pat during recessions, eventually you will get back to even. This is why the buy-and-hold doctrine is so appealing, and Siegel is a big advocate of this doctrine. But here’s the thing. A bear market may not cost you money in the long run, but it will certainly cost you time, and lots of it.

For example, those unfortunate souls who bought into the stock market mania in 1929 not only lost their collective shirts in the downturn, but it took them more than 20 years to get back to even. Do you have 20 years to wait to get back to even?

Recession forecasting

Returning once again to Siegel,

If one could predict in advance when recessions will occur, the gains would be substantial. That is perhaps why billions of dollars have been spent trying to forecast the business cycle. But the record of those efforts is extremely poor.

My own research agrees with that statement. Forecasting recessions is extremely difficult. But it’s not impossible. I know of at least three recession forecasting services (here, here and here) that have been around for at least a decade and have accuracy scores of 80% or higher. (I did my own analysis on their published forecasts to arrive at this accuracy score.) I also have my own recession forecasting model that has an 87% accuracy score, using the same analysis methods I used for the other three forecasting services.

The benefits of having a contingency plan

Unless you’re financially independent, stock market investing is going to play an important part in your retirement planning. The whole point of financial planning is to find a way to make sure your cash doesn’t run out before you do.

But investing in stocks means you’re going to go through some harsh market declines. Investors who expect to earn generous returns while watching their net worth rise smoothly are fooling themselves.

The best way to protect your nest egg from the next bear market is to plan ahead. Having a contingency plan, even a simple one, will save you from the worst parts of a bear market. You will never be able to sell at the top and buy back in at the bottom, but if you can avoid the worst months of a bear market, your returns will be significantly higher than a buy-and-hold investor.

A contingency plan is an add-on to your strategic plan. Brokers, advisors and planners often don’t cover this critical aspect of investment planning. The advice industry does a good job of designing plans that serve investors well while the economy and the market are healthy and growing. That’s how it is about two-thirds of the time. But what about the other one-third of the time? Their standard answer is “Don’t worry about it, just stay invested and ride the waves.”

That’s not bad advice for many investors, especially those who don’t have the time to fiddle with their investment accounts. Many others just aren’t interested in investing, so not worrying about bear markets or recessions makes perfect sense for them. For those who do care about bear markets, there is a better alternative: your ”plan B.”

An example of a contingency plan

A contingency plan doesn’t have to be complicated to be effective. What’s required is to take some time, perhaps an hour, and think about what you should do when things start to fall apart. The method I teach my clients is setting up a simple rules-based tactical plan that tells them exactly what to do, and when to do it. For example

This is a very simplistic example. But with such a plan in place, you don’t have to stress about what to do. You just look at the recession indicator and follow your own instructions.

Final thoughts

Recessions and bear markets are two of the topics about which I’m the most passionate. I’ve devoted most of my career to studying the link between the two, and the models I designed are the result of hundreds of hours of effort. I would be happy to answer any questions you have about this topic, and I encourage you to sign up for the free stuff on my website, like the weekly newsletter, the mini-courses in investment theory, and the quizzes.

Erik Conley was a trader and portfolio manager from 1975-2001 and former head of equity trading at Northern Trust Co. in Chicago. He is now a private investor, founder of a nonprofit investor advocacy firm and private investing coach.

Read more articles by Erik Conley